Yahoo Finance

Yahoo Finance Truist's (TFC) Business Restructuring to Aid Amid Cost Woe

Truist Financial TFC remains well-positioned for revenue growth on the back of decent loan demand, high rates, strategic restructuring initiatives and fee income growth. However, elevated expenses and weakening asset quality remain headwinds.

TFC’s net interest income (NII) growth seems encouraging. While the metric declined in the first quarter of 2024, it experienced a five-year (ended 2023) compound annual growth rate (CAGR) of 16.9% driven by decent loan demand, merger deals and increasing rates.

Its net interest margin (NIM) declined marginally in 2023 to 3%. While the current high interest rates are likely to have a positive impact on NII and NIM, higher funding costs will weigh on both.

We project NII to decline 2.9% in 2024 with a subsequent recovery of 5.2% and 3.8% in 2025 and 2026, respectively. Further, our projections for NIM are 2.94%, 3.03% and 3.10% for 2024, 2025 and 2026, respectively.

Truist Financial remains focused on non-interest revenue growth and its diversification. The metric experienced a 12.5% CAGR over the five-year ended 2023, primarily attributed to merger deals and solid wealth management and insurance businesses. The uptrend continued in the first quarter of 2024. While we estimate total non-interest income to decline in 2024 on account of securities losses to be incurred in the second quarter due to balance sheet repositioning, the metric is expected to witness pronounced growth in 2025.

Management remains optimistic about pursuing strategic business restructuring initiatives to realign and simplify operations. This is reflected by the completion of the divestiture (remaining 80% stake) of the insurance subsidiary Truist Insurance Holdings (“TIH”) in May 2024. In April 2023, it divested 20% of its stake in TIH. In February 2024, the company announced a deal to sell its asset-management subsidiary, Sterling Capital Management LLC.

As of Mar 31, 2024, Truist Financial’s total debt was $65.4 billion (with 40% being short-term in nature) and cash and due from banks were $5 billion. The company enjoys investment grade issuer ratings of A-/A-2 and A/F1 from S&P Global and Fitch Ratings, respectively, as of May 8, 2024, enhancing its accessibility to the debt market. Thus, the company is likely to address its debt obligations in the near term, even in the event of economic turmoil.

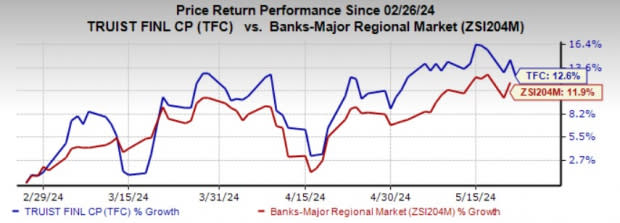

Truist Financial currently carries a Zacks Rank #3 (Hold). Over the past three months, shares of the company have rallied 12.6%, outperforming the industry’s growth of 11.9%.

Image Source: Zacks Investment Research

Nevertheless, the persistent increase in total operating expenses remains a concern. Expenses rose at a CAGR of 25.4% over the last five years (2018-2023). The rise was primarily due to an increase in personnel expenses, the company’s efforts to enhance digitization and the merger deal between BB&T Corp and SunTrust Banks. While expenses declined in the first quarter of 2024, the overall expense base is anticipated to remain high, primarily attributed to ongoing technological upgrades. While we estimate total adjusted non-interest expenses to remain stable in 2024, the same is projected to rise 2.5% in 2025.

Truist Financial’s worsening asset quality is another major headwind. Provision for credit losses witnessed a 30.1% CAGR over the five years ended 2023. While the provisions declined in the first quarter of 2024, an uptrend in the metric is likely because of an expected economic slowdown. We estimate the provision for credit losses to rise 4.3% in 2024.

Banking Stocks Worth Considering

Some better-ranked major bank stocks worth a look are Northern Trust Corporation NTRS and Wells Fargo & Company WFC.

Estimates for NTRS’s current-year earnings have been revised marginally downward in the past week. The company’s shares have increased 10.2% over the past six months. Currently, NTRS sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

Estimates for WFC’s current-year earnings have been revised marginally upward in the past 30 days. The company’s shares have risen 42.4% over the past six months. Currently, WFC carries a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

Northern Trust Corporation (NTRS) : Free Stock Analysis Report

Truist Financial Corporation (TFC) : Free Stock Analysis Report