Yahoo Finance

Yahoo Finance Meta Platforms Had a Banner Year in 2023

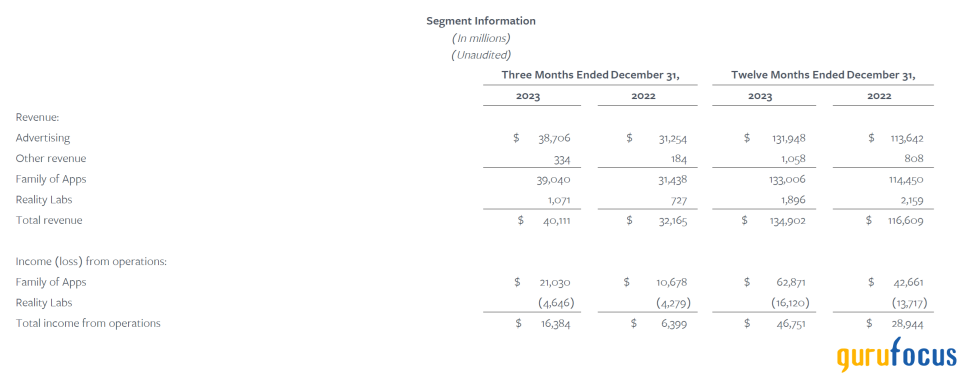

On Feb. 1, Meta Platforms Inc. (NASDAQ:META) reported financial results for the fourth quarter and full year ended Dec. 31, 2023. For the quarter, revenue increased 25% year over year, total costs and expenses decreased 8%, income from operations grew 156% and diluted earnings per share rose by a whopping 203%. The company announced its first-ever cash dividend and a $50 billion increase in the share repurchase authorization.

Meta founder and CEO Mark Zuckerberg was very happy with the results as he remarked, "We had a good quarter as our community and business continue to grow, we've made a lot of progress on our vision for advancing AI and the metaverse."

Obviously, investors agreed with Zuckerberg as Meta's shares soared 20% after the earnings report, adding more than $200 billion in market value in one day. The social media giant's earnings are very impressive compared to the other big tech companies.

Chinese advertisers powered Meta's growth

Meta's reports through two segments: Family of Apps (FoA) and Reality Labs (RL). The Family of Apps includes Facebook, Instagram, Messenger, WhatsApp and other services. Reality Labs includes augmented, mixed and virtual reality-related consumer hardware, software and content.

In terms of revenue contribution, the FoA segment accounted for more than 96% of Meta's revenue. Within the FoA segment, almost 100% of the revenue came from advertising revenue. Clearly, advertising is Meta's most important revenue source.

Meta Chief Financial Officer Susan Li explained the strong growth in advertising revenue for the quarter and year during the earnings call:

For full year 2023, the largest contributors to year-over-year ad revenue growth were the online commerce, CPG, entertainment and media and gaming verticals. The online commerce and gaming verticals benefited from strong demand by advertisers in China reaching people in other markets. In 2023, revenue from China-based advertisers represented 10% of our overall revenue and contributed 5 percentage points to total worldwide revenue growth.

Turning back to Q4 results. Q4 total Family of Apps revenue was $39 billion, up 24% year-over-year. Q4 Family of Apps ad revenue was $38.7 billion, up 24% or 21% on a constant currency basis. Within ad revenue, the online commerce vertical was the largest contributor to year-over-year growth, followed by CPG and gaming.

We can see that Chinese advertisers were the biggest drivers for Meta's revenue growth, which is consistent with the third quarter of 2023. During that quarter's earnings call, Li gave a more detailed answer regarding Chinese advertisers' growth:

To give you a little bit of color, in North America, we saw accelerate by 7 points due primarily to strong demand from China advertisers. Note that North America didn't experience the same currency tailwinds that drove acceleration in year-over-year growth for the other regions. In the EU or in our EU region, we saw that accelerate 21 points. There was a broad-based acceleration in the region, including demand from China advertisers and some benefit from currency tailwinds after facing currency headwinds in Q2. Brazil was a strong contributor to the region's acceleration due in part to increased advertisers' demand from China advertisers targeting users in Brazil.

By China adverisers, obviously Li meant Shein and Temu from PDD Holdings (PDD), especially Temu. According to a WSJ article published on Nov. 28, 2023:

Forty-six percent of Temu's digital ad spend so far this year went to Facebook, 22% went to Instagram, and 15% went to YouTube, according to market intelligence firm Sensor Tower. The wave of spending by China-owned retailers is affecting the overall online ad business. Temu and rival Shein are 'almost single-handedly having an impact on the cost of advertising, particularly in some paid channels in Google and Meta,' Etsy CEO Joshua Silverman said during an earnings call with analysts earlier this month. Susan Li, chief financial officer at Meta, has also credited unnamed Chinese retailers with helping to sustain the company's ad business in recent months.

CNBC also reported that:

JMP analysts estimated that Temu and Shein spent roughly $600 million and $200 million, respectively, on Facebook and Instagram ads in the third quarter. That would suggest they accounted for about 3% of Meta's total growth in the period, according to JMP. Research from data.AI prepared for CNBC shows that Temu notched 73.87 million downloads in 2023, up more than 500% from a year prior. Shein's downloads increased around 52% over that stretch to 36.93 million.

Temu's growth is truly extraodinary. The e-commerce site was launched in the U.S. in September of 2022. After the launch, it had to spend aggressively in order to attract customers and gain brand recognition. Fortunately for Meta, Facebook, Instagram, Messenger and WhatsApp are all important advertising channels that can give Temu the broadest reach, not only in the U.S., but across the globe.

Temu has spent a lot on Meta's social apps in 2023. The important question is whether its advertising spending is sustainable in 2024 and beyond. Even if Temu's advertising spending is sustainable, are Meta's social apps still the most effective and efficient channels for it? I will not assume that Temu will continue to contribute such growth for Meta in 2024 because its user growth has already slowed down in the U.S. and it is almost guaranteed that Meta's exposure to Temu and Shein will be a political target from both Democrats and Republicans. Therefore, I think conservative investors should assume Meta's revenue growth will slow down in 2024 due to slower advertising growth from Temu on Meta's apps.

Conclusion

Meta has benefited from both a Year of Efficiency as well as Chinese advertisers' increased growth in 2023. But in 2024, both tailwinds are likely to subside. At 31 times 2023 earnings and 23 times estimated 2024 earnings, Meta's stock is not very expensive, but not very cheap either. Investors should keep a close eye on Temu and Shein's advertising revenue growth in the next two to three years.

This article first appeared on GuruFocus.