Yahoo Finance

Yahoo Finance Citi maintains ‘buy’ rating for CapitaLand Ascendas REIT with lower TP of $3.00

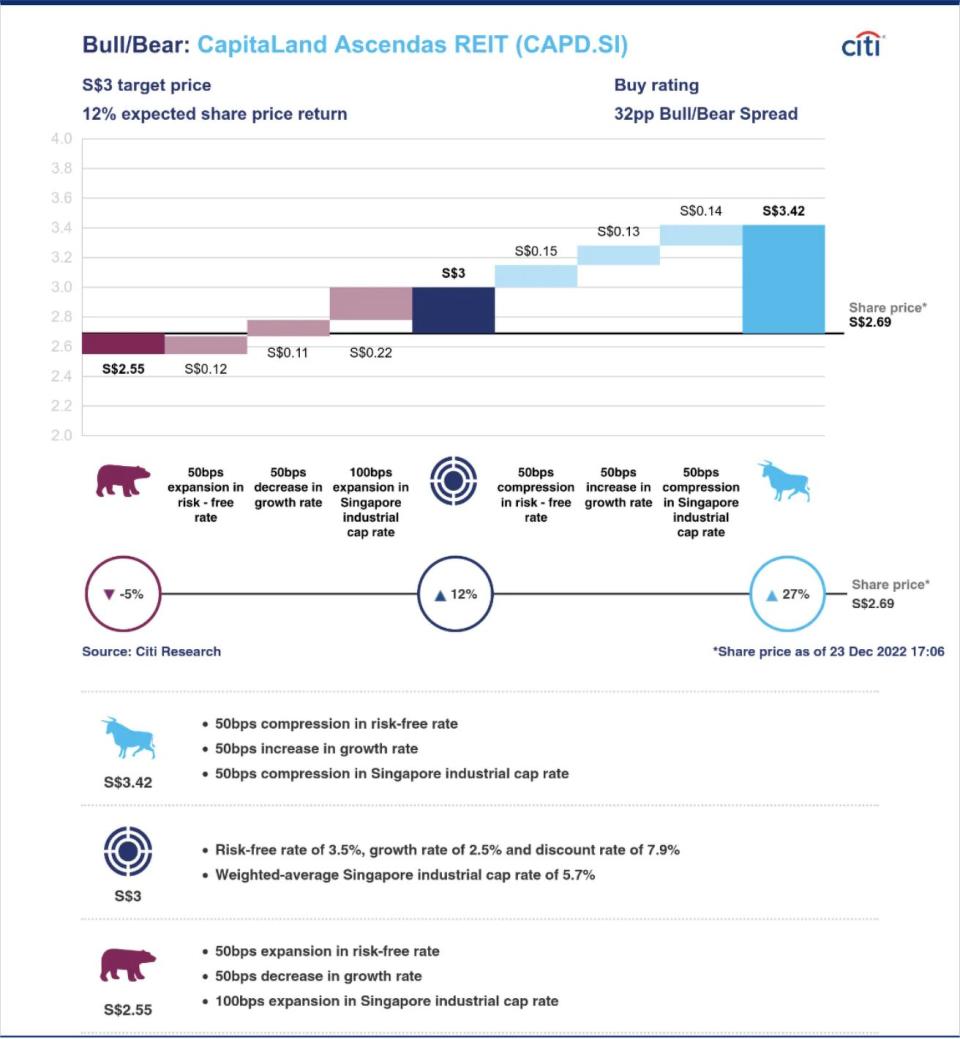

Citi Research analyst Brandon Lee has reduced his TP for CapitaLand Ascendas REIT to $3.00 from $3.15 previously.

Citi Research analyst Brandon Lee has maintained his “buy” rating for CapitaLand Ascendas REIT (CLAR) with a slightly lower target price (TP) of $3.00 from $3.15 previously following a model update.

The new target price is derived from an average of dividend discount model (DDM) and revalued net asset value (RNAV) valuations. His DDM assumes a risk-free rate of 3.5%, from 1.95% previously, which translates to a total return of 17%. It also assumes a growth rate of 2.5% and a discount rate of 7.9% in his DDM. He is not factoring for any potential earnings accretion or dilution from any unannounced acquisitions.

In addition to his lower target price, Lee has also cut his FY2022, FY2023 and FY2024 distribution per unit (DPU) estimates by 5.9%, 8.0%, and 5.9% to 15.32 cents, 15.76 cents and 16.52 cents respectively. The move is to reflect higher debt costs mitigated by recent acquisitions in Singapore and the US, he says.

For RNAV, the analyst's weighted average cap rate assumes a 5.6% split among 5.7% for Singapore, 4.9% for Australia, 5.6% for the UK, 5.5% for the US and 5.7% for Europe.

In the event of a bull market, which would feature a 50 basis points (bps) compression in risk-free rate, a 50 bps increase in growth rate and a 50 bps compression in Singapore’s industrial cap rate, Lee sees units in CLAR hitting $3.42.

On the other hand, a bear market, which would feature a 50 bps expansion in risk-free rate, a 50 bps decrease in growth rate and a 100 bps expansion in Singapore’s industrial cap rate, he is anticipating CLAR’s unit price to drop to $2.55.

Key downside risks to Lee’s investment thesis that could see CLAR drop below his TP include tenants breaking their long-term leases, affecting Citi’s projected DPU and fair value estimates, and any sharp rise in interest rates that could increase the cost of debt and lower CLAR’s DPU while raising cost of capital, creating a decline in valuation.

Any sharp slowdown in economic activity would also reduce demand for industrial property space and negatively impact occupancy, as well as rental rates of the company’s properties.

Meanwhile, upside risks that could push CLAR above Lee’s TP include stronger-than-expected rental reversions on tighter-than-anticipated demand and supply outlook, higher-than-projected occupancy levels, especially for the older business and science parks, and a pick-up in redevelopment initiatives for older science park properties.

As at 10.50am, units in CLAR are trading 1 cent or 0.37% down at $2.69.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

Citi resumes 'buy' on Digital Core REIT with TP of 82 US cents

Broker's Digest: iFast Corporation, Sea, LHN, Kimly, Del Monte Pacific

Get in-depth insights from our expert contributors, and dive into financial and economic trends