Yahoo Finance

Yahoo Finance US$196 bil investment needed through 2034 for global carbon capture: Wood Mackenzie

Nearly US$80 billion has been committed to CCUS across five countries: US, UK, Canada, Denmark and Australia.

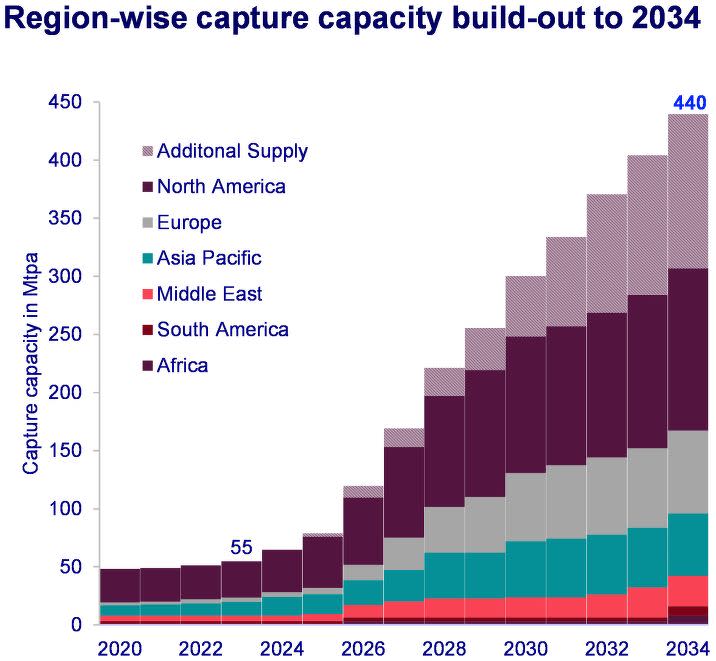

By 2034, global carbon capture capacity will reach 440 million tonnes per annum (Mtpa) and storage capacity will reach 664 Mtpa, requiring US$196 billion ($266.01 billion) in total investment, according to a new report from Wood Mackenzie, the global analytics firm for natural resources.

According to the June 26 report, titled “CCUS: 10-year market forecast”, nearly half of the investment globally is associated with CO2 capture, with the remaining US$53 billion from transport and US$43 billion from storage.

About 70% of the investment will be in North America and Europe across the value chain, says Wood Mackenzie’s APAC CCUS lead Hetal Gandhi. “This is a huge ramp-up from where the industry is today. Government funding plays a critical role in driving the first wave of CCUS investments.”

According to Gandhi, governments could offer capex grants, opex subsidies, tax incentives and contracts for differences for CCUS. “While no single mechanism has been used predominantly and each country devises novel methods to incentivise investments, nearly US$80 billion is directly committed to CCUS across five key countries,” she adds.

The US leads in funding at 50%, followed by the UK at 33% and Canada at 10%. Denmark and Australia round out the five “key countries”, according to Wood Mackenzie.

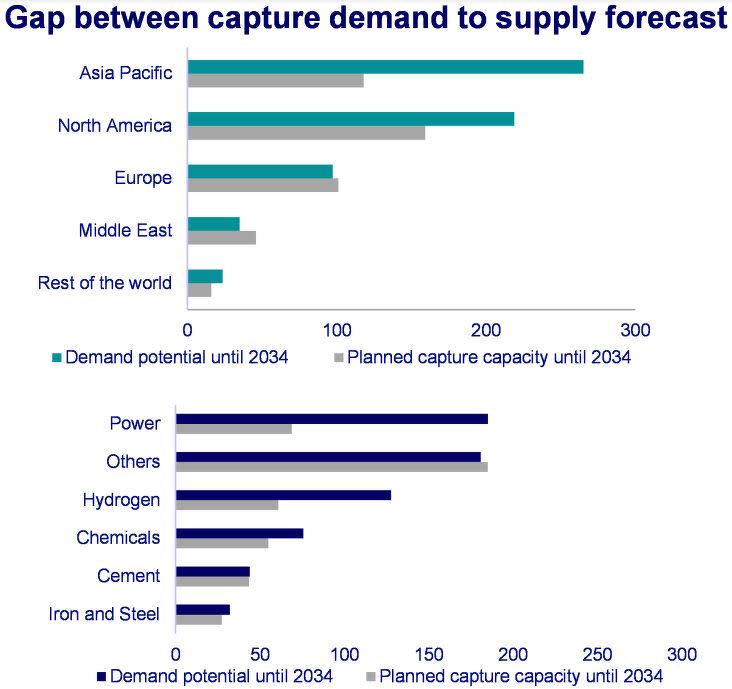

“While we are seeing strong support in countries like the US, government support in APAC lags behind,” said Stephanie Chiang, CCUS research analyst at Wood Mackenzie. “Australia, Malaysia and Indonesia have announced some benefits, but they are substantially lower as compared to their investment needs. Australia’s direct incentives at US$40 million is less than 1% of the investment needed over the next 10 years.”

In contrast, development in China, India, Latin America, the Middle East and Africa is limited by a lack of firm policy, regulatory frameworks and funding support, says Gandhi.

Ongoing debate

Wood Mackenzie’s analysts acknowledge that CCUS as a decarbonisation option continues to be debated. “Some insist it should be strictly an interim technology for hard-to-abate sectors including cement, chemicals, steel, refining and power generation,” writes Gandhi. “Others see it as a deep decarbonisation tool.”

Either way, for CCUS to fulfil its potential over the next 10 years, several conditions must be met, she notes. “To deploy CCUS at scale, heavy emitters must be motivated to decarbonise, the technology must be cost-effective and efficient, and a viable option for utilisation or storage must be available.”

Wood Mackenzie’s analysts list three milestones to watch in the coming decade.

The rise of emerging APAC hubs are the first checkpoint. Establishing hub infrastructure and ways to handle carbon import are complex, say analysts. “The speed with which these are ironed out for the emerging APAC hubs of Indonesia, Malaysia and Australia will be crucial over the next two years to galvanise new capacity announcements, project development and execution to reach the level of decarbonisation needed.”

Secondly, cross-border liabilities must be overcome. Bilateral agreements to enable cross-border CCUS, liability risk mapping, insurance obligations and risk definitions are a few crucial modalities to watch out for, say Wood Mackenzie’s analysts, as cross-border transport and storage hubs will play a bigger role in Europe and APAC.

Finally, transport infrastructure must improve. The actual buildout of transport infrastructure in Europe and North America — the former characterised by inter-country pipelines and shipping infrastructure and the latter by long and extensive pipeline requirements — will be key for projects of scale to materialise, say analysts.

Charts: Wood Mackenzie

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

Keppel, Pan-United to collaborate on CCUS, hydrogen development with energy and infrastructure firms

Dyna-Mac signs MOU with BW Offshore to pursue global carbon capture and storage projects

Get in-depth insights from our expert contributors, and dive into financial and economic trends