Yahoo Finance

Yahoo Finance A mild retreat by risk-free rates won’t help equities to rally

With ADX at 13, the STI is likely to remain rangebound. Despite a minor top, 10Y US yields may resume their climb after a pause

Not much happened in terms of price movement for the Straits Times Index which rose around 13 points during the last week of September to end the month at 3,217, and up 21 points during the month.

For most of the month, though, the index moved within a range with resistance at 3,285 and support at 3,200. The 50-, 100- and 200-day moving averages are at 3,247, 3,226 and 3,252, with the STI moving within 30 points above and below these levels.

With the index rangebound, directional movement indicators continue to stay within neutral readings. ADX is at 13, a relatively low level confirming the lack of a definite trend. The DIs are more or less neutral with a mild negative bias.

In the first week of October, the STI may remain within much of its September trading range. While it is a bit early, there have been at least two notable October crashes, in 1929 and 1987. Generally October is a skittish month for the markets, although this time it could be different.

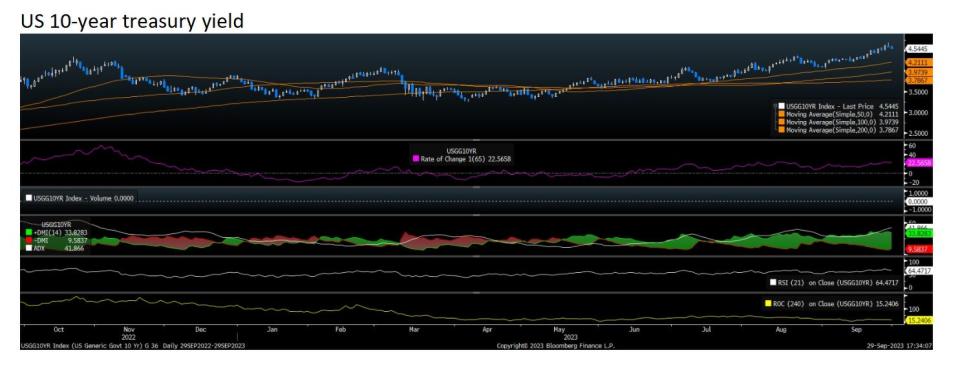

The main negativity surrounding the market - and not just the SGX - but other developed markets, is the upward trend of risk-free rates, led by 10-year (10Y) US treasury yields.

Although a small gravestone doji has appeared on the candlestick chart of the 10-year US treasury yield, it is likely to have a limited impact with a minor retreat. The 10Y yield rose to a high of 4.6% before easing to 4.54%. The 10Y yield needs to fall below 4.2% for weakness to materialise.

In the meantime, its uptrend appears relentless. Market watchers reckon that the 10Y yield could get as high as 5% before it does any meaningful retreat. Against this backdrop, equities may be unable to do much upward movement.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

The Fed has rained on the parade, but investing locally retains its positives

Straits Times Index moves above resistance as investor focus moves to FPL

Get in-depth insights from our expert contributors, and dive into financial and economic trends