Yahoo Finance

Yahoo Finance IBM Is in the Midst of a Cloud Renaissance, Unlocking Secular Growth

International Business Machines Corp. (NYSE:IBM) is in the midst of a secular revolution. The company headquartered in Armonk, New York, which is commonly called IBM, had a change in its chief executive officer in the middle of the pandemic lockdowns in April 2020, and the change in leadership seems to have paid off.

The technology giant, known for its dividend yield rather than capital appreciation, delivered 15.5% in 2023, outperforming the Dow Jones Index by almost two percentage points. Add in its juicy 4.1% annualized dividend yield, which brings total gains in 2023 to 19.6%, and there are compelling reasons to invest in the company.

Through my research, I illustrate how business fundamentals, cash flows and margins have started to look much better.

The sleeping giant has woken up

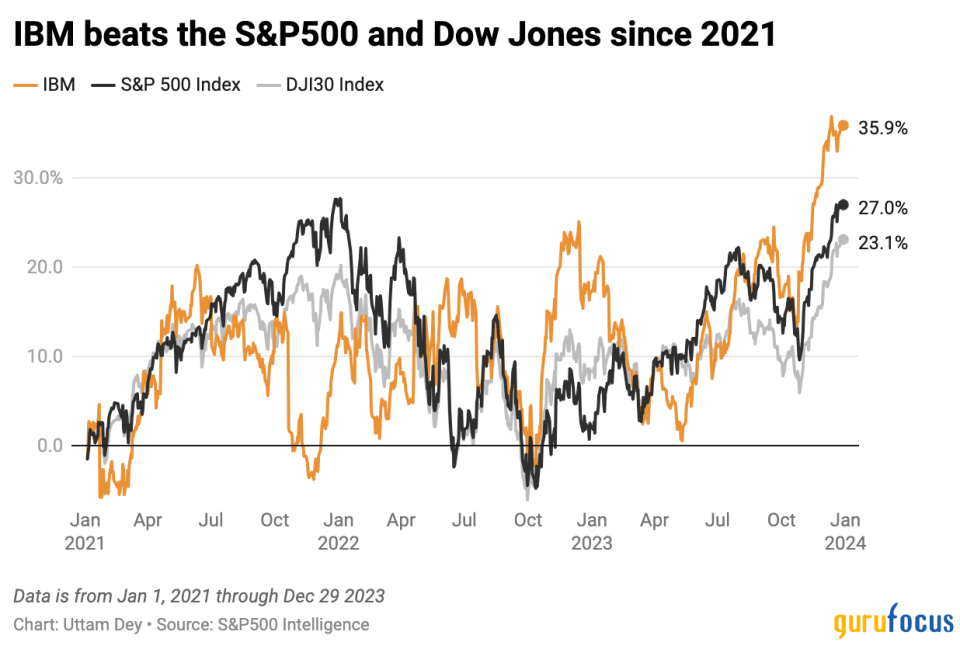

2023 was a year that most economists and market strategists got wrong. According to Bloomberg, while some economists baked in too much pessimism in the economy, market strategists issued calls for 2023 to be bleak. As the economic slowdown narratives faded with blowout U.S. gross domestic product estimates consistently surprising on the upside, according to Fortune, markets eventually became optimistic and the S&P 500 index notched a 24.7% gain in 2023. The Dow Jones Index underperformed at 13%, but IBM recorded almost 20% gains this year, taking into account its 15.5% stock performance and the 4.1% annualized yield.

While still impressive, many would view IBM as having underperformed the S&P 500 Index last year. However, when looking at larger historical performances and accounting for the severe volatility all investors were subject to in 2022, IBM has actually been outperforming the benchmark index. Its incredible performance is illustrated in the chart below.

This feat is something that would not have been deemed possible given how severely IBM underperformed between 2012 and 2020.

About IBM

While IBM is a popular pick among investors, especially value-focused investors hunting for yield, I will not go too deep into the history of the company. But I will point out that it had trouble retaining its client base, especially in the last decade, as it missed out on the cloud computing era of software development and distribution. With the rise of cloud computing, IBM severely lost market share to cloud hyperscalers such as Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT) and Alphabet's (NASDAQ:GOOG) Google.

Realizing it missed out on the opportunity, IBM acquired Red Hat, the maker of open-source cloud software products meant for enterprises to build software applications in the cloud, in 2019. This acquisition became pivotal to the technology giant fully pivoting into its cloud business. Later, IBM's new CEO, Arvind Krishna, offered a glimpse of his vision in an open letter in late 2021, where he outlined the key strategies for his vision to take IBM forward. At the center of his vision was to revamp IBM's entire product portfolio around the hybrid cloud and artificial intelligence.

Today, IBM calls itself a hybrid cloud company that helps enterprises build and scale AI, automation and hybrid-cloud-based solutions. As per its latest earnings report, the company makes most of its revenue from its Software and Consulting business verticals. While Software accounts for around 42% of sales, Consulting rakes in about 30% of the company's revenue. Since Software is the highest-margin business segment within IBM, I usually look for upward trends in this segment. Moreover, with Red Hat, Automation and AI part of the Hybrid Cloud subsegment, I want to see continued growth in the Software segment.

IBM's cloud transformation is moving faster than anticipated

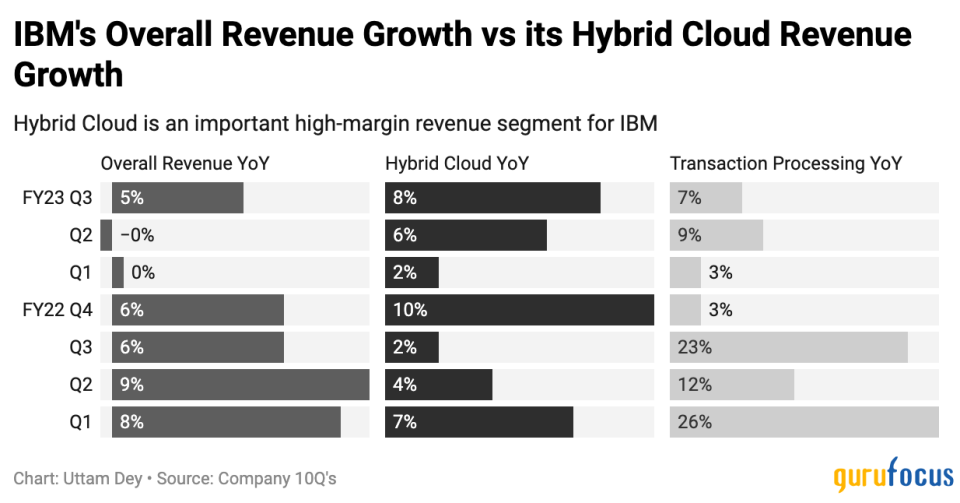

The most interesting part about IBM's reversal in business fortunes is that strength has started to return to its core Software segment. The Software segment is not only important to its overall growth narrative, but it also allows the company to leverage its position in the cloud computing space, which is still largely controlled by cloud hyperscalers. Within the Software segment, IBM's Hybrid Cloud business is critical. As can be seen in the chart below, this segment has started delivering consistent accretive growth to IBM's top and bottom lines.

In the third quarter of 2023, Red Hat and Automation led the year-over-year growth in Hybrid Cloud's 8% growth, with Red Hat up 9% and the Automation segment up 14%. For a company that was expected to grow in the low single digits for a good part of the last two decades, near double-digit growth is quite a welcome change. Typically, its software business is 80% subscription-based, while the remaining 20% is consumption-based. IBM's chief financial officer, James J. Kavanaugh, recently discussed the strength of its Subscriptions software business:

"If I extract out that 20% portfolio of consumption-based services and just look at the core subscription-based businesses of Red Hat, OpenShift and Ansible, we grew 19% overall. 110%-plus NRR on that renewal rate of that business. And within that 19%, OpenShift and Ansible were north of 40%. So, putting all that together, Software is at the high end of our segment model; we're only building in high single digits growth."

Finally, growth in the software segment is critical for IBM because this is a high-margin business, helping IBM book approximately 80% of revenue from this segment as gross profits. In a later section, I will unpack why this is important from a valuation standpoint.

Consulting business turns up its contributions

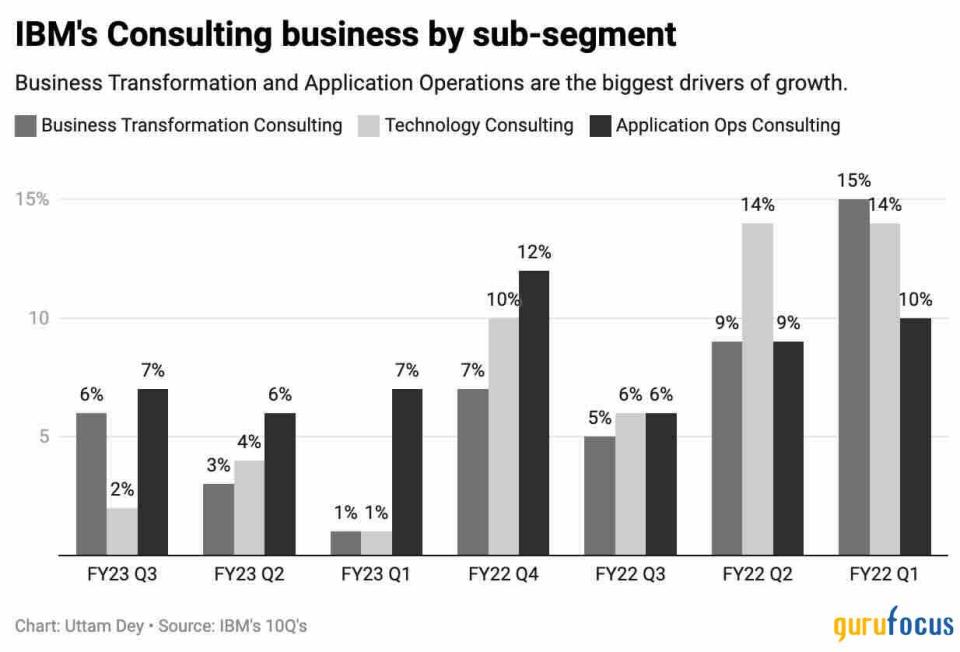

I previously mentioned IBM's Consulting business has started to scale its contributions to the top line in a very meaningful way. What is more interesting to me is that as I looked back over the past two years of available quarterly filings and compared IBM's Consulting business with its closest rival in the space, Accenture (NYSE:ACN), I noticed that IBM's Consulting business has been delivering steady and respectable contributions to its top line. Even better, the company appears to be gaining ground in market share versus Accenture, as can be seen in the chart below.

A peek under the hood reveals a clearer picture as to why IBM has been able to deliver such consistent gains even as enterprises around the world have been cutting their budgets for consulting projects. At the core of the Consulting business is the Application Operations and Management Consulting segment, which is directly tied to IBM's aspirations to scale capabilities for its clients in the hybrid cloud. As can be seen, Application Operations along with business transformation have formed the bedrock of IBM's consistency on a year-over-year basis in its consulting business.

On the third-quarter earnings call with analysts, the CFO alluded to the strength in IBM's Consulting Business by adding that most of the growth was because it opened IBM's technology to strategic partnerships, particularly with the cloud hyperscalers. I believe this may have been one of the key reasons why IBM continued to reap benefits from greater cloud ecosystem velocity due to the partnerships. The continued growth in IBM's Consulting business gives me further hope that IBM will be able to achieve its target of 6% to 8% growth this year.

Valuations point to upside

Per its most recent quarterly earnings, IBM's revenue was $14.8 billion, up 4.5% year over year. As I had talked about earlier in the post, the growth in earnings was driven by its Software segment and its Consulting business segment, which grew 7.8% and 5.6% year over year. While Software contributes 42% to IBM's top line, Consulting adds another 33%.

I mentioned earlier that the performance of IBM's Software business is crucial to the overall growth of the company; not just because it focuses on the hybrid cloud, but also because this is a high-margin business segment with 79.5% of its software business revenue being recognized as gross profit. Software's gross margins saw a nice bump up by 0.5% on a year-over-year basis. In addition, IBM's Consulting business saw a meaningful increase in its gross margins by 1.4% to 27.4%, thus lifting its overall gross margins by 1.7% to 54.4%. The incremental gains in gross margins also helped increase the non-GAAP operating margin by 1.7% to 15.6%.

In terms of free cash flow, its free cash grew by $1 billion to $5.1 billion, aided by strong growth in its operating cash flow, up $3 billion to $9.5 billion.

IBM projects its fiscal 2023 revenue will grow between 6% and 8%, while its non-GAAP earnings per sharewill decline by 5%. In fiscal 2024, consensus estimates project IBM to grow its revenue by 2.9%, with earnings per share rising by 4.4%. Assuming a 4.4% growth in earnings, this would mean IBM is trading at 17.8 times its forward earnings. Given the market estimates the S&P500 to trade at around 20 times its forward earnings, as per FactSet, this would give IBM at least 12% upside.

Risks to positive outlook

A major risk to IBM's positive outlook would be if enterprise spend were to suddenly fall, causing many enterprise clients to renegotiate their deals and push out their budget plans into subsequent periods. I use the word "suddenly because, so far,enterprise IT spend is expected to grow 8% into 2024, per Gartner. This is a strong projection, and these forecasts actually bode well for the revenue outlook of IBM into 2024. However, due to unforeseen circumstances, if there is a recession or even a soft landing, as Bank of America predicts, IBM's management may be forced to re-evaluate their forecasts lower for 2024.

A strong dollar could be another factor that could hurt the optimistic outlook for IBM. A majority of the company's consulting and software revenue comes from outside the U.S. If the dollar were to get stronger, it would dent the outlook for IBM to continue its growth into 2024. For example, one of the reasons that could push the dollar higher could be a reorientation by the Federal Reserve toward pushing interest rates higher.

Despite these risks, I still believe IBM would provide even greater opportunities to initiate or add to positions were we to see any downturn in the stock.

Takeaways

With the turnaround at IBM well underway, I believe this company has some great tailwinds that position the stock for upside. The accretive strength of its consulting and software businesses, with a renewed focus on hybrid cloud and AI technologies, has provided some opportunities for meaningful upside.

This article first appeared on GuruFocus.