Yahoo Finance

Yahoo Finance What to Expect from Disney (DIS) Earnings

Disney DIS will highlight next week’s earnings reports with the company’s fiscal Q4 release on Tuesday, November 8. Trading 44% from its highs, investors are hoping Disney’s report can give DIS stock a much-needed boost.

Disney stock had historically been thought of as a mixture of value and growth that could play a stable role in many diversified portfolios. However, Disney’s valuation ballooned during the pandemic on the back of streaming exuberance at a time when its theme parks and movie box office segments were crushed by covid.

As Disney continues to work on a post-pandemic rebound, its diverse portfolio will be crucial. Along with amusement parks, Disney is a viable player in the digital streaming space through Disney Plus and has various other television, studio, and production networks including ESPN. Disney is still a premier film industry company and retail business through its consumer products and merchandise licensing.

Image Source: Zacks Investment Research

Despite the diversity among its businesses, DIS stock is down significantly more than the broader market over the last year. Wall Street will be monitoring the growth of three core areas: Disney Media & Entertainment Distribution (DMED), Parks-Experiences, and Consumer Products.

Overview

The majority of Disney’s revenue is derived from its DMED segment which includes Theatrical and Music distribution, domestic and international channels along with a 50% equity investment in A+E Television Networks, Disney+, Disney+ Hotstar, ESPN+, Hulu and Star+ DTC streaming services, Sales/Licensing of film and television content to third-party television and subscription video-on-demand services.

Disney’s DMED segment accounts for about 75% of total revenues. Last quarter, the DMED segment revenue climbed YoY 11% to $14 billion. This helped the company bring in $21.50 billion in total revenue which was up 26% from Q3 2021.

DIS blasted its fiscal Q3 earnings expectations by 16% at $1.09 per share, up an impressive 36% from $0.80 the prior year. DIS shares spiked 8% the following day but begin declining throughout the quarter as inflationary concerns took their toll on the stock.

Investors will be hoping another strong earnings beat in the company’s Fiscal Q4 release can help the stock get going again and produce another, more sustainable rally. Wall Street will also be looking intuitively to the company’s guidance and outlook as we move further from peak entertainment and travel seasons that boost the company’s Parks and Experiences revenue.

Fiscal Q4 Outlook

The Zacks Consensus for Disney’s Fiscal Q4 earnings is $0.57 per share, which would represent a 54% increase from Q4 2021. Sales are expected to be up 14% at $21.11 Billion. This appears to reflect that the company is adapting to the challenging operating environment.

However, earnings estimates for the period are largely down from $0.85 at the beginning of the quarter. Year over year, DIS earnings are expected to rise 66% and another 32% in FY23 at $5.03 per share. Top line growth is also expected, with sales projected to climb 24% this year and another 10% in FY23 to $92.67 billion. It is important to note that this year and FY23 revenue will surpass Disney’s pre-pandemic levels with 2019 sales at $75.12 billion.

Performance & Valuation

Year to date, DIS is down -36% to underperform the S&P 500’s -22% and roughly match the Media Conglomerates Market’s -33% with notable competitors Liberty Media FWONK and Paramount Global PARA.

Image Source: Zacks Investment Research

DIS is still up +111% over the last decade to crush its Zacks Subindustry’s +18%. Disney has clearly shown itself to be an industry leader for many years and investors are hoping this continued dominance can help the stock rebound. However, it is noteworthy that Disney Plus is facing increasing competition from Netflix NFLX.

After reaching 52-week highs of $179.25 last November, DIS currently trades just under $100 per share. At current levels, DIS has a P/E of 20.1X. This is below its peer group’s 30.1X. Even better, DIS trades at a significant discount to its decade-high of 134.4X and near the median of 19.5X.

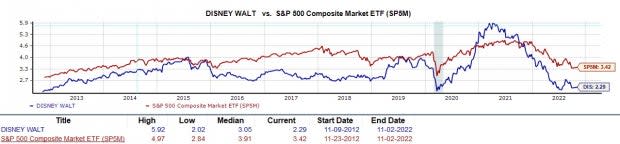

Image Source: Zacks Investment Research

Disney’s Price to Sales also looks attractive again. After spiking above the broader market’s P/S ratio during the pandemic we can see from the above chart that DIS’s P/S of 2.2X is back nicely below the benchmark’s 3.4X. Investors have historically paid a very reasonable price for every dollar of sales the company makes and this is important to see again.

Bottom Line

DIS currently lands a Zacks Rank #3 (Hold) and its Media Conglomerates Industry is in the top 26% of over 250 Zacks Industries. Despite the economic downturn, Disney’s revenue is set to surpass its pre-pandemic levels. Patient investors could be rewarded for holding DIS as it trades attractively relative to its past. Plus, the Average Zacks Price Target suggests 43% upside from current levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Walt Disney Company (DIS) : Free Stock Analysis Report

Netflix, Inc. (NFLX) : Free Stock Analysis Report

Liberty Media Corporation (FWONK) : Free Stock Analysis Report

Paramount Global (PARA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research