Yahoo Finance

Yahoo Finance KRX Growth Leaders With High Insider Stakes July 2024

The South Korean market has shown robust performance, rising 1.3% over the last week and achieving a 5.8% increase over the past year, with earnings expected to grow by 30% annually. In this context, stocks with high insider ownership can be particularly compelling as they often indicate confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In South Korea

Name | Insider Ownership | Earnings Growth |

ALTEOGEN (KOSDAQ:A196170) | 26.6% | 73.1% |

Fine M-TecLTD (KOSDAQ:A441270) | 17.3% | 36.4% |

Global Tax Free (KOSDAQ:A204620) | 18.1% | 72.4% |

Park Systems (KOSDAQ:A140860) | 33.1% | 35.8% |

Seojin SystemLtd (KOSDAQ:A178320) | 26.2% | 48.1% |

UTI (KOSDAQ:A179900) | 34.1% | 122.7% |

Vuno (KOSDAQ:A338220) | 19.5% | 118.4% |

HANA Micron (KOSDAQ:A067310) | 20% | 96.3% |

INTEKPLUS (KOSDAQ:A064290) | 16.3% | 77.4% |

Techwing (KOSDAQ:A089030) | 18.7% | 118.2% |

Let's take a closer look at a couple of our picks from the screened companies.

UNISEM

Simply Wall St Growth Rating: ★★★★★☆

Overview: UNISEM Co., Ltd. is a company based in South Korea that specializes in manufacturing and selling semiconductor equipment and components both domestically and internationally, with a market capitalization of approximately ₩355.05 billion.

Operations: The firm operates primarily in the semiconductor equipment and components sector, generating revenue through sales in South Korea and various international markets.

Insider Ownership: 30.3%

UNISEM, a South Korean company, demonstrates robust growth prospects with its earnings forecast to rise by 42.8% annually, outpacing the local market's 29.6%. Revenue is also expected to grow significantly at 22.6% per year. Despite these strong growth indicators and trading at a substantial discount of 74.3% below its estimated fair value, the company faces challenges such as high share price volatility and low forecasted Return on Equity at 17.1%. Recent activities include a modest quarterly earnings report and an extended buyback plan, underscoring ongoing financial management efforts.

Take a closer look at UNISEM's potential here in our earnings growth report.

Our valuation report here indicates UNISEM may be undervalued.

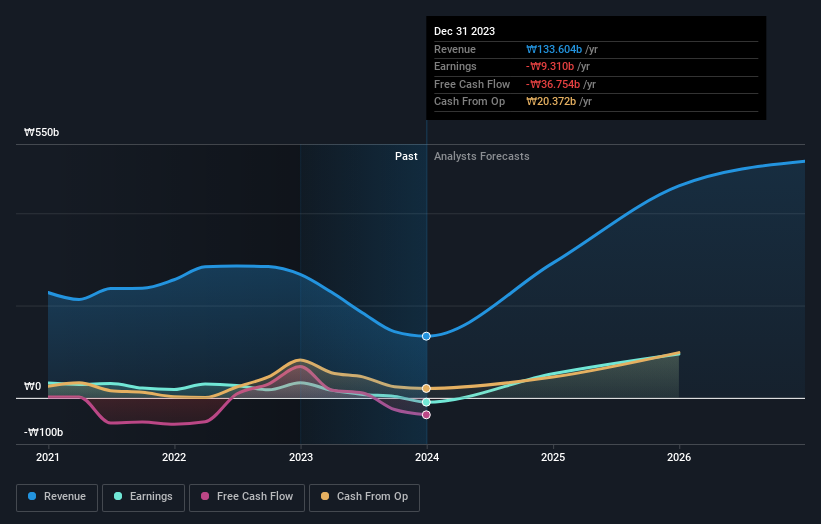

Techwing

Simply Wall St Growth Rating: ★★★★★★

Overview: Techwing, Inc. operates in the semiconductor industry, focusing on the development, manufacturing, sales, and servicing of inspection equipment both domestically in South Korea and internationally, with a market capitalization of approximately ₩2.17 trillion.

Operations: The company generates its revenue primarily from the development, manufacturing, sales, and servicing of semiconductor inspection equipment across domestic and international markets.

Insider Ownership: 18.7%

Techwing is poised for significant growth with expected revenue increases of 41.3% annually, surpassing South Korea's market average. Forecasted to turn profitable within three years, its projected Return on Equity is high at 33.1%. However, financial challenges persist as earnings barely cover interest payments, and the company's share price has been highly volatile recently. No insider trading activity was reported in the past three months, indicating stable but cautious ownership engagement.

Click here to discover the nuances of Techwing with our detailed analytical future growth report.

Upon reviewing our latest valuation report, Techwing's share price might be too optimistic.

Enchem

Simply Wall St Growth Rating: ★★★★★☆

Overview: Enchem Co., Ltd. is a South Korean company that specializes in manufacturing and selling electrolytes and additives for secondary batteries and electric double-layer capacitors (EDLC), with a market capitalization of approximately ₩4.94 billion.

Operations: The company generates its revenue primarily from the electronic components and parts segment, totaling approximately ₩357.37 million.

Insider Ownership: 19.8%

Enchem is set to experience robust growth, with revenue projected to increase by 56.5% annually, significantly outpacing the South Korean market average of 10.8%. The company is expected to become profitable within the next three years, with earnings growth forecasted at 144.8% per year. However, shareholders have faced dilution over the past year and the stock's price has shown high volatility recently. No insider trading activity has been reported in the last three months.

Navigate through the intricacies of Enchem with our comprehensive analyst estimates report here.

Our valuation report unveils the possibility Enchem's shares may be trading at a premium.

Key Takeaways

Click here to access our complete index of 87 Fast Growing KRX Companies With High Insider Ownership.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include KOSDAQ:A036200KOSDAQ:A089030 and KOSDAQ:A348370.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com