Yahoo Finance

Yahoo Finance Paysign, Inc. (NASDAQ:PAYS) boasts of bullish insider sentiment with 39% ownership and they have been buying lately

Key Insights

Insiders appear to have a vested interest in Paysign's growth, as seen by their sizeable ownership

A total of 4 investors have a majority stake in the company with 50% ownership

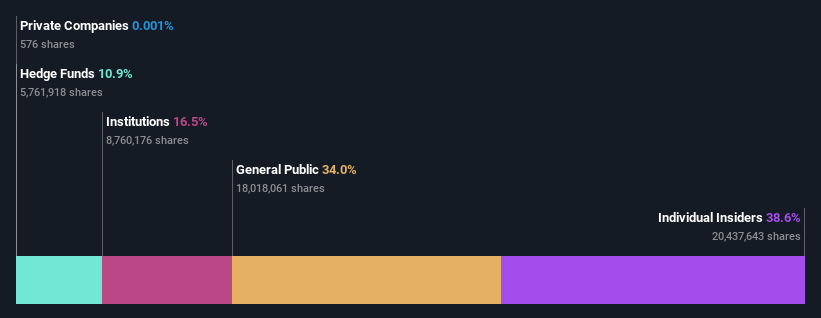

To get a sense of who is truly in control of Paysign, Inc. (NASDAQ:PAYS), it is important to understand the ownership structure of the business. And the group that holds the biggest piece of the pie are individual insiders with 39% ownership. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

It's interesting to note that insiders have been buying shares recently. This could be interpreted as insiders anticipating a rise in stock prices in the near future.

Let's take a closer look to see what the different types of shareholders can tell us about Paysign.

See our latest analysis for Paysign

What Does The Institutional Ownership Tell Us About Paysign?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

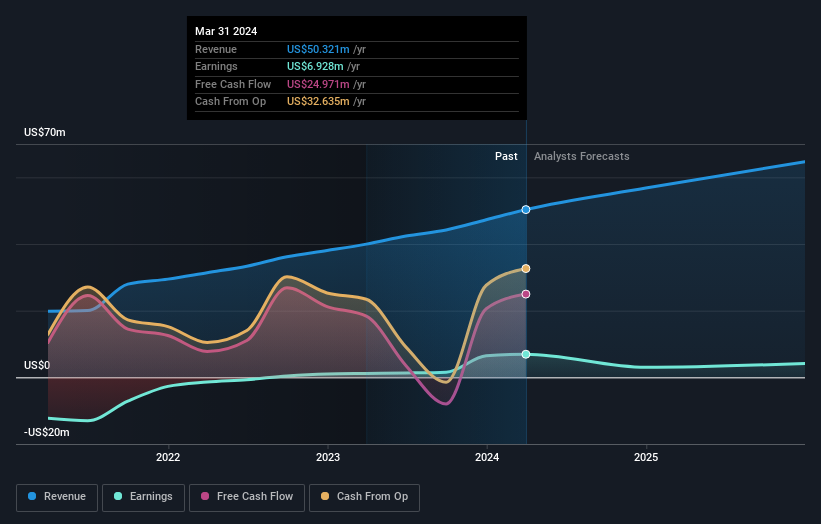

Paysign already has institutions on the share registry. Indeed, they own a respectable stake in the company. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Paysign's historic earnings and revenue below, but keep in mind there's always more to the story.

It would appear that 11% of Paysign shares are controlled by hedge funds. That's interesting, because hedge funds can be quite active and activist. Many look for medium term catalysts that will drive the share price higher. The company's CEO Mark Newcomer is the largest shareholder with 18% of shares outstanding. Daniel Spence is the second largest shareholder owning 17% of common stock, and Topline Capital Management, LLC holds about 11% of the company stock.

Our research also brought to light the fact that roughly 50% of the company is controlled by the top 4 shareholders suggesting that these owners wield significant influence on the business.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. There are plenty of analysts covering the stock, so it might be worth seeing what they are forecasting, too.

Insider Ownership Of Paysign

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

It seems insiders own a significant proportion of Paysign, Inc.. Insiders own US$88m worth of shares in the US$228m company. This may suggest that the founders still own a lot of shares. You can click here to see if they have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 34% stake in the company, and hence can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for Paysign you should know about.

Ultimately the future is most important. You can access this free report on analyst forecasts for the company.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com