Yahoo Finance

Yahoo Finance The private equity machine will be tough to unjam

The stock markets have been more or less closed to IPOs of private equity companies for 18 months now

High finance has hit a low. Investment banking work has all but dried up and the private equity industry bears a lot of the blame. The bad news for those involved is that managers of buyout funds might struggle to get their flywheels spinning again even when the current economic uncertainty starts to clear up.

Private equity has been a huge driver of investment banking revenue over the past 10 years because of its regular cycles of buying, selling and refinancing companies. At Goldman Sachs Group Inc., for example, more than 30% of global investment banking fees came from private equity related work in recent years, compared with less than 20% a decade ago.

Some bankers are starting to think that the golden age is over for the buyout industry, which was supercharged by plentiful and cheap debt as central banks suppressed volatility in financial markets with ultra-low interest rates and quantitative easing.

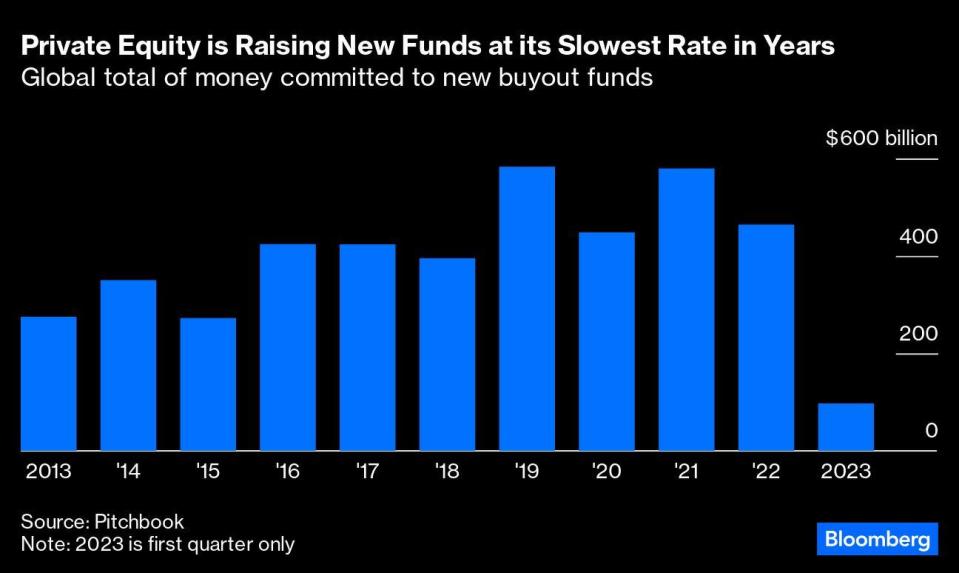

In the past 12 months, the industry has hit a sand trap. New deals and exit sales have dropped off a cliff. Initial public offerings on stock markets have almost completely disappeared. New fundraising has become extremely difficult with even big names such as Apollo Global Management and BC Partners Holdings failing to reach targets for recent funds.

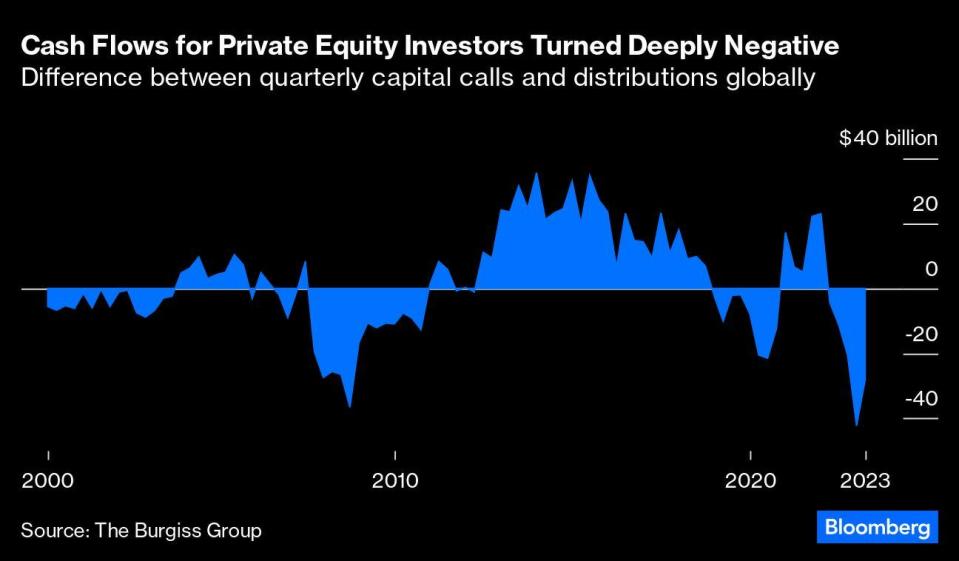

The biggest problem is that private equity investors keep being asked to put cash in while getting little money back. When the firms raise funds, their investors (known as Limited Partners) make a commitment to give managers cash when it’s needed to do deals. The difference between capital calls, when LPs hand over the money, and distributions, when they get dividends and investment profits back, turned sharply negative last year. In the third quarter of 2022, LPs experienced a greater negative cash flow even than in the worst quarter of 2008, according to data from The Burgiss Group LLC, a specialist research firm.

The stock markets have been more or less closed to IPOs of private equity companies for 18 months now, according to data from Dealogic. The recent US listing of restaurant chain Cava Group, which is trading at nearly double its offering price, raised hopes it could reopen. However, two other IPOs last week, Kodiak Gas Services Inc. and Fidelis Insurance Holdings Ltd., both fell on their first day of trading.

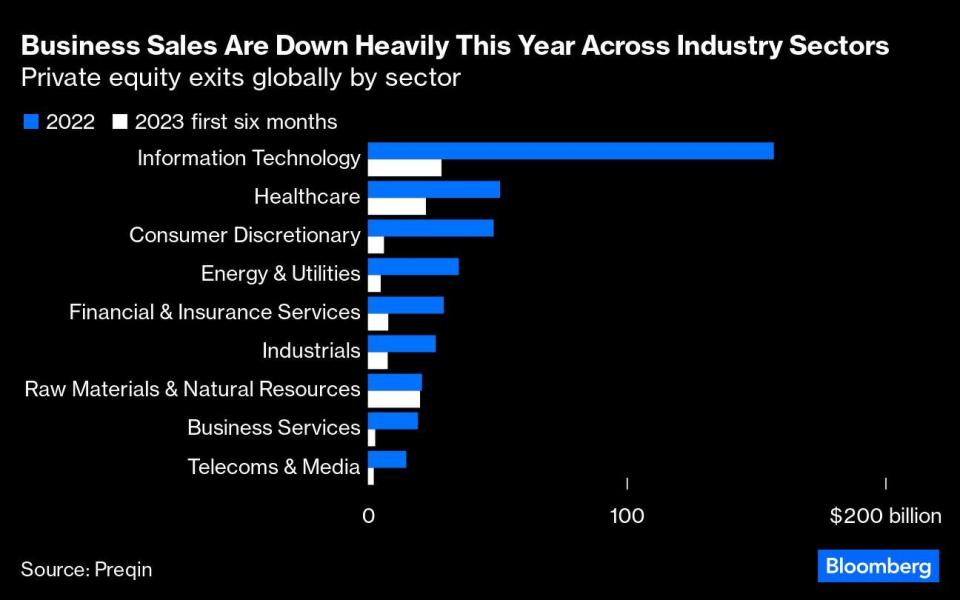

Secondary sales, where private equity funds sell companies to each other, have also slowed dramatically since 2021, according to data from Preqin. That was initially due to a collapse in the market for risky loans to fund such deals, but now is being held back by disagreements over company valuations. Strategic sales to other companies — like the Nasdaq and IBM deals — have held up better, but are still much slower than in 2021.

Private equity deal making faces two big problems. It is hard to value companies and work out what debt they can bear while interest rates are still moving. The good news is that central banks’ rate-raising cycles might be coming to an end, which should make it easier to agree new buyouts.

The second problem is longer-term: Many of the companies that funds already own were loaded up with floating-rate debt before inflation became a problem. The rising cost of that debt is eating up more of their potential profits, especially since private equity owners stopped hedging interest-rate risks. Unless rates start to fall again, those companies are going to have to work extremely hard to generate cash and keep their heads above water before their owners can even think of selling them on.

Private equity firms are instead looking for more innovative ways to get cash back to LPs. PAG, one of Asia’s biggest private equity groups, is considering buying stakes in its own funds back from its investors, Bloomberg News reported last week. In April, Apollo Global Management talked to some investors about buying them out of an old fund so that they could invest in one of its new funds instead.

Fund managers are also increasingly looking at partial sales of companies to existing investors, or using so-called continuation funds where companies owned by a fund that the manager wants to close are sold into a new fund that can be backed by different LPs.

Private equity firms live to do deals, to keep raising fresh funds and turning companies over, but with sales grinding to a near halt the whole machine looks like it could be seized up for quite a while yet. That’s tough for the fund managers, their investors — and all those bankers that have come to rely so heavily on the industry for fees. - Bloomberg Opinion

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

With a new norm this decade ahead, Pictet flags private equity and fixed income as better bets

PE secondaries turn private equity into a more accessible investment

Get in-depth insights from our expert contributors, and dive into financial and economic trends