Yahoo Finance

Yahoo Finance Texas Pacific Land: An Atypical Real Estate Growth Stock

I usually do not start with the history of a company to present my investment thesis, but Texas Pacific Land Corp. (NYSE:TPL) is such an atypical enterprise that it is better to start from the beginning. Its historical background explains its current business model.

Founded in 1871, Texas and Pacific Railway Company was created through a federal charter to build a railway that would link East Texas to the Pacific Ocean in California, crossing Arizona and New Mexico. The company never completed the full line and had to file for bankruptcy in 1888. As a way to compensate the bondholders that invested in the railroad, the vast amounts of land (3.50 million acres in Texas) were put in a public trust for the benefit of these bondholders.

The trust was later named Texas Pacific Land Trust, which is now known as Texas Pacific Land Corp. A few decades later, the first oil well was drilled (1920) and again many decades later (2010), lands owned by the trust were going to be the subject of an oil production revolution: shale oil extraction. It is no coincidence that the stock price started to rise in 2010.

The company's business model is, simply put, the holding of strategic lands and receiving royalties on every economic activity that happens on these properties.

Investment thesis

Texas Pacific Land is often wrongly considered an energy company. While it derives most of its revenue from oil and gas production, the company does not produce a single barrel of it. It is first and foremost a real estate company that holds vast amounts of land across Texas, particularly in the oil-rich Permian Basin.

The Permian Basin is the highest-producing oil field in the United States with 1.60 million barrels of oil produced per day. It holds an estimated 50 billion barrels of oil, the second largest in the world. It previously had been in decline since the 1970s, but unconventional oil production methods (i.e., fracking) have boosted shale oil extraction in the region since 2010.

The company makes its revenue from a variety of sources: fixed-fee payments for use of the land by tenants, revenue for sales of materials used in the construction of infrastructure, provision of sourced water or treated produced water, revenue from oil and gas royalty interests and revenue related to saltwater disposal on its land. Texas Pacific Land also generates revenue from all types of infrastructure projects on its properties like solar and wind installations.

Further, it has no competition and its moat (ownership of lands rich in resources) is here to last essentially forever. As Warren Buffett (Trades, Portfolio) said, When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever. Texas Pacific Land is truly one of those stocks that, from my point of view, every long-term portfolio should hold some exposure to with a forever time horizon.

The royalties received on every barrel produced on the 880,000 acres it owns in the Permian Basin, the high growth of its water business, the ultra-high financial margins and the shareholder-friendly management make the stock an unavoidable one in a long-term, growth-oriented portfolio.

Two distinct business lines

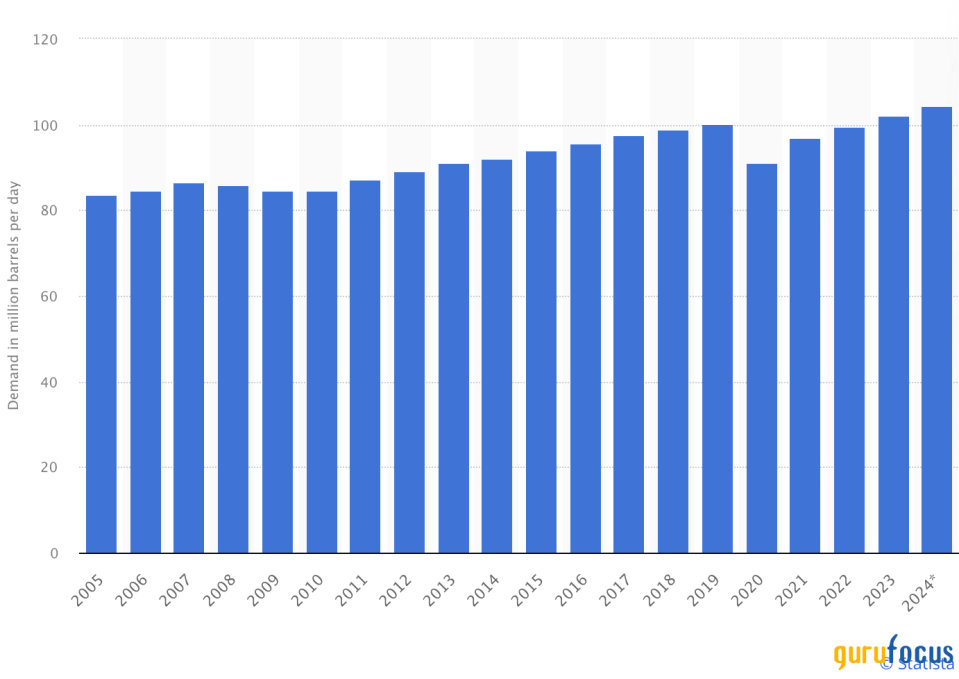

Texas Pacific Land has two distinct business lines through which it collects royalties and fees. The company makes a large portion of its revenue by lending land to reliable and growing oil-producing tenants like Exxon Mobil Corp. (NYSE:XOM), Chevron Corp. (NYSE:CVX) and EOG Resources Inc. (NYSE:EOG). Global oil demand has witnessed a rather steady rise over the last decade and, even if the demand in developed countries were to weaken, the rapid demand increase in emerging markets ensures a continued uptrend in oil demand and production.

Global Crude Oil Demand. Source: Statista

Texas Pacific Land's revenue is somewhat correlated to the U.S. and global demand for fossil fuels and oil price, although it does not produce any oil and gas directly. In a way, this allows the company to participate in the upside (increased royalties) without suffering as much as these oil producers when demand weakens because it still receives fees for the lease of the lands and royalties on a number of different economic activities occurring on the lands it holds.

And one business line in particular is promising: its water business (production, treatment and desalination). Indeed, TPL announced in the last earnings release on May 8 an increase in revenue of $27.70 million (18.90% total revenue increase) from the first quarter of 2023 to the first quarter of 2024. All revenue streams increased year over year, but the $15.40 millionn increase in water sales was the biggest contributor, representing more than half of the company's revenue growth.

Texas Pacific Land continues to invest in its water business with the development of new energy-efficient technologies, the construction of a facility with an initial capacity of 10,000 barrels of water per day and even filed an application patent for a water desalination and treatment process. In the meantime, oil and gas royalty revenue increased by $3 million due to higher production volumes in the first quarter of 2024 compared to the first quarter of 2023, which clearly indicates the water business line is where the high growth potential lies.

A pristine balance sheet justifies an expensive valuation

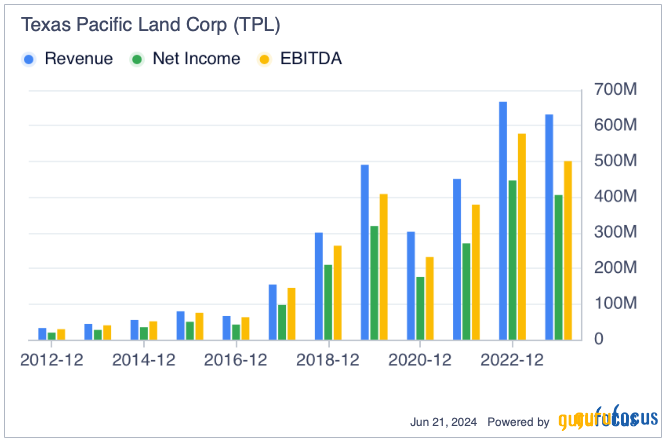

The balance sheet of Texas Pacific Land is pristine. The company currently has no debt and $837 million in cash. If we take a step back, we easily understand how the company's cash situation is the way it is; its operating margin (i.e., operating income relative to total revenue) has fluctuated between 72% and 96% since 2016, with the current operating margin standing at a whopping 78.50%. The high margin allowed the company to reach a free cash flow level of $114.5 million in the first quarter alone, significantly increasing its prior cash amount.

This stock might not be a favorite of dividend investors due its low yield (currently around 0.60% based on the recently announced $1.17 per share payable on June 17). Texas Pacific Land prefers reinvestment in the business (e.g., development of technologies useful for the water business unit, which contributed to the growth we discussed in water sales) and share buybacks over dividends. As an investor holding the stock as one of my top positions for the long term, I prefer the company reinvest in the business and continue buying back shares because both aspects have the highest impact on the stock price over the long term. Paying too high a dividend might cause the company to end up trapped in meeting the dividend payments, in a way similar to Verizon Communications Inc. (NYSE:VZ) with limited stock price appreciation over the years.

The valuation of the stock is currently not the most attractive given the recent price rally from $582.07 on June 7 to $777.27 on June 12 (33.50% gain in five trading days) after excellent earnings news. At the time of writing, it was trading around 40 times earnings, up from 30 times earnings before the recent rally. It is difficult to time the market, but it could make sense to keep accumulating shares while the stock cools down to 35 times earnings (the average historical valuation of the stock). However, given the high financial growth profile of the company (average revenue growth of 40% per year in the last 10 years), I have very little doubt the financials of the company in the coming quarters will automatically readjust the valuation without the stock having to pull back.

Given the high margins and growth profile of Texas Pacific Land, starting or continuing to accumulate shares today will likely prove to be a profitable move over the medium and long term.

Risk factors to my case

There are always risks to an asset, even though the company has high margins and low competition.

One of the key risks is energy demand in the United States. If oil demand and production fade in the U.S. due, for example, to the energy transition, the royalties received by Texas Pacific Land would also decrease. The royalties received for its lands could also sharply decline in the case of a prolonged recession, induced by the tight monetary policy of the Federal Reserve. There is an interesting caveat here, however; the company receives royalties on all types of economic activity on its lands, including infrastructure projects and renewable energy projects. In the case of an energy transition, Texas Pacific Land would continue benefitting from green energy demand because its lands are ideally located for solar and wind energy production.

Another key risk is when business becomes too easy. Although there is no competition possible on its own lands, it is possible that, when things become too easy for management thanks to high margins, the management team may be inclined to rest on its success rather than continue to aggressively pursue the growth and efficiency paths it has been on over the years.

For now, though, there is no indication management's interests are not strictly aligned with shareholders. The company loves share buybacks and still has roughly $200 million worth of repurchases remaining on its current buyback authorization. The last earnings call also proved management continues to reinvest in new technologies and pilot programs to support growth.

Bottom line

Texas Pacific Land is an attractive stock to buy and hold for any investor that has a long-term growth portfolio, but may not be as attractive for dividend investors. The company has a unique moat that allows it to virtually have no competition.

The stock is particularly attractive given its high margins and high growth rates, while at the same time allowing investors to have indirect exposure to several sectors at the same time, namely real estate, oil, renewable energy and infrastructure. The current valuation might be a bit expensive, yet a pullback might not be necessary to justify a buy today. Indeed, it is likely the company's financial growth will itself reduce the multiples at which it is trading given the company's ability to support continued growth.

This article first appeared on GuruFocus.