Yahoo Finance

Yahoo Finance Citigroup (C) Rides on Restructuring Efforts, Fee Income Ails

Citigroup Inc.’s C efforts to streamline its core business internationally and the recent organizational restructuring are likely to support its financials. Also, a solid liquidity position will support capital distribution activities. However, escalating costs and challenges in growing fee income are concerns.

C’s new organizational structure replaced the existing reportable segment with five new reportable operating segments. The restructuring resulted in streamlining and straight forwarding management structure that is aligned with the bank's strategy. With fewer layers, increased spans of control and significantly reduced bureaucracy, the company will now be able to operate more efficiently. Through these efforts, C aims to drive $2-$2.5 billion of annualized run rate savings by 2026.

Citigroup has been streamlining operations internationally to focus on its core businesses. The bank seeks to pursue investments in wealth management operations in Singapore, Hong Kong, the UAE and London to stoke fee income growth. In October 2023, C agreed to sell its China’s wealth portfolio to HSBC Holdings (HSBC). Also, the bank will wind down its U.K. retail banking business, while expanding personal banking and wealth management businesses in the region.

The bank also plans to exit consumer and middle-market banking in Mexico by the second half of 2024. The company seeks to exit from 13 markets across Asia and the EMEA, having already completed divestitures in nine, since the announcement of this strategic action in April 2021. The bank anticipates the release of roughly $12 billion (in aggregate) of allocated tangible common equity over time from such exits.

Citigroup has an impressive capital distribution program. In July 2023, the company hiked its quarterly dividend by 3.9% to 53 cents per share. In the first quarter of 2024, the company distributed approximately $1.5 billion to shareholders through dividends and share repurchases. Driven by a strong capital and liquidity position, capital distribution activities seem sustainable.

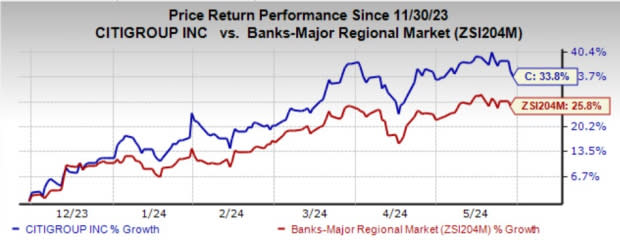

Shares of this Zacks Rank #3 (Hold) company have gained 33.8% compared with the industry’s growth of 25.8% over the past six months.

Image Source: Zacks Investment Research

However, Citigroup’s transformation expenses and business-led investments have kept the operating expenses flared up in 2023, witnessing a three-year (ended 2023) compound annual growth rate (CAGR) of 8.3%. Although increased spending, specifically on severance costs related to its organizational overhaul and divestiture expenses, inflates the company’s near-term expense base. These efforts will lead to cost savings in the longer term. Though we expect expenses to decline 3% and nearly 1% in 2024 and 2025, respectively, it will rebound and rise 2% in 2026.

Further, Citigroup’s non-interest income witnessed a three-year negative CAGR of 8.5% (ended 2023). Any decline in global investment banking activity, along with lower market valuations on assets under custody and administration, is likely to negatively impact fee income in the near term.

Stocks to Consider

Some better-ranked bank stocks worth mentioning are Northern Trust Corporation NTRS and BankUnited, Inc. BKU.

Northern Trust’s earnings estimates for 2024 have remained unchanged in the past seven days. The company’s shares have gained 3.6% over the past six months. At present, NTRS sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

BankUnited’s 2024 earnings estimates have revised upward marginally in the past 30 days. The stock has gained 8.2% over the past three months. Currently, BKU carries a Zacks Rank #2 (Buy).

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Citigroup Inc. (C) : Free Stock Analysis Report

Northern Trust Corporation (NTRS) : Free Stock Analysis Report

BankUnited, Inc. (BKU) : Free Stock Analysis Report