Yahoo Finance

Yahoo Finance PhillipCapital drops Prime US REIT, Del Monte, HRnetGroup from 2Q2023 model portfolio

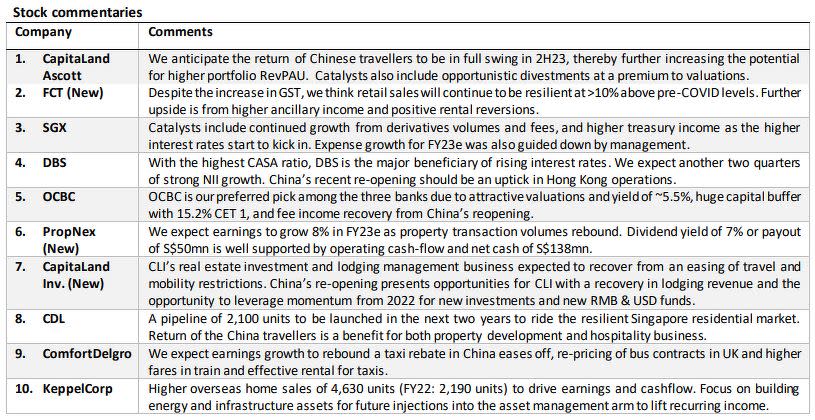

Replacing them in PhillipCapital's 2Q2023 model portfolio are Frasers Centrepoint Trust, PropNex and CapitaLand Investment.

After an encouraging 3.5% rise in January, the Singapore market returned all its gains to finish 1Q2023 relatively unchanged, as higher-than-expected inflation in the US plus jitters over banks pushed markets lower.

Singapore banks were sluggish, while the largest gainers were conglomerates from successful restructuring and better-than-expected results.

Property counters were surprisingly the weakest, says PhillipCapital head of research Paul Chew in an April 2 note, as higher interest and a large pipeline of new launches haunted investors.

After the US Fed’s March hike of 25 basis points (bps), Chew believes the rate hike cycle has paused. “We think the Fed is behind the curve. It is raising rates because economic weakness is not yet obvious.”

However, lead indicators point to an upcoming recession, says Chew, especially in manufacturing.

Conventionally, a catalyst to rally the market would be a Fed pause or interest rate cut. However, over the past three recessions, the Fed cut rates just three to six months before a recession. The market only bottoms one to 17 months after a rate cut, depending on the level of contraction in the economy.

In Singapore, the external environment is weakening fast, says Chew, as exports are in their fifth month of decline. The domestic economy will slow but we expect it to be resilient, supported by foreign domestic investment (FDI) flows, migration, tourism and fiscal spending.

‘Buy any equity that looks like a bond’

Chew’s recommended strategy is to be more patient than the Fed. “Disinflation is occurring although not immediately; global growth is tapering off. We overweight any equities that look like a bond. REITs are our tactical bet. We are not disillusioned that REITs face an uphill struggle in increasing their dividends due to higher interest rates. REITs do hedge rates for three years, but also akin to an interest rate headwind for three years.”

Looking at historical data, REITs have enjoyed more than a decade of ever declining refinancing costs on their interest-only loans, says Chew.

Chew still favours Singapore banks. “They pay attractive yields of almost 6% and enjoy huge capital buffers.”

Unlike Silicon Valley Bank (SVB) and Credit Suisse (CS), there is no accident waiting here, says Chew. "Firstly, Singapore banks only have 15% of their assets in investment securities, unlike the 57% for SVB. Local banks did not experience a doubling in deposits over the last two years, again unlike SVB. Secondly, Singapore banks enjoy a return on equity (ROE) of 12%."

PhillipCapital drops Prime US REIT, Del Monte, HRnetGroup

PhillipCapital’s Absolute 10 model portfolio was down 4.2% y-o-y in 1Q2023, which it blames on the “significant declines” of Prime US REIT and Del Monte.

PhillipCapital had added Prime US REIT to its model portfolio only in 1Q2023.

Expectations of higher interest rates and refinancing concerns in commercial real estate triggered concerns for Prime US REIT, says Chew. “We still believe valuations are attractive but worry about headline volatility. A consequence of the collapse of several banks will be a tightening of commercial real estate lending. Several commercial property funds have already defaulted due to high gearing and large exposure to gateway cities. A binary outcome is creeping up.”

Meanwhile, Del Monte results were a disappointment due to a sharp drop in margins, he adds. For 2Q2023, PhillipCapital is also removing HRnetGroup over near-term softness in the job market.

“Our model is designed around the assumption that global growth will slow down faster than expected and interest rates have peaked. REITs are the near-term beneficiaries. Another theme is the re-opening of China. Beneficiaries are tourism and consumer spending. Banks pay an attractive yield of close to 6% and with earnings growth supported by another year of margin expansion,” notes Chew.

PhillipCapital adds FCT, PropNex, CLI

Replacing Prime US REIT, Del Monte Pacific and HRnetGroup in 2Q2023 are Frasers Centrepoint Trust (FCT), owing to improvement in rental income following strong tenant sales; PropNex, which enjoys a 7% dividend yield with good earnings visibility; and CapitaLand Investment (CLI), which is “reactivated” with the reopening of China.

CLI has a unique real estate “cradle-to-grave-to-afterlife” model. CLI can develop a piece of real estate, fill the property with tenants, dispose of the development to its own private equity funds or REITs and still enjoy fees as manager of these funds.

The model was at a standstill when China was in lockdown and interest rates were rising, but these conditions have reversed, says Chew.

They join incumbent names CapitaLand Ascott Trust (CLAS), Singapore Exchange (SGX), DBS Group Holdings, Oversea-Chinese Banking Corporation (OCBC), City Developments (CDL) , ComfortDelGro and Keppel Corporation.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

'Buy' banks ahead of FY2022 results, OCBC profit to exceed estimates: PhillipCapital

PhillipCapital maintains 'buy' on LHN, reduces TP to 47 cents

Continue to 'buy' dual-listed Del Monte after record margins in 2QFY2023: PhillipCapital

Get in-depth insights from our expert contributors, and dive into financial and economic trends