Yahoo Finance

Yahoo Finance Does Amtel Holdings Berhad (KLSE:AMTEL) Deserve A Spot On Your Watchlist?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Amtel Holdings Berhad (KLSE:AMTEL). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Amtel Holdings Berhad

Amtel Holdings Berhad's Earnings Per Share Are Growing

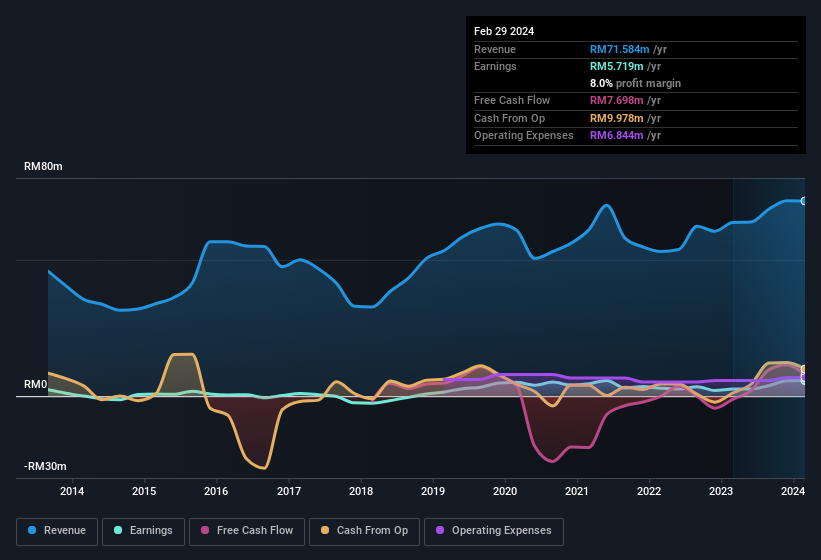

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Amtel Holdings Berhad managed to grow EPS by 4.5% per year, over three years. This may not be setting the world alight, but it does show that EPS is on the upwards trend.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. The good news is that Amtel Holdings Berhad is growing revenues, and EBIT margins improved by 3.4 percentage points to 10.0%, over the last year. Ticking those two boxes is a good sign of growth, in our book.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Amtel Holdings Berhad isn't a huge company, given its market capitalisation of RM58m. That makes it extra important to check on its balance sheet strength.

Are Amtel Holdings Berhad Insiders Aligned With All Shareholders?

Seeing insiders owning a large portion of the shares on issue is often a good sign. Their incentives will be aligned with the investors and there's less of a probability in a sudden sell-off that would impact the share price. So as you can imagine, the fact that Amtel Holdings Berhad insiders own a significant number of shares certainly is appealing. In fact, they own 44% of the shares, making insiders a very influential shareholder group. This should be a welcoming sign for investors because it suggests that the people making the decisions are also impacted by their choices. Valued at only RM58m Amtel Holdings Berhad is really small for a listed company. So this large proportion of shares owned by insiders only amounts to RM26m. That might not be a huge sum but it should be enough to keep insiders motivated!

It means a lot to see insiders invested in the business, but shareholders may be wondering if remuneration policies are in their best interest. Our quick analysis into CEO remuneration would seem to indicate they are. The median total compensation for CEOs of companies similar in size to Amtel Holdings Berhad, with market caps under RM943m is around RM496k.

The CEO of Amtel Holdings Berhad was paid just RM2.0k in total compensation for the year ending November 2023. This total may indicate that the CEO is sacrificing take home pay for performance-based benefits, ensuring that their motivations are synonymous with strong company results. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Should You Add Amtel Holdings Berhad To Your Watchlist?

One important encouraging feature of Amtel Holdings Berhad is that it is growing profits. The fact that EPS is growing is a genuine positive for Amtel Holdings Berhad, but the pleasant picture gets better than that. With company insiders aligning themselves considerably with the company's success and modest CEO compensation, there's no arguments that this is a stock worth looking into. You should always think about risks though. Case in point, we've spotted 1 warning sign for Amtel Holdings Berhad you should be aware of.

Although Amtel Holdings Berhad certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with more skin in the game, then check out this handpicked selection of Malaysian companies that not only boast of strong growth but have strong insider backing.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com