Yahoo Finance

Yahoo Finance Exploring Undervalued Small Caps With Insider Actions In June 2024

As global markets exhibit a mix of cautious optimism and selective growth, with the S&P 500 reaching new highs and modest gains across major indices, investors are keenly observing market dynamics. In this environment, undervalued small-cap stocks, particularly those with insider buying actions, could present intriguing opportunities for discerning investors looking to potentially capitalize on overlooked value in the current economic landscape.

Top 10 Undervalued Small Caps With Insider Buying

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Tokmanni Group Oyj | 16.6x | 0.5x | 39.37% | ★★★★★★ |

Cabka | NA | 0.5x | 22.13% | ★★★★★★ |

Columbus McKinnon | 21.4x | 1.0x | 42.13% | ★★★★★☆ |

PCB Bancorp | 8.6x | 2.3x | 46.54% | ★★★★★☆ |

THG | NA | 0.4x | 33.18% | ★★★★★☆ |

Norconsult | 28.3x | 1.0x | 41.59% | ★★★☆☆☆ |

Robert Walters | 20.6x | 0.3x | 35.50% | ★★★☆☆☆ |

Kambi Group | 17.9x | 1.5x | 23.86% | ★★★☆☆☆ |

Papa John's International | 20.7x | 0.7x | 31.02% | ★★★☆☆☆ |

Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

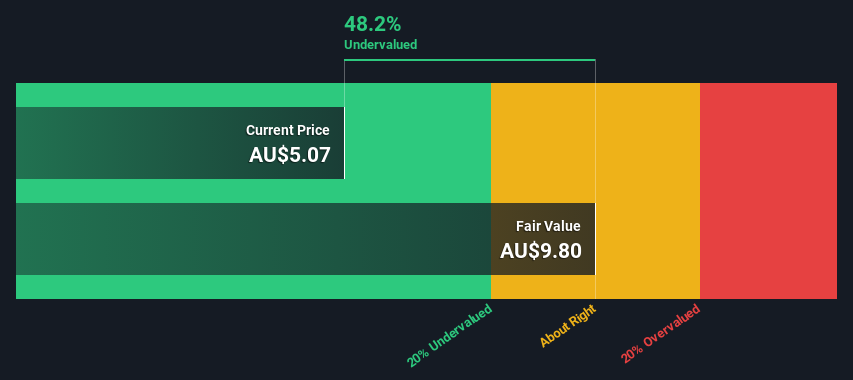

Clarity Pharmaceuticals

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Clarity Pharmaceuticals is a company focused on the development of radiopharmaceuticals, with a market capitalization of approximately A$9.49 million.

Operations: Radiopharmaceutical Development generates revenue of A$9.49 million, with a consistent gross profit margin of 100%. However, the company faces challenges as operating expenses have escalated to A$42.21 million, significantly impacting net income which stands at -A$30.56 million.

PE: -51.7x

Clarity Pharmaceuticals, engaged in critical industry conferences, recently showcased at events such as the ASCO Annual Meeting and SNMMI 2024, highlighting its active role in the medical community. Despite its current unprofitability with no short-term change expected, insider confidence is evident; they recently purchased shares, signaling belief in long-term prospects. This aligns with a recent follow-on equity offering raising A$20 million at a slight discount—further evidence of strategic capital management despite past shareholder dilution.

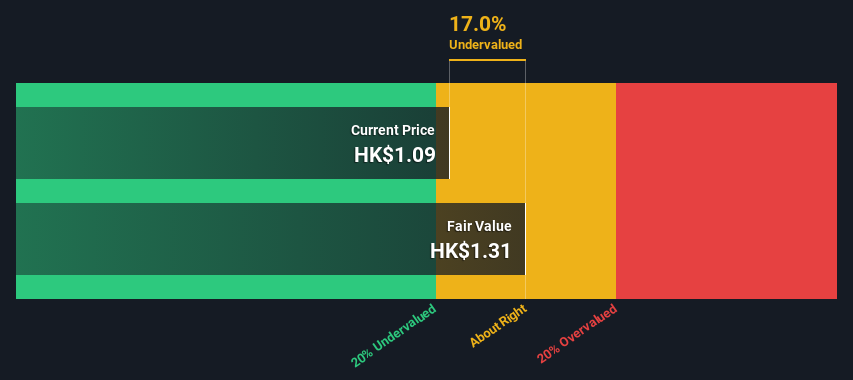

Kinetic Development Group

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Kinetic Development Group is a company primarily engaged in the property development sector with a market capitalization of approximately CN¥1.23 billion.

Operations: The company has demonstrated a notable trend in its gross profit margin, which has increased from 9.66% in June 2013 to 59.07% by June 2024, reflecting significant improvements in operational efficiency and cost management over the period. In terms of net income, it reversed from a loss of CN¥117.85 million in June 2013 to a profit of CN¥2.08 billion by June 2024, indicating robust growth and profitability enhancements.

PE: 4.3x

Kinetic Development Group, a lesser-known company with significant potential, recently showcased insider confidence through recent share purchases, signaling strong belief in its future prospects. Despite a reduction in its annual dividend to HKD 0.05 and the adoption of new company bylaws which could streamline operations, they continue to reward shareholders with a special dividend of HKD 0.03. With all liabilities backed by external borrowing, financial stability hinges on strategic management and market performance. The anticipation around their Q1 results due on May 31 reflects investor interest in their growth trajectory.

Dive into the specifics of Kinetic Development Group here with our thorough valuation report.

Understand Kinetic Development Group's track record by examining our Past report.

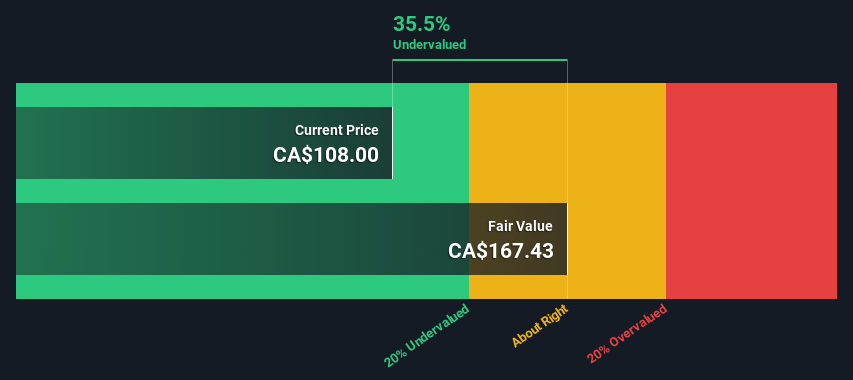

Hammond Power Solutions

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Hammond Power Solutions specializes in the manufacture and sale of transformers, with a market capitalization of approximately CA$729.61 million.

Operations: In the most recent fiscal quarter, the company recorded revenues of CA$729.61 million, with a net income of CA$55.63 million. The gross profit margin stood at 32.49%, reflecting the cost management in relation to revenue generated from transformer sales.

PE: 23.6x

Hammond Power Solutions, demonstrating a notable increase in sales from CAD 558.46 million to CAD 710.06 million year-over-year, recently showcased a robust financial trajectory despite a dip in net income for the first quarter of 2024. With earnings anticipated to climb by approximately 18.59% annually and reliance on external borrowing marking its funding strategy as higher risk, insider confidence shone through with recent share purchases, hinting at strong internal optimism about the company’s future prospects amidst its latest activities including a Shelf Registration filing for Class A Subordinate Voting Shares.

Make It Happen

Discover the full array of 233 Undervalued Small Caps With Insider Buying right here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:CU6 SEHK:1277 and TSX:HPS.A.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com