Yahoo Finance

Yahoo Finance Do Inchcape's (LON:INCH) Earnings Warrant Your Attention?

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Inchcape (LON:INCH). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Inchcape with the means to add long-term value to shareholders.

Check out our latest analysis for Inchcape

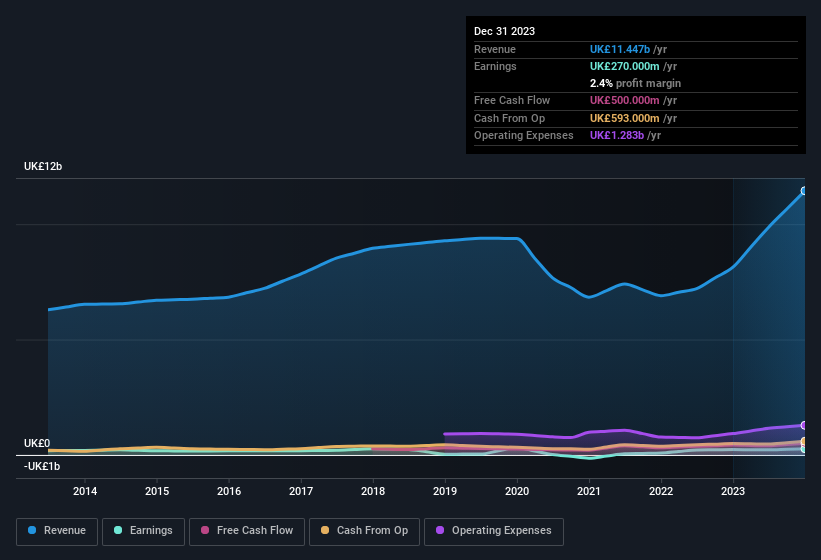

Inchcape's Improving Profits

In the last three years Inchcape's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. So it would be better to isolate the growth rate over the last year for our analysis. Over the last year, Inchcape increased its EPS from UK£0.61 to UK£0.66. That amounts to a small improvement of 7.2%.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. While we note Inchcape achieved similar EBIT margins to last year, revenue grew by a solid 41% to UK£11b. That's encouraging news for the company!

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Inchcape?

Are Inchcape Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Over the last 12 months Inchcape insiders spent UK£156k more buying shares than they received from selling them. Shareholders who may have questioned insiders selling will find some reassurance in this fact. We also note that it was the Independent Chairman of the Board, Jerry Buhlmann, who made the biggest single acquisition, paying UK£100k for shares at about UK£6.41 each.

Along with the insider buying, another encouraging sign for Inchcape is that insiders, as a group, have a considerable shareholding. With a whopping UK£63m worth of shares as a group, insiders have plenty riding on the company's success. This would indicate that the goals of shareholders and management are one and the same.

Should You Add Inchcape To Your Watchlist?

One important encouraging feature of Inchcape is that it is growing profits. In addition, insiders have been busy adding to their sizeable holdings in the company. That makes the company a prime candidate for your watchlist - and arguably a research priority. We don't want to rain on the parade too much, but we did also find 2 warning signs for Inchcape (1 is significant!) that you need to be mindful of.

Keen growth investors love to see insider activity. Thankfully, Inchcape isn't the only one. You can see a a curated list of British companies which have exhibited consistent growth accompanied by high insider ownership.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.