Yahoo Finance

Yahoo Finance Govt measures pull the brakes on accelerating HDB house prices as mortgage rates continue to rise

SINGAPORE (EDGEPROP) - In an attempt to cushion the effects of rising interest rates and tame house prices, which are at all-time highs, the Singapore government rolled out a new set of cooling measures at 11.40 pm on Sept 29, which came into effect at midnight.

Read also: Government releases yet another set of property cooling measures amid rising market interest rates

"The property market is now closer to an inflection point, amid slowing economic growth, rising living costs and interest rates, says Lam Chern Woon, head of research & consulting at Edmund Tie. “The final straw that breaks the housing camel’s back would be an outright recession impacting employment and income, or further cooling measures."

The latest measures include raising the medium-term stress test interest rate by 0.5 percentage points from 3.5% to 4% for residential property purchasers, based on the total debt servicing ratio (TDSR) of 55% for private housing loans. For non-residential property, the medium-term interest rate has been increased to 5% from 4.5% before.

For HDB loans, an interest rate floor of 3% will be applied for housing loan applications, based on the mortgage servicing ratio (MSR) of 30% for the purchase of executive condos (ECs) or HDB flats. However, the actual HDB rate of 2.6% shall remain unchanged. Both MSR and TDSR were introduced in the 2013 cooling measures.

“The calibration of the medium-term stress test interest rate is widely expected, as mortgage rates have already exceeded 3% in recent months and are likely to exceed the pre-measure stress test rate of 3.5% going into 2023, vanquishing any meaningful buffer to safeguard borrowers’ ability to service property loans in a rising rate environment,” says Edmund Tie's Lam.

“The 0.5 percentage point increase in the floor interest rate used to assess potential homebuyers’ repayment ability could weed out highly leveraged buyers if they are unable to re-juggle their loans to qualify,” says Tay Huey Ying, JLL head of research & consultancy. “We expect this to be a small number, and unlikely to have a major impact on overall sales volume, even after considering the potential slight crimping of HDB upgraders due to the latest round of cooling measures,” she adds.

Tay reckons the latest round of cooling measures could have been prompted by the 3.5% q-o-q jump in the URA all-private residential property price index in 2Q2022 and potentially strong price growth in 3Q2022 alongside the firmly recovering home buying activity in the first nine months of 2022, amid a rising interest rate environment and sharply slowing economic growth outlook.

The latest round of cooling measures could have been prompted by the 3.5% q-o-q jump in the URA all-private residential property price index in 2Q2022 and potentially strong price growth in 3Q2022 (Photo: Samuel Isaac Chua/EdgeProp Singapore)

EC buyers affected by stricter MSR limit

While unexpected, the new measures could lead to some short-term impact on private home sales in the coming months, notes Ismail Gafoor, CEO of PropNex. He sees the 0.5 percentage point increase in the medium-term interest rate potentially weighing heavier on the sale of new executive condominiums (EC) as EC buyers are subjected to the stricter MSR of 30% relative to the 55% TDSR for private home buyers.

As an example, a buyer with a monthly household income of $16,000 per month will now only be able to borrow about $1.667 million (assuming a loan tenure of 25 years, loan-to-value (LTV) of 75% and no debt obligations) and using a medium-term interest rate of 4%. Before Sept 30, the buyer would have been able to borrow up to $1.758 million or nearly $91,000 more in loan quantum (see Table 1).

Table 1: Impact of medium-term interest rate at 4% on maximum loan quantum*

*assuming 25-year loan, 75% LTV and no other debt obligations

Source: PropNex Research

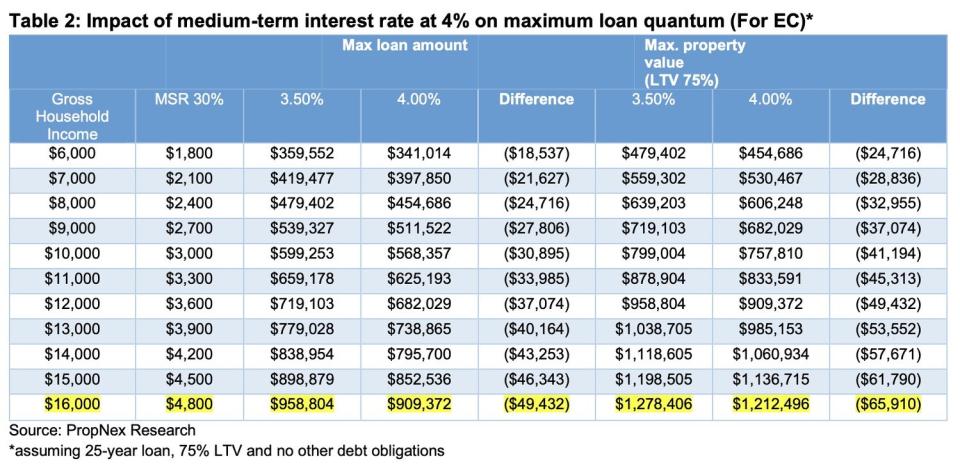

For EC buyers, where the monthly household income ceiling is $16,000, their loan quantum will differ as they are subjected to the 30% MSR. Under the revised medium-term interest rate of 4%, they will now be able to borrow about $909,300 assuming a household income of $16,000 a month. This is nearly $50,000 less than the $958,800 loan amount the EC buyer could have borrowed before. (see Table 2).

In terms of overall property price quantum, the EC buyer will only be able to buy an EC unit that is priced at $1.212 million, compared with $1.278 million under the previous 3.5% medium-term interest rate.

Lower LTV for HDB flat purchases

In addition to the 3% interest floor introduced in assessing home loan repayment ability, the loan-to-value (LTV) limit for HDB loans was also reduced to 80% from 85%. The LTV had already been reduced from 90% to 85% in December 2021.

“The new set of cooling measures have also been calibrated to tamp down demand for HDB resale flats and rein in the strong price growth in this segment,” notes PropNex’s Gafoor. “The reduction of the LTV limit for HDB loans will help narrow the discrepancy versus the 75% limit for loans from financial institutions.” (Find HDB flats for rent or sale with our Singapore HDB directory)

With the LTV lowered to 80%, even buyers of HDB flats taking a mortgage from HDB are likely to borrow a smaller loan quantum, says Nicholas Mak, ERA head of research & consultancy. The reduced purchasing power of some buyers could cause them to downsize, he adds. Mak expects four-room HDB flats to become even more popular, given that they are the smallest flats with three bedrooms.

Another measure requires private homeowners and ex-private homeowners to wait out 15 months after the disposal of their private properties before they are eligible to purchase a non-subsidised resale flat. (The 15-month wait-out period will not apply to seniors aged 55 and above (and their spouses) who are moving from their private property to a 4-room or smaller resale flat).

The wait-out period of 30 months continues to apply for purchases of new HDB flats or subsidised resale flats. “The authorities are clearly concerned about the ripple effects of ever-rising resale HDB prices on the private property market, plus the Built-to-Order [BTO] market where prices are offered at a discount to market,” says Edmund Tie’s Lam.

In the first nine months of the year until Sept 27, the number of HDB resale flats transacted for at least $1 million totalled about 270, already exceeding last year’s record of 259 units (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Slowdown in million-dollar HDB flat transactions expected

Strong demand for HDB resale flats spurred a 12.7% price growth in 2021 and a further rise of 5.3% in the first half of 2022, says Wong Siew Ying, head of research and content, PropNex Realty.

In the first nine months of the year until Sept 27, the number of HDB resale flats transacted for at least $1 million totalled about 270, already exceeding last year’s record of 259 units, PropNex’s Wong points out. Observations suggest that some of the million-dollar flat buyers have sold their private homes and downgraded to such flats, she says. “Flushed with cash from the sale of their private property, such buyers have the ability to pay higher prices for the resale flat as well as cash-over-valuation.”

To some extent, the latest measure will help to level the playing field for other buyers of HDB resale flats, as they may not have quite as big a war chest compared to the cash-rich downgraders who have sold their private homes, says PropNex’s Wong. “We expect the 15-month wait-out period to calm demand for HDB resale flats from private home downgraders,” she adds.

The number of transacted million-dollar flats is expected to slow down and may even decline for three to four months as many buyers wait and see before deciding on their home purchases, says ERA’s Mak. “After a few months, the potential buyers will return to the HDB resale market and the transaction volume of such flats will stabilize according to the market and economic conditions,” he adds.

The 15-month wait-out period may actually help support the rental market for both private and public housing markets (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Private resale and rental markets could benefit in the short-term

Some private residential property owners may be reluctant to sell their private properties to move into HDB flats, notes Mak. These private property owners include empty-nesters and couples who wish to downsize to a smaller property. “They could move to other private residential properties without waiting 15 months,” he says. Hence, this could increase the sales volume in the resale market.

While the wait-out period will have minimal impact on the residential en bloc sale market, the beneficiaries of en bloc sale projects who wish to buy HDB resale flats for their replacement home will now have to wait 15 months before doing so. “The profit from the en bloc sale is so attractive that they will be willing to rent a temporary home during the 15-month waiting period,” says Mak. (See potential condos with en bloc calculator)

The 15-month wait-out period may actually help support the rental market for both private and public housing markets, says Tricia Song, CBRE head of research for Southeast Asia. New private residential properties in the pipeline for completion in 2023 were projected at 17,394 units in 2Q2022, the highest number of completions in a single year since 2016, she notes.

“Residential rents are at a record high now and with this announcement, may continue to move up and remain elevated into 2023,” adds Song.

However, JLL’s Tay expects the upward pressure in the rental market to ease next year. “Those who still wish to dispose of their private homes, perhaps to ride the current robust home prices, could contribute to leasing demand – both in the private and HDB markets,” she says. Hence, she expects “a marginal upside” in the residential rental market.

One consolation is that borrowers who are refinancing their owner-occupied property will not be affected by the latest measures, according to ERA’s Mak.

The latest measures are also likely to impact HDB sellers who have sold their HDB flats at higher prices, and have decoupled for the purpose of using part of the proceeds to buy a private residential property as an investment (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Decoupling, HDB upgraders, property investors bear the brunt

This latest round of cooling measures has a more severe impact on the HDB resale market, in particular, the bigger five-room and executive HDB flats, says CBRE’s Song. This in turn could see lower demand for private home downgraders or en bloc sellers, and hence, a moderation in prices, she adds. “Lower HDB resale prices, in turn, could also moderate upgraders’ ability and thus demand into private homes.”

The shrinking pool of upgrader demand will indirectly cool the private residential market, especially the mass market or Outside Central Region (OCR), says Catherine He, Colliers director and head of research for Singapore. “This segment is mode dependent on upgraders,” says He. “Cash-rich buyers such as high-net-worth individuals will be less affected as they require less leverage.”

The latest measures are also likely to impact HDB sellers who have sold their HDB flats at higher prices, and have decoupled for the purpose of using part of the proceeds to buy a private residential property as an investment as well as a new home, says CBRE’s Song.

Recent new launch prices in Outside Central Region (OCR) exceed $2,000 psf, closing the price gap with the higher-end segments, notes Song. The latest launch was the 605-unit Lentor Modern on Sept 17. where 85% of the units have been sold at an average price of $2,106 psf, according to caveats lodged to date. It capped a year where new projects in the city fringe (Rest of Central Region) and suburbs (Outside Central Region), achieved sales rates from 75% to 98% on the first weekend of launch, with average prices above $2,100 psf.

The increase in medium-term interest rate stress test from 4.5% to 5% for non-residential property would most affect commercial property purchases by individuals for investment, says Colliers’ He. These include shophouses, strata office and retail units, as well as smaller industrial properties.

New home sales momentum and price growth are expected to slow in the next six to 12 months (Photo: Samuel Isaac Chua/EdgeProp Singapore)

Developers to go ahead with EC launches in 4Q2022

For existing launches in the market, most of them are at least 80% sold, and it will be business as usual, says Lee Sze Teck, senior director of research at Huttons Asia.

Two EC projects are scheduled for launch in 4Q2022: the 639-unit Copen Grand by City Developments and MCL Land, which will be the first EC project launched in Tengah Estate; and the 618-unit Tenet EC at Tampines North Street 62, a joint venture between Qingjian Realty and Santarli Construction. “They are likely to proceed as planned,” says PropNex’s Gafoor.

According to Mark Yip, CEO of Huttons Asia, buyers of ECs can opt for the deferred payment scheme. “This will allow them to ride out the current high interest rates,” he adds. “They can use the construction period to build up their savings to cover the lower loan limit.”

New home sales momentum and price growth are expected to slow in the next six to 12 months, cautions CBRE’s Song.

JLL’s Tay is expecting new home sales volume to end the year with 8,000 to 9,000 units, given that over 5,500 units have already been sold in the first eight months of the year. She expects the URA all-residential property price index to remain on track to end the year with an 8-9% increase, given the 4.2% price growth in 1H2022.

Likewise, Huttons’ Lee is also expecting a price increase of 8% by end of the year.

Marcus Chu, CEO of ERA Realty Network believes that the underlying demand for real estate is “still very robust, as the need to hedge against high inflation remains”. “This round of property curbs will encourage more financial prudence among buyers,” he says. “This would be positive for the property market in the medium to longer term as it would minimise financial risks from rising interest rates.”

Check out the latest listings near Lentor Modern, Copen Grand

See Also:

Singapore Property for Sale & Rent, Latest Property News, Advanced Analytics Tools

New Launch Condo & Landed Property in Singapore (COMPLETE list & updates)

Government releases yet another set of property cooling measures amid rising market interest rates

August BTO exercise sees strong demand for larger Ang Mo Kio and Tampines flats

En Bloc Calculator, Find Out If Your Condo Will Be The Next en-bloc