Yahoo Finance

Yahoo Finance Plover Bay Technologies Leads Three SEHK Stocks That Could Be Trading Below Their Estimated Value

Amid a backdrop of modest global equity gains and shifting market dynamics, the Hong Kong stock market presents unique opportunities as certain stocks appear to be trading below their intrinsic values. In this context, understanding the fundamental attributes that contribute to a stock being considered undervalued—such as strong financials relative to market price—is crucial for investors navigating these conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

Name | Current Price | Fair Value (Est) | Discount (Est) |

Best Pacific International Holdings (SEHK:2111) | HK$2.11 | HK$3.82 | 44.7% |

Kuaishou Technology (SEHK:1024) | HK$49.35 | HK$98.69 | 50% |

Gaush Meditech (SEHK:2407) | HK$13.80 | HK$26.13 | 47.2% |

China Cinda Asset Management (SEHK:1359) | HK$0.72 | HK$1.29 | 44.2% |

Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$10.26 | HK$19.07 | 46.2% |

Innovent Biologics (SEHK:1801) | HK$36.80 | HK$66.88 | 45% |

REPT BATTERO Energy (SEHK:666) | HK$14.16 | HK$27.24 | 48% |

Zhaojin Mining Industry (SEHK:1818) | HK$13.86 | HK$25.10 | 44.8% |

Vobile Group (SEHK:3738) | HK$1.17 | HK$2.11 | 44.6% |

CGN Mining (SEHK:1164) | HK$2.70 | HK$4.86 | 44.5% |

Here's a peek at a few of the choices from the screener

Plover Bay Technologies

Overview: Plover Bay Technologies Limited, an investment holding company, specializes in designing, developing, and marketing software-defined wide area network routers with a market capitalization of approximately HK$3.57 billion.

Operations: The company generates revenue through the sale of wired SD-WAN routers (HK$14.59 million), wireless SD-WAN routers (HK$49.39 million), and from software licenses along with warranty and support services (HK$30.28 million).

Estimated Discount To Fair Value: 43.4%

Plover Bay Technologies, trading at HK$3.24, is significantly undervalued with a fair value estimated at HK$5.72 based on discounted cash flows, reflecting a potential undervaluation of 43.4%. The company's earnings are expected to grow by 13.82% annually, outpacing the Hong Kong market's average of 11.6%. Despite an unstable dividend track record, recent share repurchase announcements could enhance shareholder value by potentially increasing net asset value and earnings per share.

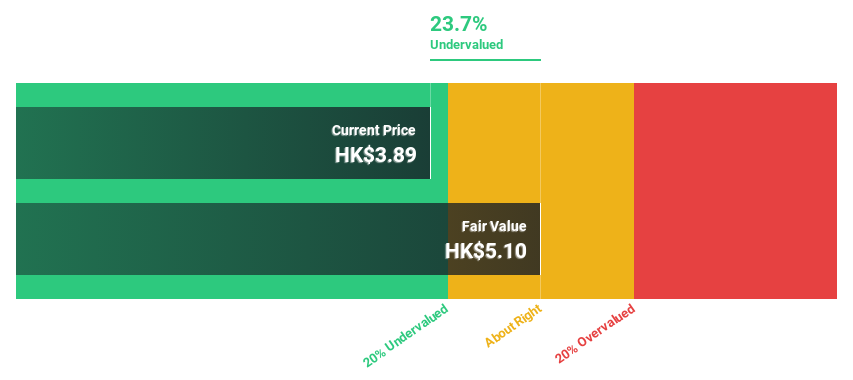

Global New Material International Holdings

Overview: Global New Material International Holdings Limited is an investment holding company that specializes in producing and selling pearlescent pigment, functional mica filler, and related products both domestically in the People’s Republic of China and internationally, with a market capitalization of approximately HK$4.82 billion.

Operations: The company generates revenue primarily through its operations in the People’s Republic of China and Korea, with segments reporting revenues of CN¥961.34 million and CN¥103.11 million respectively.

Estimated Discount To Fair Value: 23.7%

Global New Material International Holdings, priced at HK$3.89, is considered undervalued with an estimated fair value of HK$5.10. Despite a recent dip in net income and earnings per share for 2023, the company's revenue growth projections stand strong at 31.1% annually, significantly outpacing the Hong Kong market average. Furthermore, earnings are expected to surge by 41.85% per year, although it faces challenges like shareholder dilution and a decrease in profit margins from the previous year.

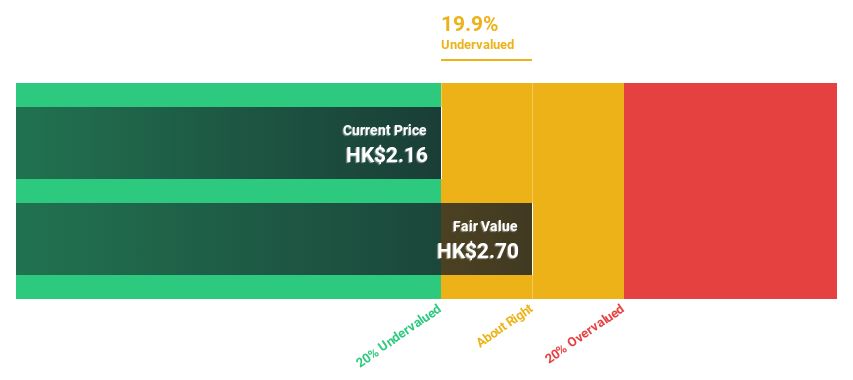

China East Education Holdings

Overview: China East Education Holdings Limited operates as an investment holding company that offers vocational training education services across the People's Republic of China, with a market capitalization of approximately HK$4.71 billion.

Operations: The company's revenue is primarily generated from its New East Culinary Education segment at CN¥1.87 billion, followed by Wontone Automotive Education and Xinhua Internet Technology Education with revenues of CN¥847.35 million and CN¥744.00 million respectively, along with contributions from Omick Education of Western Cuisine and Pastry at CN¥330.81 million, Cuisine Academy at CN¥49.30 million, and Wisezone Data Technology Education at CN¥37.88 million.

Estimated Discount To Fair Value: 19.9%

China East Education Holdings, valued at HK$2.16, is trading below its estimated fair value of HK$2.7, suggesting some undervaluation. The company's earnings are expected to grow by 20.84% annually, outperforming the Hong Kong market's average growth rate. However, its dividend sustainability is questionable as it is not well-covered by earnings or cash flows. Recent corporate actions include affirming dividends and adopting new articles of association to align with regulatory changes.

Make It Happen

Investigate our full lineup of 43 Undervalued SEHK Stocks Based On Cash Flows right here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:1523SEHK:6616 and

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com