Yahoo Finance

Yahoo Finance Consumers Deplete an Average of 67% of All Available Savings Once Every Four Years

Nearly 8 Out of 10 Consumers Have Depleted Savings to Cover a Major Expenditure

Conversely, over One-Third of Consumers Earning More than $200,000 Annually Have Increased Their Savings Ability

SAN FRANCISCO, Oct. 30, 2023 /PRNewswire/ -- LendingClub Corporation (NYSE: LC), the parent company of LendingClub Bank, America's leading digital marketplace bank, today released key findings from the 27th edition of the Reality Check: Paycheck-To-Paycheck research series, conducted in partnership with PYMNTS Intelligence. The Savings Deep Dive Edition examines consumers' ability to preserve their savings in the current economic environment, especially when faced with major expenditures. This edition draws on insights from a survey of 3,648 U.S. consumers conducted from Sept. 5 to Sept. 20 and an analysis of other economic data.

The Paycheck-to-Paycheck Landscape

Living paycheck to paycheck remains the main financial lifestyle among U.S. consumers. As of September 2023, 62% of consumers lived paycheck to paycheck, unchanged from a year prior. Seventy-nine percent of consumers earning less than $50,000 yearly live paycheck to paycheck, as well as 68% and 44% of middle- and high-income consumers, respectively. Moreover, over one-fifth of U.S. consumers reported struggling to pay their bills — nearly 3 percentage points higher than this time last year. The share of consumers living paycheck to paycheck without issues paying monthly bills is 41%, down from 43% last year, while the share of those not living paycheck to paycheck has remained the same at 38%.

Consumer Savings Capacity

Aggregate consumer savings amounted to an average of $11,000 per consumer in September 2023, roughly unchanged from a year ago. Overall, 44% of consumers reported diminished savings capacity relative to a year ago, with 50% of those earning less than $50,000 yearly reporting such changes. Conversely, at 35%, consumers earning more than $200,000 annually are the most likely among income brackets to cite increased savings ability. Across groups, more than one-third of consumers are optimistic regarding increasing their savings capacity in the year to come — an indication that consumers expect to tighten their belts when they can.

"Inflation is taking its toll on Americans' ability to save, and while consumers remain optimistic, they are still reporting that their monthly expenses outpace their incomes," said Alia Dudum, LendingClub's Money Expert. "While unemployment and wage growth are low, consumers with middle- to high-incomes are getting squeezed the most as interest rates rise, and items that were once considered routine are now a luxury."

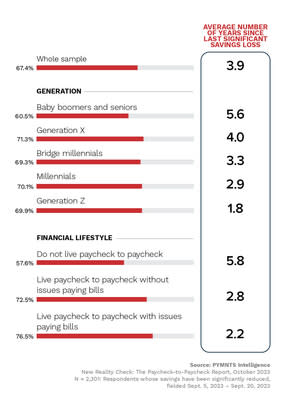

Average Savings Deplete Every Four Years

The research also indicates that nearly 8 out of 10 consumers (78%) recall having at least one expenditure which required them to withdraw a significant portion of their savings. While it is more prevalent with consumers who cite issues paying their bills (90%), a solid majority of consumers not living paycheck to paycheck (67%) have also done so. These depletions occur on average every four years and use 67% of the average consumer's available savings, with Gen Z emptying 70% of their savings as often as every two years. Among paycheck-to-paycheck consumers, these withdrawals occur every 2.2 years and require 76% of their savings balances, on average, for those struggling to pay bills; and they occur every 2.8 years and require 73% of savings, on average, for those living paycheck to paycheck without difficulty. Among consumers not living paycheck to paycheck, the share of savings required is 58% and is depleted every 5.8 years, on average.

Key Reasons for Savings Depletion

At 31%, emergency expenses, such as medical bills or unexpected repairs, are the top reason consumers deplete their savings, followed by job loss or income reductions, at 20%. This aligns with LendingClub's and PYMNTS Intelligence's research from June, which found average consumer emergency expenses rose 16% to $1,700 from the prior year, far above the Federal Reserve's $400 benchmark.

This latest research also indicates that Americans are dipping into their savings for discretionary spending, such as major life events (24%), travel (13%), and purchasing expensive items (12%). Consumers disclose that financial contingencies, such as debt accumulation (15%) and investment losses (15%), also cause them to deplete their savings. Moreover, younger consumers, at 51%, are more likely to tap into savings for major life events, such as marriage or buying a home, or splurge on expensive items or travel, making it more difficult to maintain higher savings levels.

Ease of Access to Funds and Fear of Risk Determine How Individuals Save

Despite ongoing inflationary pressures, there are no significant changes in the drivers of saving patterns when comparing 2023 to 2022. Even amid inflation worries, ease of access remains a top determinant in how consumers choose to save, with close to half of consumers citing speedy and convenient access to their funds as one of the drivers. Minimizing risk, at 19%, continues to outpace maximizing returns, at 14%, as consumers' top motivation when choosing how to save.

That said, consumers have benefited from better returns from the stock market this year, even as just one-tenth of savings are stored in these financial assets. Fifty percent of domestic stock investors reported increased values in their savings in the quarter prior to the survey — up from 31% when surveyed in 2022.

"When you take a deeper look at public savings data, increased saving rates are concentrated among those aged 55 and older," continued Dudum. "For those aged 34–44, their saving rates are compressed. As Americans spend upwards of $700 more per month on everyday goods and services than they did two years ago, we will likely see increased pressure on the overall household balance sheet and continued reliance on credit."

To view the full report, visit: https://www.pymnts.com/study/reality-check-paycheck-to-paycheck-consumer-savings-debt-investment

Methodology

New Reality Check: The Paycheck-to-Paycheck Report, a PYMNTS Intelligence and LendingClub collaboration is based on a census-balanced survey of 3,648 U.S. consumers conducted from Sept. 5 to Sept. 20 as well as an analysis of other economic data. The data in this report is not intended to be a representation of LendingClub's core member base. The Paycheck-to-Paycheck series expands on existing data published by government agencies, such as the Federal Reserve and the Bureau of Labor Statistics, to provide a deep look into the core elements of American consumers' financial wellness: income, savings, debt and spending choices. Our sample was balanced to match the U.S. adult population in a set of key demographic variables: 51% of respondents identified as female, 33% were college-educated and 39% declared incomes of more than $100,000 per year.

About LendingClub

LendingClub Corporation (NYSE: LC) is the parent company of LendingClub Bank, National Association, Member FDIC. LendingClub Bank is the leading digital marketplace bank in the U.S., where members can access a broad range of financial products and services designed to help them pay less when borrowing and earn more when saving. Based on more than 150 billion cells of data and over $90 billion in loans, our advanced credit decisioning and machine-learning models are used across the customer lifecycle to expand seamless access to credit for our members, while generating compelling risk-adjusted returns for our loan investors. Since 2007, more than 4.7 million members have joined the Club to help reach their financial goals. For more information about LendingClub, visit https://www.lendingclub.com.

CONTACT:

For Investors: IR@lendingclub.com

Media Contact: Press@lendingclub.com

PYMNTS Contact: information@PYMNTS.com

View original content to download multimedia:https://www.prnewswire.com/news-releases/consumers-deplete-an-average-of-67-of-all-available-savings-once-every-four-years-301971018.html

SOURCE LendingClub Corporation