Yahoo Finance

Yahoo Finance Reasons to Retain DexCom (DXCM) Stock in Your Portfolio for Now

DexCom, Inc. DXCM is well-poised for growth in the coming quarters, backed by its strong product portfolio. A robust first-quarter 2024 performance, along with a series of favorable coverage decisions, is expected to contribute further. However, risks related to stiff competition persist.

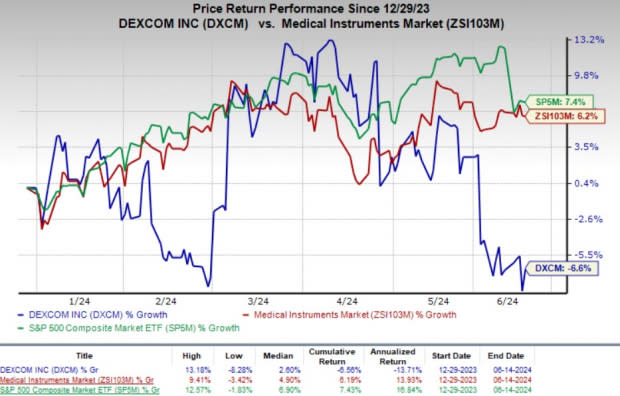

This Zacks Rank #3 (Hold) company’s shares have lost 6.6% year to date against the industry’s 6.2% growth. The S&P 500 Index has increased 7.4% in the same time frame.

DXCM, a renowned medical device company and provider of continuous glucose monitoring (CGM) systems, has a market capitalization of $46.11 billion. It projects 22.9% growth over the next five years and expects to maintain a strong performance going forward.

DexCom’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 34.1%.

Image Source: Zacks Investment Research

Let’s delve deeper.

Strong Product Demand: We are upbeat about DexCom's continued strength in its CGM products.

The company continues to expand its product portfolio with the addition of new products like G7 in 2023 and One+ in February 2024. These have helped accelerate its growth. Sales of G7 reflect strong demand since its launch late last year.

Moreover, the expansion of coverage for CGM systems during the quarter supported growth. This trend is likely to continue in 2024 as well. The availability of new sensors like G6 and G7 in new international markets is also boosting revenue growth. DXCM launched its latest sensor, G7, in more than 15 countries in 2023. Moreover, the company is focusing on connecting its CGM sensors with automated insulin delivery systems worldwide. This may boost the sensors’ demand going forward.

Additionally, the glucose monitoring market presents significant commercial opportunities for the company. DexCom’s prospects in alternative markets such as non-intensive diabetes management, hospital, gestational, pre-diabetes and obesity are likely to provide it with a competitive edge in the MedTech space.

New Product Launch: Earlier this month, DexCom announced the direct connectivity of the G7 CGM system with the Apple Watch. This added feature is now available to users in the United States, the UK and Ireland, with additional markets launching the feature soon.

In March, DexCom received FDA approval for its new glucose sensor, Stelo, designed specifically for people with type II diabetes who do not use insulin. The device has been approved for over-the-counter availability. The company expects to launch the sensor in the U.S. market during the summer of 2024. The device is likely to be a key growth driver for the company in 2024. In February, DexCom launched its latest CGM system, Dexcom ONE+, which is simple to use and lowers the entry hurdle to diabetic technology. It aims to deliver a highly effective CGM experience to people treating type 1 or type 2 diabetes with insulin.

Positive Coverages: DXCM’s G6 and G7 sensors have received extensive coverage in the United States during the last year, raising our optimism. The Centers for Medicare & Medicaid Services’ decision to expand coverage for all people using insulin and certain non-insulin-using individuals who struggle with hypoglycemia in 2023 paved the way for greater commercial coverage for these populations. This decision strengthened the company’s position as the most covered CGM in the United States.

The company’s G7 CGM System is already covered by all major pharmacy benefit managers in the country. The DexCom One+ is also available in Europe under a reimbursement policy. On its first-quarter earnings call, DexCom stated that the extensive coverage for its CGM devices has led to the rising demand for the devices.

Strong Q1 Results: DXCM’s strong first-quarter revenues buoy optimism. The company’s earnings per share improved 88.2% year over year to 32 cents, while revenues were up 24% at $921 million. Dexcom raised the lower end of its guidance during the quarter. It now expects total revenues to be in the band of $4.2-$4.35 billion for 2024, implying organic growth of 17-21% year over year.

Impressive contributions from the Sensor segment, and domestic and international revenue growth were the key catalysts. Additionally, the glucose monitoring market presents significant commercial opportunities for DXCM.

Downsides

Rising Costs: The company’s gross margin contracted 160 basis points year over year during the first quarter to 61.8%, reflecting the rising cost of sales.

Stiff Competition: The market for blood glucose monitoring devices is highly competitive, subject to rapid changes and new product introductions. DXCM’s competitors manufacture and market products for the single-point finger stick device market and collectively account for the worldwide sales of self-monitored glucose testing systems at present.

Estimate Trend

DexCom is witnessing a flat estimate revision trend for 2024. In the past 30 days, the Zacks Consensus Estimate for earnings per share has been stable at $1.78 for 2024.

The consensus mark for the company’s second-quarter revenues is pegged at $1.04 billion, indicating a 19% improvement from the year-ago quarter’s reported number. The same for earnings is pinned at 39 cents per share, implying growth of 14.7% year over year.

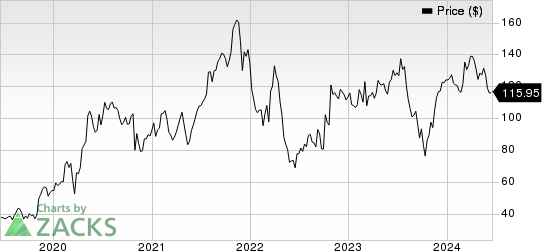

DexCom, Inc. Price

DexCom, Inc. price | DexCom, Inc. Quote

Stocks to Consider

Some better-ranked stocks in the broader medical space are DaVita Inc. DVA, Boston Scientific BSX and Hologic HOLX.

DaVita, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 13.6%. Its earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 29.4%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

DaVita’s shares have risen 34.7% compared with the industry’s 7.9% growth year to date.

Boston Scientific, carrying a Zacks Rank of 2 at present, has an estimated earnings growth rate of 12.5% in 2024. Its earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 7.49%.

BSX’s shares have risen 32.8% year to date compared with the industry’s 3.1% growth.

Hologic, carrying a Zacks Rank of 2 at present, has an estimated long-term growth rate of 7.4%. Its earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 4.94%.

Hologic’s shares have risen 0.5% year to date compared with the industry’s 6.2% growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

DexCom, Inc. (DXCM) : Free Stock Analysis Report