Yahoo Finance

Yahoo Finance Where BlackRock Goes, Liquidity Flows

News that BlackRock and Securitize are linking up to create a digital assets fund has major implications on regulated, compliant tokenization markets within the United States.

BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) is not the first of its kind to list on Securitize’s platform, but it’s likely the product that will catalyze institutional capital and serious money managers to the Securitize ecosystem.

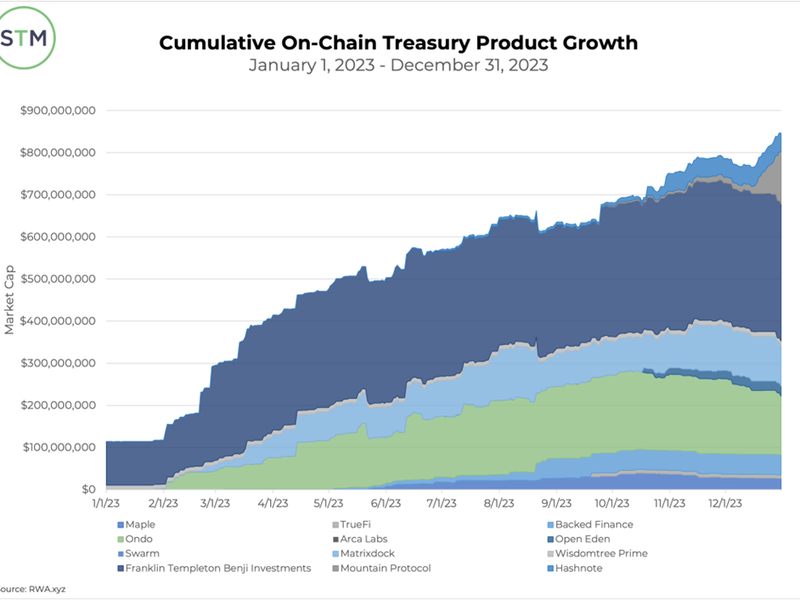

(BUIDL) will hold 100% of its assets in cash, U.S. Treasury bills, and repurchase agreements (repos), categorizing it as a digital money market product. Securitize previously and currently acts as the transfer agent and issuance platform for Arca’s US Treasury Fund (RCOIN). While Arca mapped out the vision and pioneered the blockchain-based structure for a traditionally ultra-liquid fund in 2020, BlackRock’s positioning here may provide the real spark this vision was aimed at.

You're reading Crypto Long & Short, our weekly newsletter featuring insights, news and analysis for the professional investor. Sign up here to get it in your inbox every Wednesday.

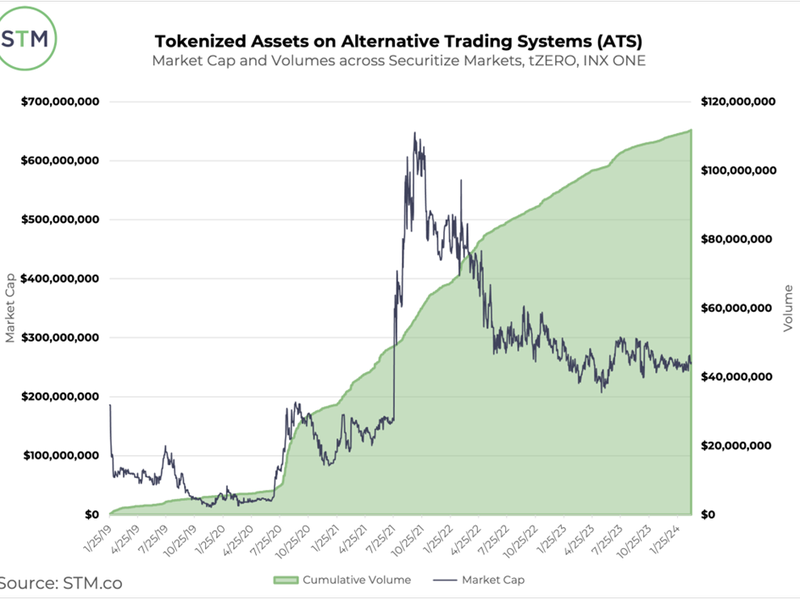

Per Security Token Market (STM.co) data, lifetime Alternative Trading System (ATS) volumes for tokenized assets reached $110+ million through March 2024. BlackRock’s $100 million BUIDL seed funding makes it the largest asset on Securitize, and Week 1 inflows of roughly $175 million already position BUIDL as the second-largest product in the money market cohort with $275 million in AUM behind Franklin Templeton’s $360+ million money market fund.

While limited to Qualified Purchasers (QPs) in the primary markets (defined as an estimated 2.7 million households with $5 million or more in investable assets or investment managers & corporations with $25 million in investable assets), eventual spillover to a secondary market listing will enable more desirable trading conditions to incentivize investors. BUIDL will prove itself to be a sticky asset enabling investors to collect yield while evaluating other listed alternative investments like Securitize’s listed KKR and Hamilton Lane funds and composing portfolios without ever leaving the platform once.

As Security Token Advisors detailed all 2023 in its State of Security Tokens report series, money markets and treasuries are the low-hanging fruit for asset managers to get familiar and comfortable with tokenization technology, partners, and the landscape. Other blue-chip money managers will see BlackRock’s liquidity fund as the gold standard to park capital in and get their own teams up-to-speed with regards to on-chain finance.

In fact, on March 27, 2024, Ondo Finance completed a $95 million reallocation of its own tokenized short-term bond fund to BUIDL. As fiduciaries onboard with Securitize for the desired access to BUIDL, they’ll move significant capital into the fund and therefore into the Securitize ecosystem. As a result, surrounding alternative investment products and listings on Securitize Markets’ primary and secondary trading venues are likely to see a bump in capital flows and activity. This in turn will set precedent for other broker-dealers, alternative trading systems, and comparable regulated venues in their issuer structuring and strategies.