Yahoo Finance

Yahoo Finance Hancock Whitney (HWC) Loan Balance Solid, Asset Quality Weak

Hancock Whitney Corp. HWC remains well-positioned for growth on the back of efforts to improve non-interest income, strong loan balance, higher rates and strategic expansion initiatives. However, weak mortgage income and deteriorating asset quality are challenges.

HWC remains focused on its revenue growth strategy. In 2019, the company acquired MidSouth Bancorp, which has been aiding its financials. Total revenues on a tax-equivalent (TE) basis experienced a compound annual growth rate (CAGR) of 4% over the last five years (2018-2023). Concurrently, total loans witnessed a 3.6% CAGR. Though the year-over-year trend reversed for total revenues in the first quarter of 2024, the uptrend for loans continued. High interest rates, decent loan demand and a strategic shift toward full relationship loans alongside investments in growth and new markets to boost fee income are likely to further aid top-line expansion. We project total revenues on a TE basis and total loans to witness a CAGR of 2.8% and 2.7%, respectively, by 2026.

Hancock Whitney’s net interest margin (NIM) witnessed a rise in 2023 to 3.34% from 3.26% in 2022 and 2.95% in 2021 on the back of high interest rates. The trend reversed in the first quarter of 2024 on a year-over-year basis amid high funding costs. With the Federal Reserve expected to keep the rates high in the near term, rising funding costs will continue to exert pressure on NIM.

Nevertheless, the company’s bond restructuring and balance sheet deleveraging initiatives are likely to offer support to NIM going forward. The company projects a modest NIM expansion this year on the assumption of three rate cuts, moderating deposit costs and a rise in loan yields. We project NIM to be 3.39%, 3.45% and 3.62% in 2024, 2025 and 2026, respectively.

As of Mar 31, 2024, HWC’s total debt was $904.1 million (most of which comprised short-term borrowings) and cash and due from banks was $414.3 million. The company enjoys investment-grade ratings of BBB/Baa3 and a stable outlook from Standard and Poor and Moody’s Investors Service, respectively. Thus, its decent earnings strength and liquidity position will enable the company to address its near-term debt obligations, even if the economic situation deteriorates.

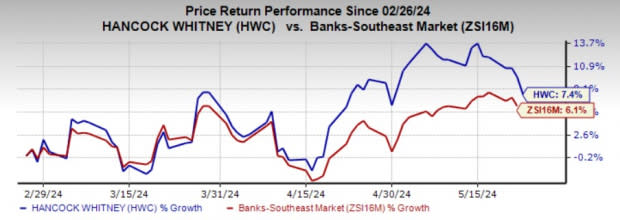

Hancock Whitney currently carries a Zacks Rank #3 (Hold). Over the past three months, shares of the company have rallied 7.4%, outperforming the industry’s growth of 6.1%.

Image Source: Zacks Investment Research

Yet, uncertainties regarding HWC’s mortgage banking business are a major concern. Secondary mortgage activity continues to be subdued due to higher mortgage rates, leading to lower mortgage income. The company’s secondary mortgage market income recorded a negative CAGR of 38.9% over the last three years (2020-2023). Though the trend reversed in the first quarter of 2024, Hancock Whitney is not likely to experience much improvement in secondary mortgage market income as mortgage rates are expected to remain high in the near term. Per our estimates, secondary mortgage market income is likely to witness a CAGR of just 12.2% by 2026.

Worsening asset quality is another headwind for Hancock Whitney. Though provision for credit losses and net charge-offs (NCOs) dipped in 2022, both witnessed an uptrend in 2023 on the anticipation of a deteriorating operating backdrop. The uptrend continued in the first quarter of 2024 for both metrics on a year-over-year basis. Even though the near-term recession risks have diminished, expectations of an economic slowdown are likely to keep the company’s asset quality under pressure. We project provision for credit losses to witness a CAGR of 12.1% by 2026.

Banking Stocks Worth Considering

Some better-ranked bank stocks worth a look are First BanCorp. FBP and First National Corporation FXNC, each sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks Rank #1 stocks here.

Estimates for FBP’s current-year earnings have been revised 6% upward in the past month. The company’s shares have rallied 18.8% over the past six months.

Estimates for FXNC’s current-year earnings have been revised 3.4% north in the past 30 days. The company’s shares have lost 15.1% over the past six months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

First BanCorp. (FBP) : Free Stock Analysis Report

First National Corp. (FXNC) : Free Stock Analysis Report

Hancock Whitney Corporation (HWC) : Free Stock Analysis Report