Yahoo Finance

Yahoo Finance CGS-CIMB lifts ComfortDelgro target price following introduction of platform fee via CDG Zig app in Singapore

CGS-CIMB Research keeps “add” call on ComfortDelGro and with a raised target price of $1.55 from $1.47, cites rosy forecast.

With expectations of higher earnings, CGS-CIMB Research analyst Ong Khang Chuen has kept his “add” call on ComfortDelGro C52 and with a raised target price of $1.55 from $1.47.

The new target price, as indicated by Ong in his Oct 10 note, is pegged to a 16.2x FY2024 earnings, 0.5 standard deviation above CD’s five-year historical average.

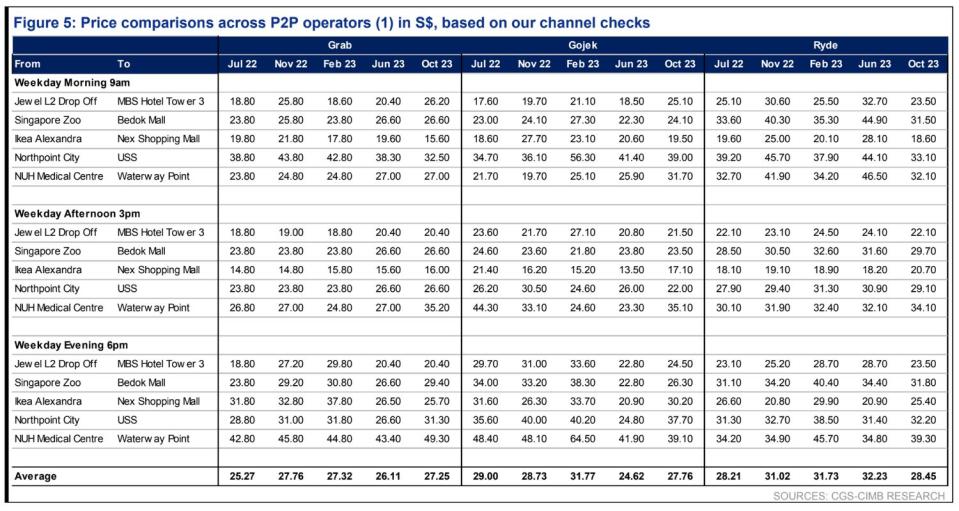

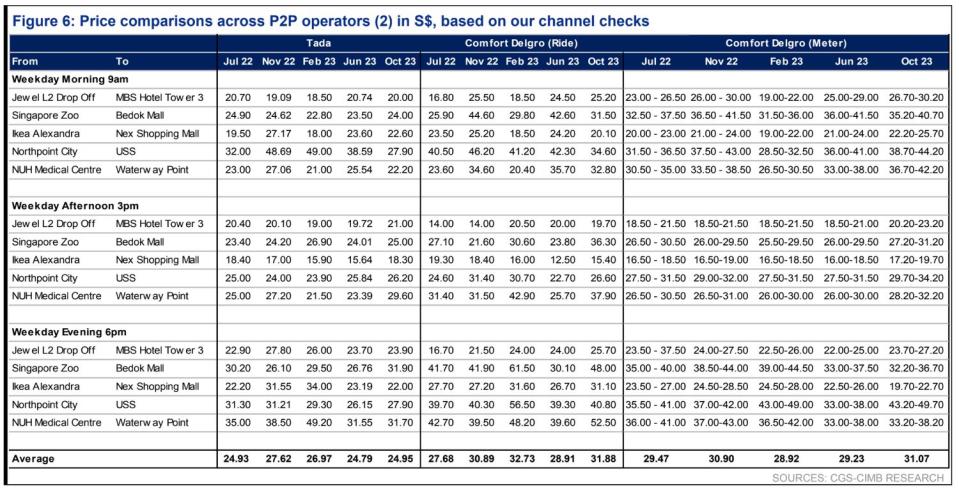

Ong sees higher earnings coming from a few fronts. First, CD, since July, has been charging higher platform fees for users of its Zig booking app, which might generate additional revenue of $6 million for 3QFY2023 alone.

Even so, demand for taxis and point-to-point transport continues to grow. According to Ong, citing his channel checks, fares have remained at high levels. In July, for example, the average daily number of trips increased 5% y-o-y to 613,000.

SBS Transit, CD’s 75%-held subsidiary which is separately listed, runs both buses and trains here. In 1HFY2023, the latter’s train business has turned profitable along with the recovery of passenger volume following the pandemic.

Last but not least, CD, which runs bus services in the UK, had been bearing higher than expected costs in fuel and manpower. It has been able to negotiate a higher operating fee from the UK government.

Ong projects CD to record a patmi of $52 million for 3QFY2023 ended Sept 30, up 14% q-o-q and up 61% y-o-y. For the whole of 2HFY2023, Ong projects earnings growth of 84% y-o-y.

Further down the road, CD has been investing for a more sustainable business. For example, CD has set up a 49%-owned joint venture CDG ENGIE to build 5,000 electric vehicle (EV) charging points in Singapore.

In China, CD has a partnership with Guangzhou Public Transport Group to build an EV charging network for buses and cars in Guangzhou.

Meanwhile, re-rating catalysts identified by Ong include higher commission rates for its taxi segment, and additional tender wins.

Conversely, downside risks include a slower margin recovery due to the inability to pass on costs. With its significant businesses in China, Australia and UK, CD is exposed to currency risks too.

As at 3.15pm, units in CD are trading one cent higher or 0.75% up at $1.34.

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

UOB Kay Hian raises Frencken’s target price on improving semiconductor outlook

CGS-CIMB lowers APAC Realty's TP to 57 cents following higher cost projections

As bulls and bears remain asleep, stay put in high-yield and non-cyclical counters

Get in-depth insights from our expert contributors, and dive into financial and economic trends