Yahoo Finance

Yahoo Finance Singapore Commercial Property Q12023 Rental Market Update

The commercial property market in Singapore comprises various segments such as office, retail, and industrial. They are tracked separately and may not be correlated to one another as they cater to different user needs.

Here’s what you need to know about the rental demand for the following three sectors, according to the latest Q12023 URA Real Estate Statistics and CBRE Research Singapore Figures.

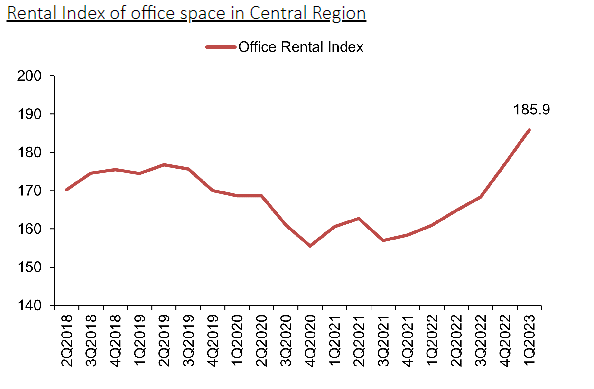

Office Sector: Rents Have Increased By 5.1% In Q12023 But Market Indicators Show Signs Of Moderation

Demand for office spaces was affected during the height of the COVID-19 pandemic in 2020–2021 as businesses switched to a work-from-home (WFH) setting. Eventually, demand recovered in 2022 as office workers were allowed to return to office settings in phases and due to the pickup in international companies like Amazon and Bytedance setting up offices in Singapore.

This strong demand in the buoyant office market was sustained from the previous quarter and led to another quarter-on-quarter (q-o-q) gain of 5.1% in Q12023, according to the URA Rental Index of Office Space in the Central Region.

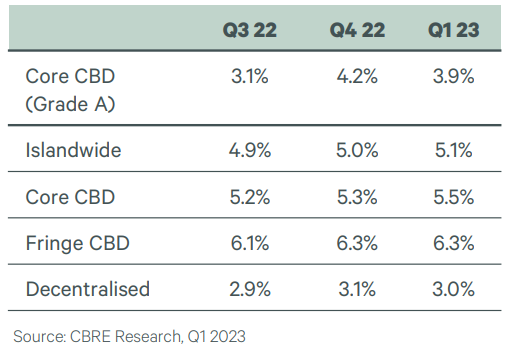

But this may not be indicative of the future demand for the office market for the rest of 2023. Based on the report by CRBE Research, Core CBD (Grade A) rose by 0.4% q-o-q to reach $11.75 psf/mth. This is slower than the 0.9% increase in the previous fourth quarter and the slowest since Q22021. On the other hand, Core CBD (Grade B) and Islandwide (Grade B), rose by 0.6% q-o-q to reach $8.55 psf/mth and $7.90 psf/mth, respectively.

The slowing demand is due to the technology sector, which has carried out large waves of retrenchment exercises in recent months. It alone accounts for about 80% of the shadow space—excess space on an existing lease agreement that the tenant would like to give up by finding a replacement tenant for the landlord.

Instead, the demand for leasing space in Q12023 was led by non-banking financial institutions, professional services, FMCG and government agencies, which were still expanding their headcount. But the sentiments of these occupiers might be turning more cautionary as the economy slows down and more news regarding the collapse of financial institutions such as Silicon Valley Bank and Credit Suisse surfaces.

Nevertheless, according to the CBRE Research report, Core CBD (Grade A) rents are expected to remain stable for the rest of 2023 due to the low supply of new office completions, which are 22% below the historical 10-year average.

Retail Sector: Consecutive Quarters Of Declining Rents As Retailers Face More Cost Pressures In 2023

The goods & services tax (GST) was raised from 7% to 8% in 2023, a move that was widely expected to affect retail sales in the initial months. Instead, retail sales (excluding motor sales) grew by 4.1% on a year-on-year (y-o-y) basis in March 2023 due to higher demand for food & alcoholic products and clothing & footwear.

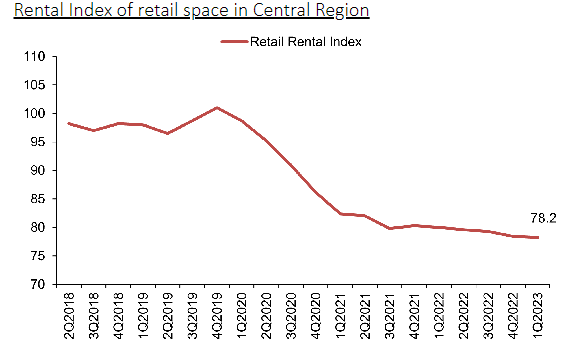

Despite the positive sales growth for the year, the URA Rental Index of Retail Space in Central Region continued to decline q-o-q with a drop of 0.3% in the Q12023. This is still better than the previous quarter’s drop of 1.1%.

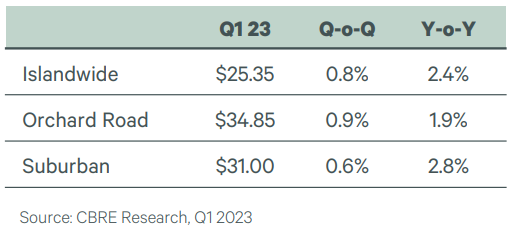

In contrast, the report by CBRE Research recorded a third consecutive quarter of increases in prime retail rents for all submarkets. The growth in rental rates of the retail space was led by the Orchard Road area, which saw a q-o-q increase of 0.9% to $34.85 psf/mth and islandwide prime rents, which, despite an increase of 0.8% q-o-q to $25.35 psf/mth, are still 8.5% lower than pre-pandemic (Q42019) levels.

The difference in the two sets of data could be because, unlike the URA Index, which tracks the records of retail space used for shop, food & beverage (F&B), entertainment and health & fitness purposes obtained from the Inland Revenue Authority of Singapore (IRAS), the CRBE Research looks at projects with a net lease area (NLA) of more than 20,000 sq ft.

CRBE Research expects further recovery in retail rents in 2023 with improved shopping activities, tourism, and below-historical-average new retail supply in the next few years. This is in spite of the further cost pressures that retailers may continue to face, such as a labour shortage, higher operational costs, a possible economic slowdown, and a further GST rate hike in 2024.

Industrial Sector: Strong Demand To Last For Storage Space, Particularly In The Prime Logistics Space

Businesses are facing a more challenging operating environment as a result of high inflation, rising interest rates, and a tight labour market. In fact, the OCBC SME Index, which tracks 11 business sectors and is used as a barometer of SME business health and performance, contracted in 1Q2023 after eight consecutive quarters of expansion.

Amidst this backdrop, rental demand for the industrial sector has remained resilient in Q12023. It was supported by leasing activities from the electronics, medical products and wholesale trade sectors. In particular, across the various segments, demand for storage space in modern developments, or prime logistics saw the biggest q-o-q increase of 3.7% to $1.68 psf/mth, according to the CBRE Research report.

It expects rental for prime logistics to be resilient in 2023, given close to full occupancy for three consecutive quarters and the lack of new prime logistics development for completion for the year. This comes as no surprise given the proliferation of e-commerce since the pandemic, which has sustained the demand from third-party logistics (3PLs).

The post Singapore Commercial Property Q12023 Rental Market Update appeared first on DollarsAndSense Business.