Yahoo Finance

Yahoo Finance Palantir Technologies Is Navigating Growth and Valuation Challenges

Founded in 2003 by Peter Thiel, Nathan Gettings, Joe Lonsdale, Stephen Cohen and Alex Karp (who remains CEO), Palantir Technologies Inc. (NYSE:PLTR) is a data analytics and software development company based in Palo Alto, California.

The company develops software designed to serve as the backbone of a corporation's data infrastructure. This software ingests vast amounts of data and uses artificial intelligence models and proprietary algorithms to identify deficiencies, misallocated resources and inefficiencies.

Palantir went public in late 2020, experiencing a tumultuous ride with its stock surging over 300% at its peak from the initial public offering price, then plummeting to 37% below the IPO price before rebounding. Currently, the stock is still up over 100% from its initial debut.

Further, shares have climbed more than 40% year to date, significantly outperforming the S&P 500.

Figure 1: Palantir stock up over 45% year-to-date despite price decline following earnings release

For the first quarter of 2024, Palantir reported solid results, though growth fell short of elevated investor expectations. Despite a major beat-and-raise in its earnings release on May 6, the stock saw a 15% decline immediately following the announcement. Since then, the stock has largely regained its footing to previous levels.

While Palantir has been a favorite among AI enthusiasts, its valuation appears to be ahead of its projected growth rate. Although it is one of the few companies genuinely benefiting from the surge in AI interest, its current stock price reflects substantial hype around AI and the company itself.

From a long-term perspective, I remain bullish about Palantir's growth prospects. The company continues to deliver strong revenue growth and operating leverage, maintains a fortress-like balance sheet and has a management team dedicated to enhancing its offerings. However, my analysis suggests the current valuation is too generous. Therefore, I reiterate a hold rating at current price levels.

Current operations

Despite the negative market reaction following Palantir's earnings release, I believe that its financials are robust thanks to the strength of its Artificial Intelligence Platform bootcamp program. During the earnings call, management expressed confidence in Palantir's ability to capture additional market share for AI applications beyond generative AI, suggesting the platform's capabilities surpass those of its competitors. This optimism stems from Palantir's software, which not only addresses generative AI, but also extends to broader data analysis and business process enhancement. Palantir's AIP continues to be a driving force for the business, with the company having completed bootcamps with over 915 organizations.

Figure 2: 915-plus AI Bootcamps completed since inception

Source: Palantir Investor Relations

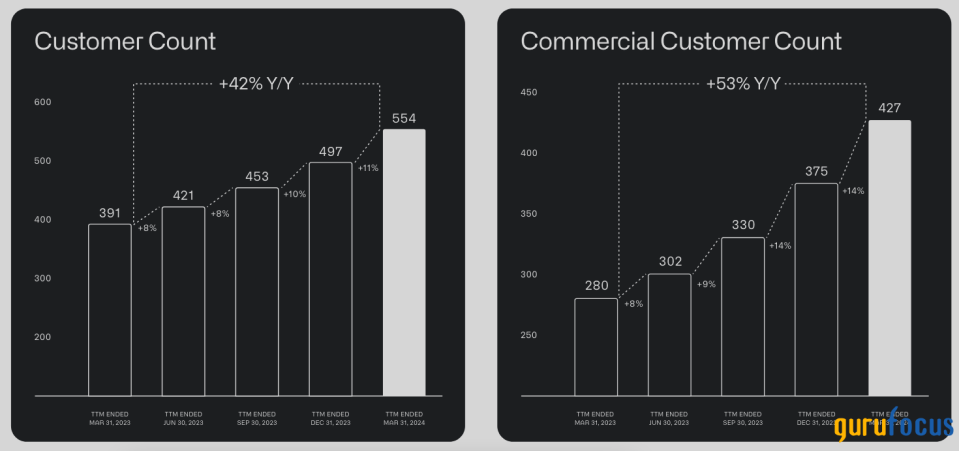

The demand for Palantir's services appears to be widespread, particularly in the U.S. commercial sector, which now includes customers from 56 of the 74 GICS industries. However, a critical issue for the company is its relatively small customer base. By focusing exclusively on commercial and governmental clients and excluding retail customers, its customer pool remains limited. As of the end of last year, the customer base was just 497 (554 as of first-quarter end 2024).

Figure 3: Growing customer base, though still limited

Source: Palantir Investor Relations

The company operates on a value model, deriving most of its revenue from a limited number of high-value contracts, such as the recent half-billion-dollar Army contract. This strategy contrasts with a volume-based approach and underscores the importance of landing substantial contracts to drive revenue growth.

Palantir also has a strong government business, which I consider a strategic advantage. Many of its legacy platforms sell to commercial customers, indicating the company's offerings are not solely reliant on AIP. However, the government segment has underperformed in recent quarters, a notable contrast to the success seen by competitors like C3.ai (NYSE:AI) in the same area. Despite this, I believe Palantir's government business will perform well over time, given its history and ability to provide comprehensive and secure solutions. While it has demonstrated strong performance and growth potential, particularly with its AIP, the company faces challenges related to its small customer base and recent underperformance in the government sector, balancing my positive outlook.

Financials

During the first quarter, Palantir demonstrated strong deal flow, closing 87 deals valued at $1 million or more, including 27 deals over $5 million and 15 deals over $10 million. This robust performance resulted in a 21% year-over-year growth rate on the top line, driving significant adjusted operating income margin expansion to 36%, up from 24% a year ago. Palantir's customer base is split between commercial and governmental clients, both showing strong year-over-year growth.

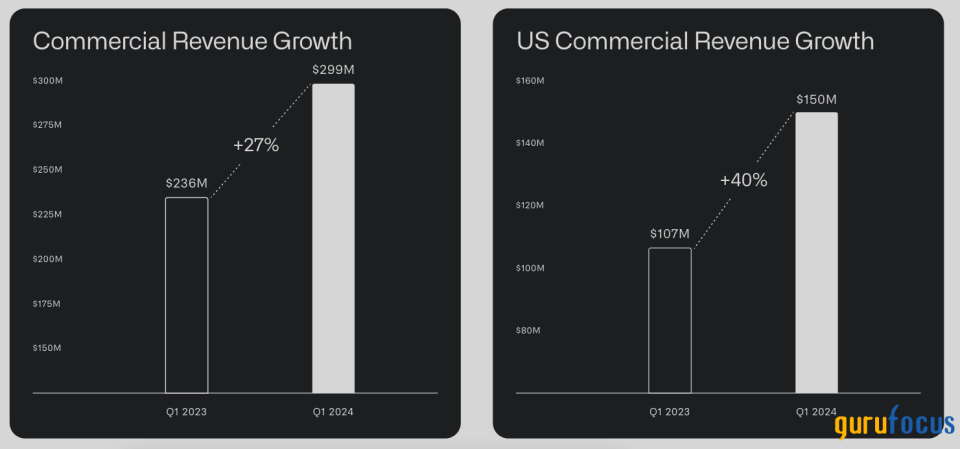

Figure 4: Strong first-quarter 2024 performance despite negative market sentiment

Source: Palantir Investor Relations

Commercial revenue grew by 27% year over year, with US commercial revenue increasing by 40%. While these figures are impressive, it is crucial to note that commercial revenue is recorded only after Palantir receives payment for invoices, which can take time due to the complexity of the software solutions. The key metric for evaluating AIP's scalability is whether the platform successfully closes contracts with new and existing customers, which it is.

Figure 5: First-quarter commercial revenue growth

Source: Palantir Investor Relations

Despite active sales growth in the first quarter, total operating costs rose by only 4.70%, allowing the company to achieve 18-fold growth in Ebit. The adjusted earnings per share expanded from 5 cents to 8 cents year over year, with actual revenue of $634 million beating expectations by 2.71%. The gross margin expanded from 79.50% to 81.70% and the operating margin improved from 0.80% to 12.80%. This strong operating leverage enabled Palantir to generate $83 million in free cash flow during the quarter.

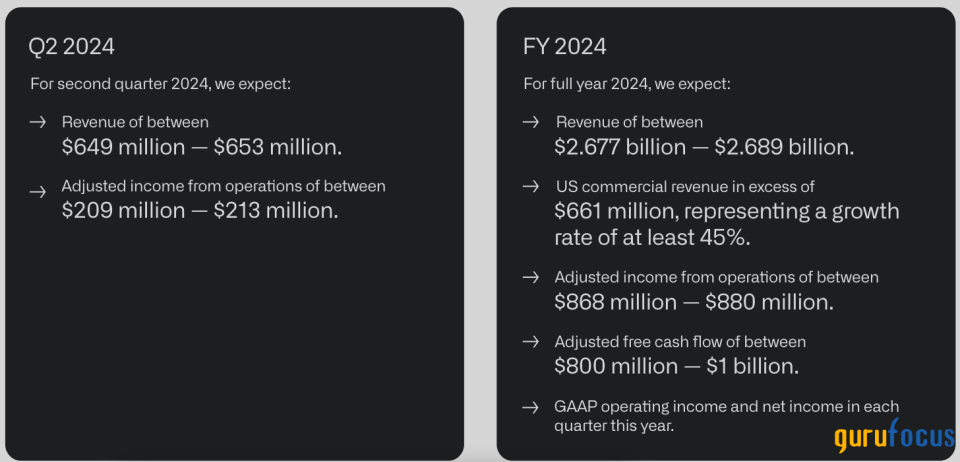

Palantir expects revenue of $649 million to $653 million in the second quarter, representing an approximate 22% year-over-year increase at the midpoint. I believe this guidance is conservative and anticipate growth exceeding 25%. Despite the projected top-line increase, adjusted earnings per share is expected to remain at 8 cents.

For the full year, the company forecasts revenue of $2.67 billion to $2.68 billion, up 21%, driven by U.S. commercial revenue growth of at least 45%. Revenue from strategic commercial contracts will continue to be a headwind in the coming quarters, causing Palantir's underlying growth to be understated. Management has increased its 2024 forecast across the operating statement and expects higher commercial engagement rates for the year. The company's ability to help enterprises save costs while optimizing operations suggests continued growth regardless of the macro environment. While AIP is a significant capital investment, it offers potential savings in operational expenses that justify its cost.

Figure 6: Palantir management forecasts

Source: Palantir Investor Relations

Palantir's profit margins continue to improve with scale, although operating leverage has started to moderate. Assuming the competitive landscape remains stable, I expect the company's operating profit margin to reach around 30% at maturity. However, there could be downward pressure in the near term as Palantir increases its investments in the U.S. to capitalize on both commercial and defense opportunities, leading to higher expenses in the latter half of the year. At the same time, its balance sheet is robust with $3.90 billion in cash and almost no debt. This financial flexibility is a fundamental strength, enabling the company to fuel organic growth, pursue acquisitions and invest in innovation.

Business outlook and valuation perspective

The crucial factor for my thesis is the growth of Palantir's AIP. Launched just nine months ago, the platform has already achieved over 100% growth in the U.S. commercial business for two consecutive quarters. In this context, I believe the reduced market guidance for 2024 is not a major concern. The behavior of Palantir's stock before and after the earnings release exemplifies short-term volatility and erratic market actions. The shares rallied more than 10% in the days immediately preceding the report.

In my opinion, this surge was based purely on speculation, as no new information was released during this period. The market seems to have overreacted to some of the data. However, after a thorough analysis of the financials, I believe Palantir is successfully scaling its AIP business in the U.S., which is crucial for gauging the scalability of its entire business model.

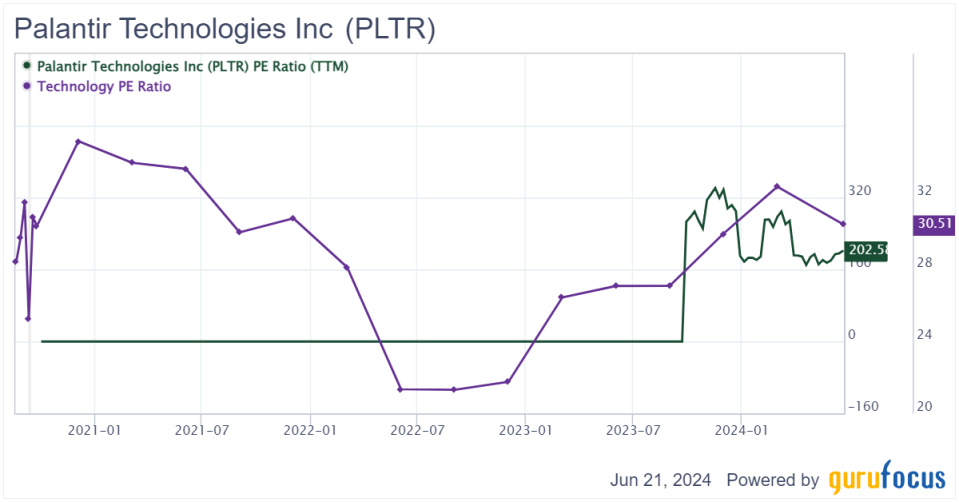

Palantir's negative earnings until 2023 put its current high valuation into perspective with a price-earnings ratio of 175.80 at the time of writing. Justifying this is challenging as it depends heavily on the company's future performance, which remains uncertain. However, if Palantir continues its trajectory of revenue and earnings growth, this ratio will likely decrease significantly by the end of this year.

Figure 7: Palantir's price-earnings multiple versus industry median

We have already seen progress as Palantir's earnings multiple previously exceeded 300. One major argument against the stockat least in the mid-term (the next five to 10 years) is the extremely high valuation multiples it is currently trading at. It is undisputed that such high valuation multiples are not sustainable. Considering the expected earnings per share for the next fiscal year, we arrive at a one-year forward price-earnings ratio of 70.90, which is still very high. If the stock drops below $15, it would enter what I consider value territory and I would reconsider my current hold rating.

Figure 8: Palantir's forward price-earnings multiples

Source: AlphaSpread

Final thoughts

To conclude, I maintain a hold rating for Palantir at its current share price. While expectations of lower interest rates should support valuations, mounting macroeconomic headwinds present an underappreciated risk. The company's growth is expected to accelerate in the coming quarters, but this may not be sufficient to drive the stock higher in the short term.

Palantir's first-quarter results have demonstrated that AIP is a scalable product. However, the market was anticipating an immediate and significant impact from its performance on the company's overall results, which has not yet materialized.

While I remain bullish on Palantir's long-term prospects, the stock is currently too expensive to be a prudent investment for risk-averse individuals or those focused on short-term gains. The company shows great potential with its innovative AI platform and strategic growth initiatives. However, given its high valuation multiples and the inherent volatility, it is not well-suited for all investors. For now, Palantir remains a hold as we await further validation of its growth trajectory and scalability in the broader market.

This article first appeared on GuruFocus.