Yahoo Finance

Yahoo Finance Should You Buy Canopy Growth (CGC) Ahead of Q4 Earnings?

Canopy Growth Corporation CGC is scheduled to report fourth-quarter fiscal 2024 results on May 30 before the opening bell.

Let’s consider a few factors that might have influenced this cannabis major’s results in this to-be-reported quarter. However, it’s worth examining CGC’s performance in the previous quarter first.

Surprising History and Estimates at a Glance

In the third quarter of fiscal 2024, the company reported a loss of $1.79 compared with the Zacks Consensus Estimate of a loss of 45 cents per share. Canopy Growth missed estimates in three of the trailing four quarters and surpassed in one, the average negative surprise being 94.86%.

The Zacks Consensus Estimate for Canopy Growth’s fourth-quarter fiscal 2024 revenues is pegged at $52.7 million, which suggests a fall of 18.6% from the year-ago reported figure.

The Zacks Consensus Estimate for its fourth-quarter fiscal 2024 loss stands at 33 cents per share, 85.7% narrower than the year-ago reported figure.

Factors to Note Ahead of Q4 Results

On a year-over-year basis, Canopy Growth’s fiscal fourth-quarter sales are expected to be impacted by reduced shipments to the United States due to the ongoing financial difficulties among its distributors. Nonetheless, the business transformation initiatives executed in Canada have significantly improved the company’s gross margins, with the fiscal third quarter being the second quarter in a row of margin expansion in the mid-30s.

The Canadian cannabis business has demonstrated consistent revenue growth in the past four quarters. The quality of its flower offerings is the cornerstone of this impressive revenue streak, further validated by the expansion of its distribution to an additional 900 points nationwide in the third quarter. Demand for high-quality strains such as Tweeds, Kush Mintz, and Tiger Cake remained at an all-time high.

The company also relaunched the Wana edibles brand across Canada in the third quarter with very active retailer engagement. The introduction of new Wana products addressing specific gaps in the current Canadian edibles market is likely to have boosted performance in the fiscal fourth quarter.

Furthermore, the Canadian medical business has achieved record revenues across various periods, driven by the ongoing assortment expansion in the Spectrum store and exceptional patient service. We also expect another strong quarter for Canopy Growth’s Rest of the world cannabis business following a remarkable 81% revenue increase in the fiscal third quarter.

Australia, Poland and Germany may also have strongly contributed to the sales increase. Additionally, the Storz & Bickel segment is likely to have continued seeing a solid uptick in the demand for the new VENTY portable vaporizer.

Bigger Picture Also Appears Bright

Canopy Growth’s top priority lies in becoming a North American cannabis leader. In December 2023, it divested its “This Works” skincare and wellness brand, which is imperative to achieve this vision. Other major actions taken for this transformation include selling off the Canadian retail operations, consolidating the cultivation platform to two purpose-built facilities and discontinuing BioSteel. By concentrating solely on the core cannabis and rightsizing its footprint, the company is now well-positioned to target the most promising markets and geographies.

In the Canadian business, Canopy Growth’s robust new product introduction cycle promises to win market share across priority categories, including pre-rolls, vapes and soft gels. The company will soon launch new large-pack infused pre-rolls and burners and plans to introduce a range of Tweed and 7ACRES-based products with differentiated flavor profiles.

In addition, Canopy Growth’s historical expertise in soft gel backs its significant potential to win share through recently launched and soon-to-come products. Moreover, CGC’s international markets also offer enough scope for growth through the consistency of the flower supply and the onboarding of new distribution partners. The company envisions the new VENTY vaporizer to play a central role in the Storz & Bickel portfolio in the long term, following the footsteps of the iconic VOLCANO.

Furthermore, the Canopy USA strategy has been crucial to gaining exposure to the rapidly growing U.S. cannabis market by bringing together Acreage Holdings, Jetty Extracts and Wana Brands under one umbrella. Apart from their individual growth strategies, the Canopy USA ecosystem companies continue to develop collaborative opportunities and synergies to speed up growth through a unified multi-state operating business. Both Canopy Growth and Canopy USA companies stand to gain significantly from the Department of Health and Human Services’ proposed rescheduling of cannabis to Schedule III under the Controlled Substances Act.

Additionally, they are aiming to achieve positive adjusted EBITDA on exiting fiscal 2024.

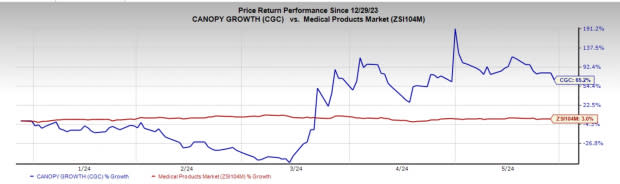

Stock Performance

Year to date, the stock has gained 65.2% of its value compared with the industry’s rise of 3%.

Image Source: Zacks Investment Research

In the past three months, the stock has outperformed the industry’s -2.6% with a staggering 162.9% surge.

We believe that CGC’s shares are attractive at the current level, banking on an innovative portfolio and expanding footprint.

Favorable Estimate Revision

Over the past 30 days, analysts have upgraded the company’s fourth-quarter consensus mark from a loss of 77 cents per share to its current level of a loss of 33 cents. Fiscal 2024’s consensus estimate also underwent a positive revision to a loss of $6.11 from a loss of $6.14 for the same time frame.

Canopy Growth currently has a Zacks Rank #2 (Buy) with a Growth Score of A, a combination that offers a good investment opportunity, per the Zacks proprietary methodology. A Momentum Score of A makes CGC further attractive to investors.

To Conclude

Canopy Growth is on track to achieve profitability and accelerate top-line growth with its strengthened product portfolio while simultaneously advocating for high-potential catalysts. In conclusion, CGC is a buy ahead of its fiscal fourth-quarter results.

Other Stocks to Consider

Here are some other medical stocks worth considering:

Hims & Hers Health HIMS sports a Zacks Rank #1 (Strong Buy) at present. The company’s revenues of $278.2 million in the first quarter of 2024 surpassed the Zacks Consensus Estimate by 2.8%. You can see the complete list of today’s Zacks #1 Rank stocks here.

HIMS’ earnings are expected to surge 263.6% in 2024 compared with the industry’s 16.9% growth. In the trailing four quarters, the company has an average earnings surprise of 79.2%.

HealthEquity HQY carries a Zacks Rank #2 at present. The company reported revenues of $262.4 million in the fourth quarter of fiscal 2024, which beat the Zacks Consensus Estimate by 1.5%.

HQY has an expected fiscal 2025 earnings growth rate of 28.9% compared with the industry’s 12.7%. In the trailing four quarters, the company had an average earnings surprise of 17.4%.

Inogen INGN carries a Zacks Rank #2 at present. The company reported revenues of $78 million in the first quarter of 2024, which beat the Zacks Consensus Estimate by 6.5%.

INGN’s earnings are expected to surge 45% in 2024 compared with the industry’s 13.3% growth. In the last reported quarter, the company delivered an earnings surprise of 18.4%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Inogen, Inc (INGN) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report

Canopy Growth Corporation (CGC) : Free Stock Analysis Report

Hims & Hers Health, Inc. (HIMS) : Free Stock Analysis Report