Yahoo Finance

Yahoo Finance The Future 50: Companies built for growth in uncertain times

Economic volatility and geopolitical uncertainty have roiled the markets all year. The causes are many, as new crises have continued to unfold: the war in Ukraine, with ensuing inflation and recession fears; the “tech crash” and the rising interest rates that fueled it; rising tensions between the U.S. and China; and the recent horrors in the Middle East.

Crises can be extraordinary opportunities for businesses to lay the foundations for robust growth. Gaining perspective on their impact, however, has become harder than ever. Will business leaders shift their focus from long-term growth toward short-term profitability? Will the tech sector continue to be a growth engine? Will China’s economy rebound? And how will all this interplay with longer-reaching issues like climate change?

To help investors cut through this kind of noise, Boston Consulting Group and Fortune teamed up in 2017 to create the Future 50. Our ranking assesses the long-term revenue growth prospects of more than 1,700 of the world’s largest public companies—judging them by a measure we call vitality. Our vitality index is based on two complementary pillars: a top-down, market-based assessment of a company’s growth potential, and a bottom-up analysis of its capacity to deliver, based on financial and nonfinancial metrics—including long-term strategic orientation, technology and investments, people, and structure. These factors are weighted based on their contribution to long-term growth using an AI model, and boiled down to a vitality score. (Read more on our methodology here.)

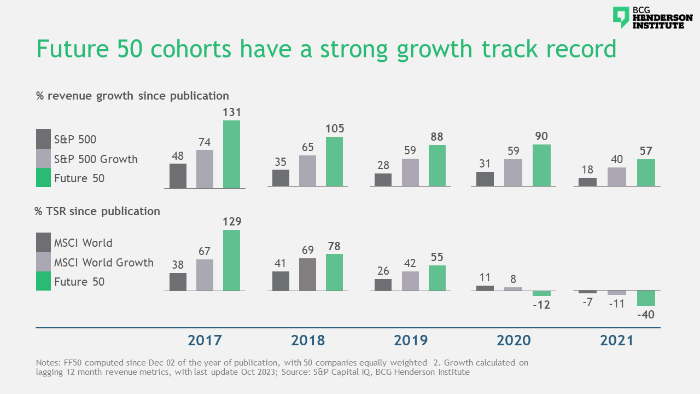

Over time, the Future 50 has delivered consistently on its revenue-growth potential, with all of our past cohorts beating the broader market on growth. Over the longer term, outperformance in growth translates into superior returns. However, this is not a linear process, since total shareholder returns display significant volatility over time. Accordingly, our 2017, 2018, and 2019 cohorts have outperformed the market in returns, while the 2020 and 2021 cohorts lag behind, at least for now.

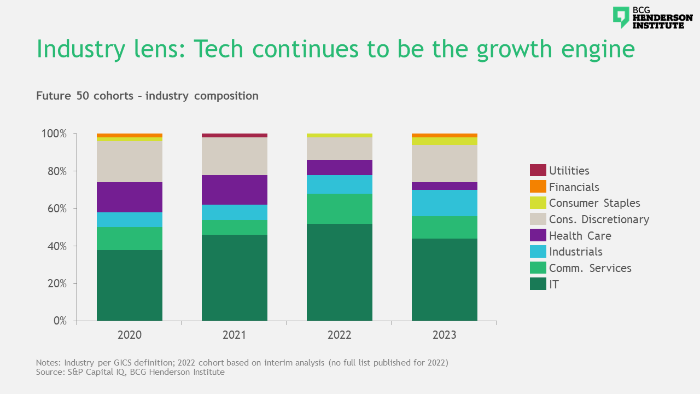

Why tech dominates

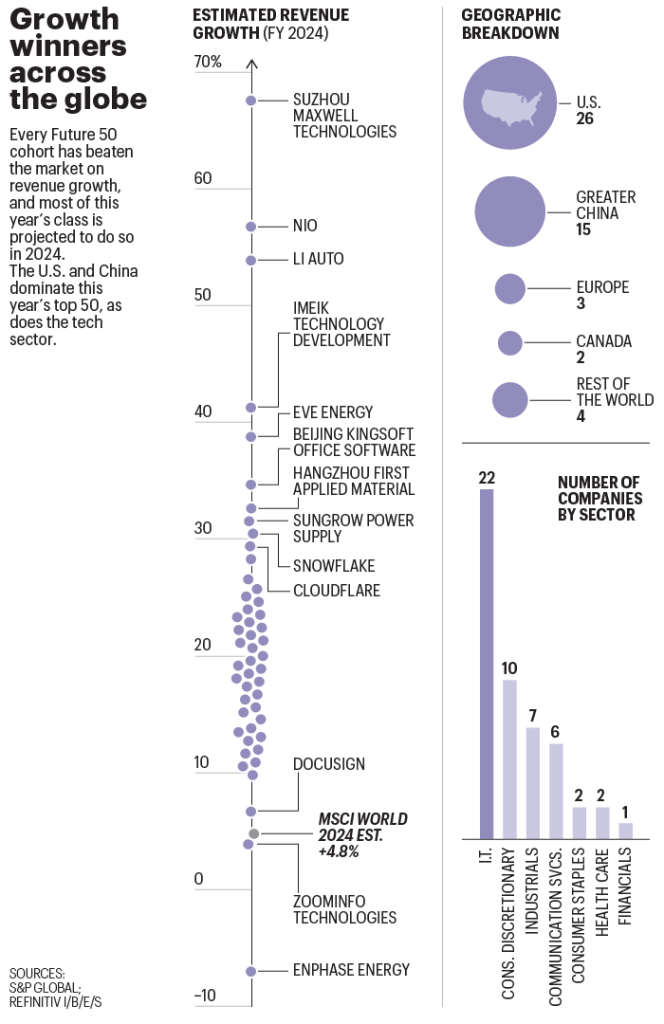

The tech sector faced significant headwinds in 2022 and 2023, as rising capital costs and increased investor scrutiny of profitability sent stocks plummeting and catalyzed a wave of layoffs. However, our analysis suggests that these are short-term corrections, and that the long-term growth potential of the sector is alive and well. The IT and communication services sectors continue to dominate this index, accounting for 28 of this year’s Future 50.

Various factors explain why tech has featured so prominently on our list. Tech companies’ market valuations often reflect investors’ high expectations of future growth—and our methodology gives substantial weight to the share of valuation attributable to those expectations. Other key characteristics that these companies share include significant R&D spending, high-quality patent portfolios, relatively youthful and stable leadership, and lean corporate structures.

This year’s cohort is in part driven by generative AI. For example, Shopify (No. 16) is developing a chatbot that simplifies sales operations for users, while ServiceNow (No. 19) is introducing large language models that generate case overviews and insights for customer service reps. Companies providing the tools behind AI solutions also score highly: As the saying goes, a gold rush is a great time to sell shovels. This group includes players in cloud computing, most notably No. 1 Snowflake, which is partnering with Nvidia to allow customers to develop AI models and applications on Snowflake’s platform; data warehousing (e.g., No. 42 Arista Networks); and big-data analytics (e.g., No. 18 Palantir).

The consumer discretionary and industrials sectors are also well-represented. This trend, too, is mostly driven by tech: Many Future 50 companies in these sectors are digital ecosystem players—for example, e-commerce giant No. 29 MercadoLibre, and platform providers like No. 9 DoorDash and No. 37 Trip.com Group. Most of the industrial companies, meanwhile, are active in the fast-growing “cleantech” industry, in solar power and battery tech (e.g., No. 12 Sungrow Power and No. 17 Suzhou Maxwell).

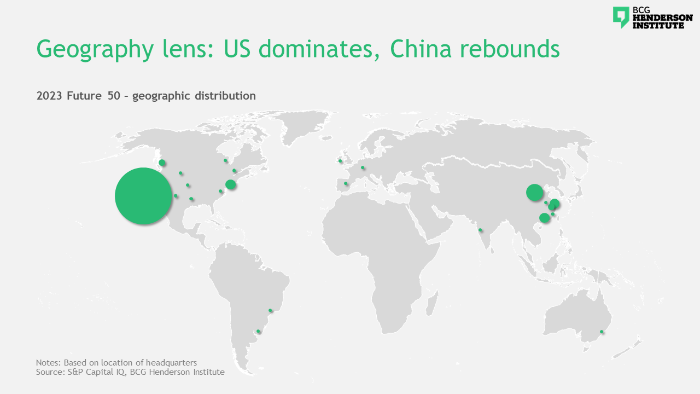

Rebound for China?

North America–based firms continue to account for the lion’s share (28 companies, or 56%) of the Future 50. Besides benefiting from systemic advantages such as strong education, trust in markets, and high availability of capital, they’ve been boosted by the robustness of the U.S. economy, which has weathered inflation and recession better than the rest of the world.

The Greater China region also attains strong representation (30%), concentrated within two sectors. First, there’s cleantech, represented by domestic EV makers (e.g., No. 5 Li Auto), and solar energy and battery tech companies (No. 10 EVE Energy and No. 49 CATL) that have been boosted by China’s ambitious renewable energy targets, as well as its dominant position in the mining and processing of many crucial raw materials. Second, e-commerce players make a strong showing, driven not only by sizable demand from a domestic consumer base, but by expansion into international markets.

This concentration reflects the shadows on other parts of China’s economy, from the still-raging property crisis, to tech and entertainment players being under threat as the government restricts internet usage for minors, to longer-term uncertainty driven by the decline and rapid aging of China’s population.

Europe continues to lag on vitality, with Spotify (No. 48) and Amadeus (No. 50) the only truly European firms on the list. (E-commerce player PDD is Dublin-registered but Shanghai-based.) Historically, this effect has been driven by a lack of venture capital funding; now war on the continent has exacerbated it.

Finally, Future 50 companies continue to have higher shares of female executives and board members (21%, on average) than other companies (19%) in our sample. Those numbers underscore the role diversity plays in driving innovation. However, that ratio, and the fact that only three of the 50 (6%) have female CEOs, also highlight that there is still far to go to achieve gender parity in leadership.

Overall, the 2023 Future 50 indicates that, despite near-term turbulence, the dominant patterns of long-term growth potential—including tech as a growth driver, and the U.S. and China as the dominant locations to nurture vital businesses—remain relatively stable. At a time of global instability, that makes our vitality ranking a critical tool for investors.

Martin Reeves is a senior partner at BCG and chairman of the BCG Henderson Institute. Adam Job is director of the Strategy Lab at the BCG Henderson Institute. Magdalena Krupa, Lina Cabarique, and Santiago Neira, data scientists at BCG X, also contributed to this work.

A version of this article appears in the December 2023/January 2024 issue of Fortune with the headline, "Companies that are built for growth, even in uncertain times."

This story was originally featured on Fortune.com