Yahoo Finance

Yahoo Finance Suntec REIT’s manager raises $94.4 million in strata sales at Suntec, prefers divestments to EFR to lower gearing

Suntec REIT's manager looks to divest core plus property in Australia or Suntec's strata units to lower aggregate leverage to 40%

Suntec REIT’s headline distributions per unit (DPU) look underwhelming for FY2023, with a 19.3% y-o-y decline to 7.135 cents. In FY2019, before Covid, Suntec REIT’s DPU was 9.507 cents. For FY2023, DPU from operations fell by 21.6% y-o-y to 6.341 cents. DPU was topped up to 7.135 cents from gains from the sale of a property (Park Mall) in 2015. These gains have been largely distributed.

Chong Kee Hiong, CEO of Suntec REIT’s manager has a stated strategy to bring the REIT’s aggregate leverage of 42.4% as at Dec 31, 2023, down to 40%. (Suntec REIT’s aggregate leverage is within 45% for its interest coverage ratio (ICR) of 2x.) Still, Chong would be more comfortable with a lower aggregate leverage.

Suntec REIT’s ICR includes the impact of its two tranches of perpetual securities issued in 2020 and 2021. In previous briefings, Chong had expressed a wish to improve Suntec REIT’s ICR and states that equity fund raising is unlikely to be an option for the REIT.

One way to lower gearing is to divest strata-titled units at Suntec’s office towers. During 2023, Suntec REIT raised $94.4 million from the sale of strata-title units, at an average of a 31% premium to book value.

When asked if Suntec REIT could top-up DPU with gains from the sale of Suntec’s strata units, Chong says: “We have to look at [the gains] on a case by case basis. We’ve made divestment gains but the interest rate cycle is still uncertain. Gearing is still high, so we will take it one step at a time.”

Suntec REIT’s manager is expecting average cost of debt to remain at its current level of 4.2%. Although the interest rate cycle may have peaked, with base rates and margins easing, in 2024, the REIT has interest rate hedges dropping off that it entered into during the low rate environment and these would inevitably cost more.

In view of the rate cycle, Chong would like to divest one of the Australian office buildings if possible. However, liquidity and financing are limited down under for large transactions and actual selling prices of buildings may well be lower than valuations for these large transactions. “Transactions are at about 20% to 25% off their last valuations. There is a gap between valuation and transaction prices,” Chong notes.

In FY2023, Australia contributed 18% to the REIT’s income, and accounted for 14% of AUM. Operationally, NPI from its Australian properties was 9.5% lower y-o-y in 2HFY2023, and 14.3% lower in Singapore dollars.

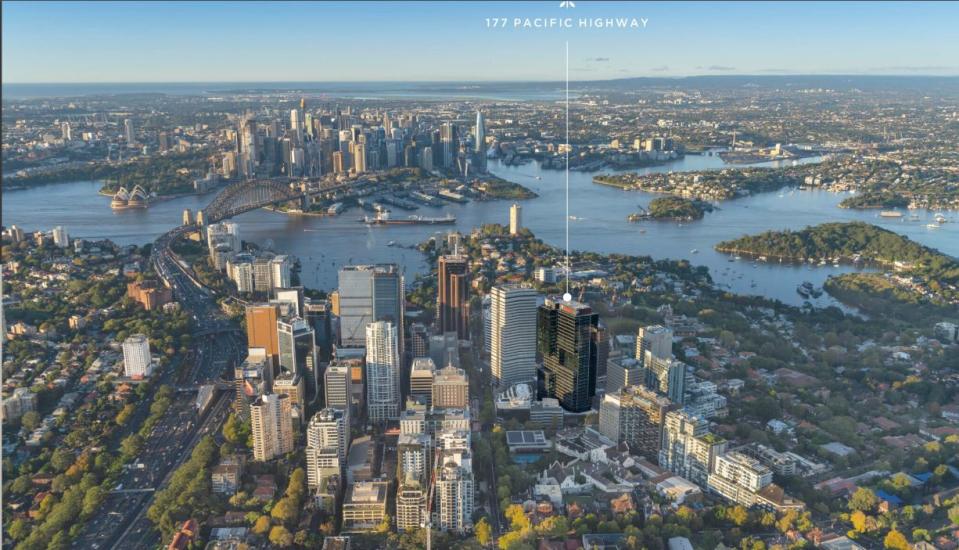

The Australian portfolio, valued at $1.72 billion as at Dec 31, 2023, is down 5.3% y-o-y in Singapore dollars. The portfolio comprises five buildings, 177 Pacific Highway in Sydney, Southgate Complex Melbourne, 477 Collins Street Melbourne, 35 Currie Street Adelaide and 21 Harris Street Sydney.

Chong has classified the Australian portfolio as core and core-plus. Core represents the properties Suntec REIT plans to hold on to while the manager would be willing to part with core-plus properties. Among them, 477 Collins Street is viewed as core; 21 Harris Street is fully occupied and core as is 177 Pacific Highway.

At present, only the 50% stake in Southgate Complex in Melbourne is core-plus. At a valuation of $328.2 million as at Dec 31, 2023, Southgate is one of two Australian properties that is valued above its purchase price of $200.8 million in 2016. The other is 177 Pacific Highway which was last valued at $618.6 million compared to its purchase price of $457.5 million. The other three buildings were valued below their purchase prices, a result of a combination of higher capitalisation rates and a stronger Singapore dollar.

Notable among the properties which were valued lower y-o-y and compared to the purchase price is 55 Currie Street, whose occupancy is below average at 87.3%, Chong appears reluctant to classify it as core-plus because when fully occupied and stabilised, its yield is 7.5%.

While large transactions are absent, the Australian press has reported some bite-sized deals. Cromwell Property Group is reported to have agreed on the sale of 2-6 Station Street for about A$48m to private company Sandran Property

In North Sydney, AEW Capital has agreed to sell a 14-storey office block at 54 Miller Street for A$72 million. CBRE reports that a Hong Kong high net worth individual bought the building. AEW acquired the building for A$59.4 million in 2018 and repositioned it.

CBRE reported that the most significant deal for in 3Q2023 was 1 Margaret Street in Sydney, which was sold by Dexus to Quintessential Equity for A$296 million.

According to JLL Research, the most significant sales for 3Q2023 across all sectors was the divestment of a 50% interest in 20 prime industrial assets to UniSuper for A$560 million, Midland Gate Shopping Centre (Western Australia) for A$465 million, 7 Spencer Street (Victoria) for A$313 million, 44 Market Street (NSW) for A$393.1 million, 1 Margaret Street (NSW) for A$296 million and 189 Kent Street (NSW) for A$200 million.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

Lippo Mall Indonesia Retail Trust sees aggregate leverage increase to 44.3%

For S-REITs, acquisitions and hints of acquisitions have undermined prices

PhillipCapital initiates ‘buy’ on Suntec REIT, calling it ‘the discounted gem’

Get in-depth insights from our expert contributors, and dive into financial and economic trends