Yahoo Finance

Yahoo Finance 'Stable NIMs' expected for Asean banks, OCBC is UOBKH's top pick here

UOB Kay Hian Research analysts are maintaining “overweight” on Singapore and Indonesian banks ahead of quarterly results.

Growth in Asean’s banks is supported by foreign direct investment (FDI) inflows, which are already above pre-pandemic levels, say UOB Kay Hian Research analysts Jonathan Koh, Keith Wee, Kwanchai Atiphophai and Posmarito Pakpahan.

Ahead of quarterly results reporting season, the region’s banks are expected to post stable net interest margins (NIMs), add the UOBKH analysts, as central banks have completed their rate hike cycles but are maintaining interest rates at current elevated levels in the near term.

In particular, the analysts are maintaining “overweight” on Singapore and Indonesian banks, while maintaining “market weight” on those in Malaysia and Thailand, where the formation of a new government in the latter country is a positive for banks there.

In Singapore, the “higher for longer” narrative is gaining traction, write the UOBKH analysts in an Oct 6 note.

US GDP expanded by a resilient 2.1% in 2Q2023 (seasonally adjusted annual rate). Crude oil prices have been rising since Saudi Arabia and Russia imposed voluntary cuts in crude oil production in July. US Consumer Price Index (CPI) accelerated to 0.6% m-o-m, driven by energy prices in August.

The Fed left interest rate unchanged during the FOMC meeting on Sept 20, but is likely to hike Fed Funds Rate by another 25 bps on Nov 1, says UOBKH. “It is expected to hold interest rates at restrictive levels until inflation moves sustainably lower towards the objective of 2%. Banks benefit from resilient NIM as interest rates stay higher for longer.”

The resultant “higher for longer” narrative caused 10-year Singapore government bond yield to expand 32 basis points (bps) to 3.40% in 3Q2023.

Competition for fixed deposits has, however, eased with interest rates for fixed deposits currently at 2.7% compared to 3.9% at end-2022.

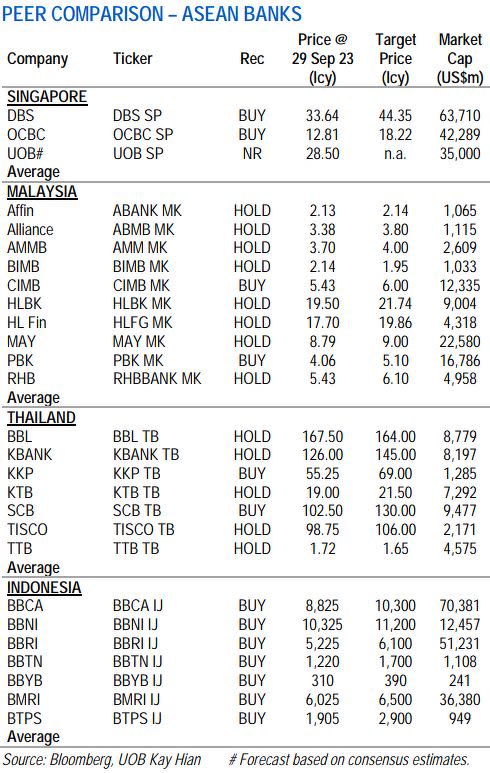

Banks’ share prices were lifted higher with DBS and Oversea-Chinese Banking Corporation (OCBC) gaining 6.7% and 4.6% respectively. Among the three local banks, UOBKH prefers OCBC, keeping “buy” with a target price of $18.22.

Banks provide low price-to-book (P/B) of 1.13x and “sustainably” high yield of 6.2% for 2024, they add. DBS and OCBC have potential to return surplus capital to shareholders as their current common equity tier-1 (CET-1) ratios of 14.1% and 15.4% are above their preferred operating range of 12.5%-13.5%.

UOBKH prefers OCBC for its new dividend policy with payout ratio at 50%, focus on Asean and a “defensively low” 2024 P/B of 1.03x.

Mixed trends in Malaysia

In Malaysia, loan applications increased by 7.8% y-o-y in August, in contrast to a 6.6% decrease in July. However, loan approvals decreased by 7.7% y-o-y vs a 0.5% increase in July.

Meanwhile, current system loan growth of 4.1% is trending slightly below UOBKH’s full-year 2023 estimates of 4.5%.

All eyes are on the Malaysian banks’ NIMs, note the UOBKH analysts. “Despite the Overnight Policy Rate (OPR) having normalised upwards to pre-pandemic levels, the sector's average NIM of 2.04% in 2Q2023 remains below the pre-pandemic range of 2.10%-2.20%.”

While UOBKH anticipates a modest NIM recovery in 4Q2023, several factors are expected to limit further improvement in 2024. These include no expected OPR hikes, competition in deposits from digital banks, and the potential for further normalisation of the current accounts and savings accounts (CASA) ratio from 29% to the pre-pandemic average of 26%.

The UOBKH analysts have factored in a stable NIM trend in 2024 compared with 2023. NIMs are predicted to remain flattish with downside risks, while loan growth is expected to slow down.

That said, the sector’s dividend yields are attractive, surpassing 5%, they add. “Credit costs are anticipated to decrease, albeit at a modest rate. We like Public Bank, [with a] target price of RM5.10 ($1.47), for its high provision buffers providing scope for potential provision write-backs when macroeconomic conditions permit and CIMB, [with a] target price of RM6.00, for strong earnings growth and proxy to potential emerging market inflows.”

Thailand’s rate hike cycle has ended

In Thailand, the rate hike cycle has come to an end, say UOBKH analysts. The Bank of Thailand (BOT) made an unexpected move to increase the policy rate by 25 bps to 2.5% in September, justifying its decisions based on future economic outlooks.

BOT expressed confidence in the country's economic prospects for 2024, projecting a GDP growth of 4.4%, up from the previous estimate of 3.8%. This anticipated growth is largely fuelled by government spending. BOT indicated that the current policy rate of 2.5% is likely to remain stable for the foreseeable future.

That said, UOBKH expects Thai banks to post q-o-q declines in 3Q2023 earnings. “We expect Thai banks to report aggregate net profit of Bt47b in 3Q23, up 4% y-o-y but down 11% q-o-q. The q-o-q decline is primarily attributed to a significant increase in credit costs, brought about by weaker-than-expected economic recovery. Additionally, we project a q-o-q decrease in the sector's non-interest income in 3Q2023, largely driven by sluggish investment gains.”

On a positive note, the sector's NIM is expected to maintain its upward trend. UOBKH prefers SCB X, with a target price of THB130 ($4.80), given its laggard play in terms of share price performance, goal to raise return on equity (ROE) to 13%-15% in the next three to five years and plans to maintain a high dividend payout ratio. The bank’s last payout ratio was 60%.

Rising competition in Indonesia

Finally, Indonesia’s banks posted solid results in 2Q2023 by sustaining high ROEs, improving asset quality and maintaining robust capital adequacy ratios, says UOBKH.

Domestic economic recovery drove high-single-digit loan growth and supported further decline in credit costs, despite higher interest rates putting pressure on cost of funds, they add. Digitalisation and enhanced economies of scale helped banks to control their opex. All in all, the combined profit of the big four banks was flat q-o-q but grew 17.8% y-o-y.

That said, UOBKH points to rising competition to gather third-party funds. Loan to deposit ratio (LDR) gradually rose to 85.7% in August as loan growth outpaced deposit growth.

With current reserve requirement (GWM) of 9%, banks are facing rising competition to gather third-party funds, they add. The time deposit rates increased across all tenors by 168.2 bps y-o-y and 53.6 bps year to date on average.

UOBKH believes Bank Indonesia could lower GWM before cutting rates as LDR gradually increases above 90% and inflation declines.

Nevertheless, earnings will continue to grow, they add. “We expect banks to deliver 19.7% y-o-y net profit growth this year despite pressure on cost of funds. Underpinned by domestic manufacturing optimism and more government spending in 2H2023, loan growth will remain expansive. Political campaign for the 2024 election will start in November, which should support the purchasing power of the low-income class.”

There, UOBKH prefers Bank Rakyat Indonesia (Persero) (BBRI) with a target price of 11,200 rupiah (98 cents).

Shares in OCBC closed 10 cents higher, or 0.78% up, at $12.85 on Oct 6.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

As bulls and bears remain asleep, stay put in high-yield and non-cyclical counters

UOBKH touts 'blue-chip S-REITs' CICT, FLT and MINT as rates may stay higher for longer

Get in-depth insights from our expert contributors, and dive into financial and economic trends