Yahoo Finance

Yahoo Finance Nordstrom (JWN) on Track With Long-Term Plans: Apt to Hold?

Nordstrom Inc. JWN is well-placed for long-term growth, backed by its efforts to drive efficiency and improve customer experience via faster order fulfillment. It is also on track to reduce inventory and optimize product mix. Its market strategy aimed at capitalizing on its digital-first platform to serve customers better, gain market share and deliver profitable growth bodes well.

The company is benefiting from increased emphasis on Nordstrom Rack. Management remains focused on enhancing customer experience, improving the Nordstrom Rack performance, increasing inventory productivity and progressing on supply-chain optimization initiatives. The company is confident about the strength of brands, and the ability to drive profitable growth and deliver long-term value to shareholders.

Markedly, the introduction of Rack stores, the expansion of the Nordstrom banner digital sales and comparable store sales growth across the company’s banners appear encouraging.

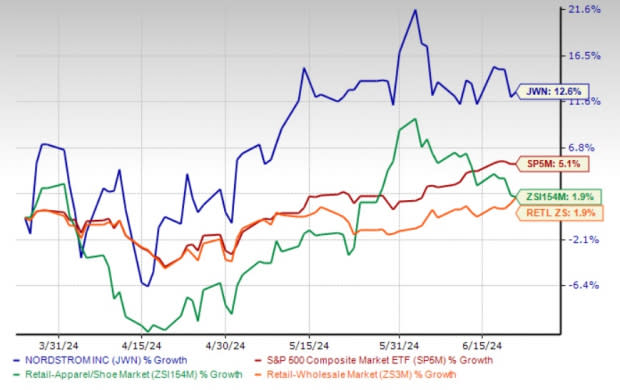

Shares of this Zacks Rank #3 (Hold) company have gained 12.6% in the past three months compared with the industry and the sector’s growth of 1.9% each. The consumer goods company also compared favorably with the S&P 500’s rise of 5.1% in the same period.

Image Source: Zacks Investment Research

What Places JWN Well?

As part of its long-term growth strategy, Nordstrom is focused on three areas — winning in the most important markets, expanding the reach of Nordstrom Rack and enhancing its digital velocity. It remains focused on the closer-to-you strategy, which aims to link stores and services to expedite deliveries, expand online offerings, and add cheaper merchandise at its Rack off-price stores, to improve customers' shopping experiences.

The company’s increased focus on distribution capabilities, and the improved connectivity of physical and digital inventory are expected to aid Nordstrom Rack sales by $2 billion in the long term.

As part of the earlier issued long-term outlook, JWN predicts revenues to grow in the low-single digits annually in the long term. This growth is expected to be accompanied by the operating income growth rate outpacing revenue growth annually. The EBIT margin is expected to be more than 6%, with annual operating cash flow anticipated to be more than $1 billion. Capital expenditure is expected to be 3-4% of sales.

Additionally, Nordstrom has been focused on supply-chain optimization efforts beginning in 2022. This plan has been enhancing customer experience via speedy deliveries while delivering significant customer benefits and operational efficiencies. Hence, the company remains focused on operational optimization. Such endeavors resulted in more than 5% quick click-to-delivery speed and improvement in variable fulfillment costs in the first quarter of fiscal 2024.

Going ahead, JWN continues seeking additional efficiencies in flow and improved productivity through inventory management initiatives.

Hiccups

Nordstrom has been witnessing headwinds related to the recent wind-down of Canadian operations, hurting the top line. In the first quarter of fiscal 2024, total revenues of $3.3 billion included a 75-bps adverse impact of the wind-down of Canada operations. Although net sales for the Nordstrom banner rose 0.6% year over year in the reported quarter, the banner’s sales included a negative impact of 110 bps, owing to the wind-down of the Canada operations.

For fiscal 2024, management projects total revenues, including retail sales and credit card revenues, between a decline of 2% and an increase of 1%. The revenue guidance for fiscal 2024 includes a headwind of 135 bps from the additional 53rd week in fiscal 2023. The company expects fiscal 2024 comps between a 1% year-over-year decline and a 2% increase. Nordstrom envisions earnings per share of $1.65-$2.05, excluding share repurchase impacts.

Key Picks

Some better-ranked stocks are Abercrombie & Fitch ANF, The Gap Inc. GPS and Canada Goose GOOS.

Abercrombie, a specialty retailer of premium, high-quality casual apparel for men, women and kids, currently flaunts a Zacks Rank #1 (Strong Buy). ANF has a trailing four-quarter earnings surprise of 210.3%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for ANF’s current financial-year sales and earnings indicates growth of 10.4% and 47.3%, respectively, from the year-ago reported numbers.

Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. It sports a Zacks Rank #1 at present.

The Zacks Consensus Estimate for Gap’s current financial-year sales and earnings indicates growth of 0.2% and 21.7%, respectively, from the year-ago reported numbers. GPS has a trailing four-quarter earnings surprise of 202.7%, on average.

Canada Goose is a global outerwear brand. It currently flaunts a Zacks Rank #1. GOOS has a trailing four-quarter average earnings surprise of 70.9%.

The Zacks Consensus Estimate for Canada Goose’s current fiscal-year earnings indicates growth of 13.7% from the previous year’s reported figure. Meanwhile, the consensus estimate for the current fiscal year suggests flat year-over-year sales of $986.2 million.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

The Gap, Inc. (GPS) : Free Stock Analysis Report

Canada Goose Holdings Inc. (GOOS) : Free Stock Analysis Report