Yahoo Finance

Yahoo Finance BlackRock: A Wide-Moat Opportunity

Investing guru Warren Buffett (Trades, Portfolio) has historically extolled investing in companies with a wide moat around their business. He said:

"What we're trying to dois we're trying to find a business with a wide and long-lasting moat around it, surround -- protecting a terrific economic castle with an honest lord in charge of the castle."

BlackRock Inc. (NYSE:BLK) is the largest asset management company in the world with roughly $10.5 trillion in assets under management. The company's massive scale provides competitive advantages relative to smaller industry players, resulting in a wide moat. This has allowed it to generate best-in-class returns historically.

Since becoming a public company in 1999, BlackRock shares have delivered a total return of more than 14,000%. Comparably, the S&P 500 has delivered a total return of nearly 700% over the same period.

Over the past 10 years, BlackRock shares have delivered a total return of roughly 252%. Comparably, over the same period, peers such as T Rowe Price (NASDAQ:TROW), Franklin Resources (NYSE:BEN) and Invesco (NYSE:IVZ) have delivered total returns of roughly 106%, -32% and -29%.

While BlackRock is a wide-moat company, it is currently valued more like an ordinary company as it trades at a modest discount to the broader market. Thus, at current levels I believe it represents an excellent opportunity.

BLK Data by GuruFocus

Leading global asset manager

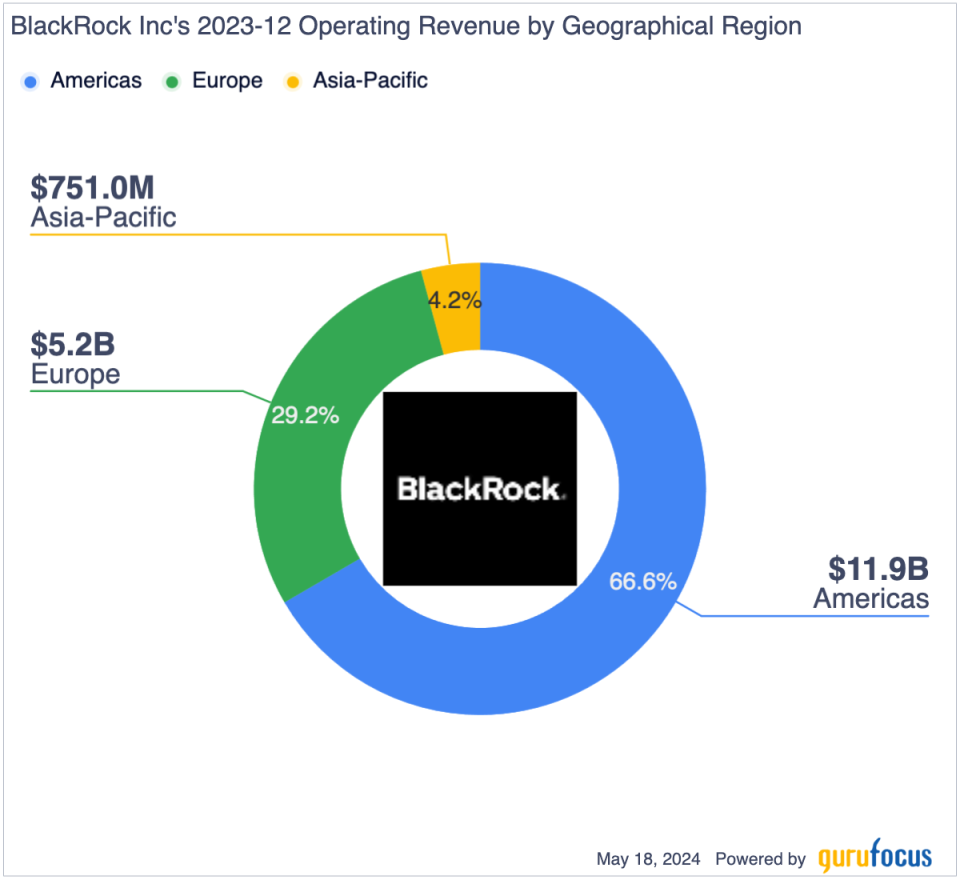

BlackRock is the largest asset management company in the world with roughly $10.50 trillion in assets under management. It offers a wide array of products across both the public and private markets. The company is a global industry leader and generates roughly one-third of its revenue outside of the Americas.

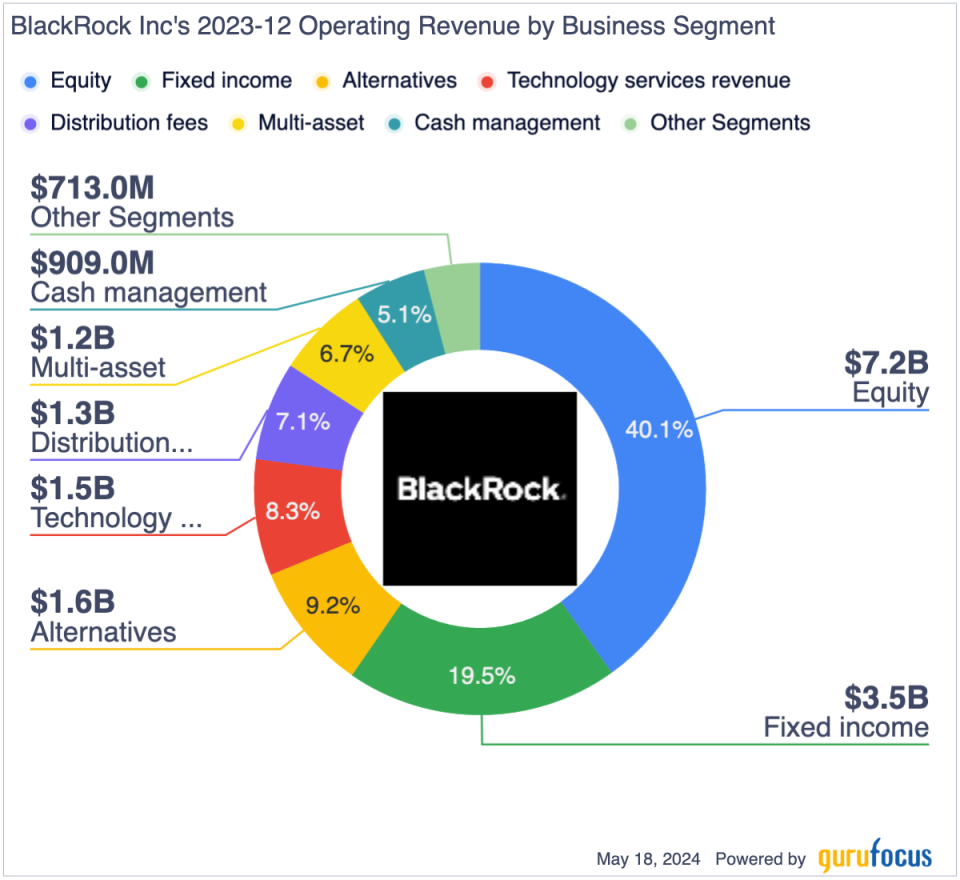

Exchange-traded funds represent a key part of the company's business, accounting for roughly 36% of total assets under management and 41% of base fees. While the vast majority of BlackRock's assets under management are invested in traditional investment strategies focused on public markets, it has a large and growing alternatives business which now accounts for roughly 11% of base fees.

In addition to its asset management business, BlackRock also has a technology services business, which includes Aladdin. Technology services revenue accounts for roughly 8% of total sales.

BlackRock's scale has created a wide moat

The asset management business is highly competitive. BlackRock competes with large asset management companies such as Fidelity, T Rowe Price, Franklin Resources, Invesco, Janus Henderson, Vanguard, PIMCO, Blackstone (NYSE:BX) and many others. Additionally, the company competes with asset management arms of large banks such as Goldman Sachs (NYSE:GS), Morgan Stanley (NYSE:MS) and JPMorgan (NYSE:JPM).

Despite operating in a highly competitive business, BlackRock has been able to build competitive advantages due to its size and scope of operations. The company's massive size allows it to spread shared costs such a technology development, marketing, distribution and operations across a much larger asset base than competitors. Moreover, it benefits from scale in that it generally does not require substantially more portfolio managers and traders to manage accounts. For example, a $10 billion fund with a 1% management fee will bring in $100 million of fees each year, while a $1 billion fund will bring in $10 million in fees. While the $10 billion fund generates 10 times the revenue of the $1 billion fund, it does not require 10 times the cost to operate as a single portfolio management team can easily manage that amount of money.

In addition to benefiting from its size, BlackRock benefits from its scope of operations. By offering everything from passive ETFs to private market alternatives to technology services, the company is uniquely positioned to meet almost any client need. Moreover, BlackRock's scope of offerings often give it multiple touchpoints with a given client, which can be serviced by a single client service team.

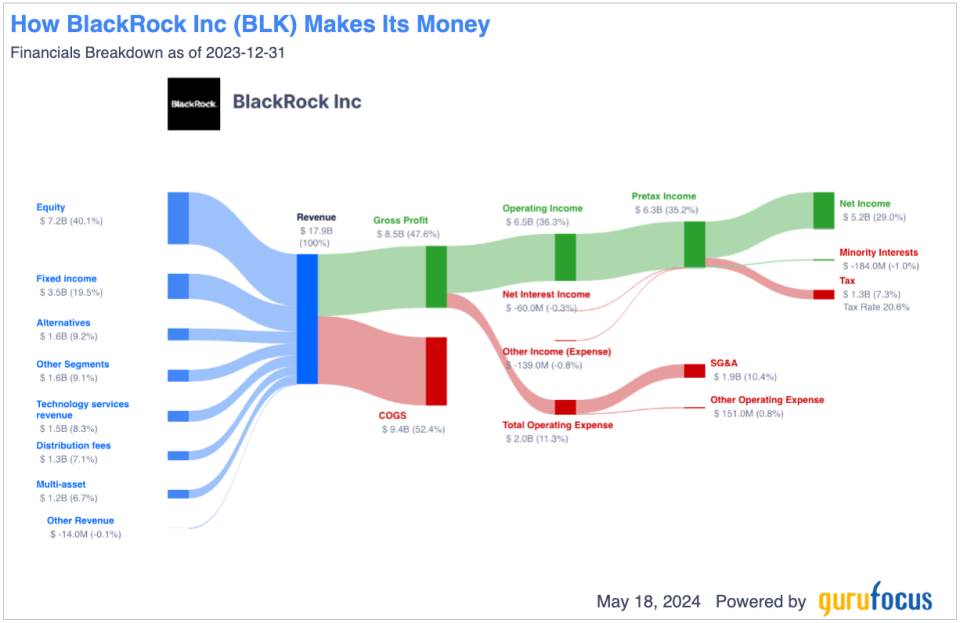

As a result of its competitive advantages, BlackRock has been able to generate best-in-class profit margins of nearly 30%. Comparably, smaller competitors such as Franklin Resources and Invesco generate adjusted profit margins of roughly 21% and 16%.

BlackRock's roughly $10.5 trillion in assets under management is only rivaled by Vanguard, which has approximately $8.20 trillion in assets under management. Fidelity, T Rowe Price, Franklin Resources and Invesco have roughly $5.3 trillion, $1.49 trillion, $1.6 trillion and $1.63 trillion in assets under management respectively. Thus, from a scale perspective, BlackRock has a massive lead and it will be very challenging for any other player to reach a scale close to it. For this reason, I believe BlackRock has a wide moat around its business and it is unlikely competitive pressures will erode BlackRock's dominance of the global asset management business.

Multiple growth drivers lead to accelerated earnings growth

BlackRock has a number of key growth drivers that should allow it to continue growing earnings at a healthy pace going forward. One key driver is increasing assets under management due to rising asset prices and positive returns overtime in equities, fixed income and alternatives. Another key driver of growth will be increased retirement investments driven by an aging population.

Growing interest in alternative investments also represents a key growth driver for BlackRock. The company recently announced plans to acquire Global Infrastructure Partners for roughly $12.50 billion. The deal will further increase BlackRock's scale in the alternatives business by adding roughly $100 billion in assets under management. The company's technology services business, driven by Aladdin, also represents a growth driver due to increased demand for technological solutions in the investment business.

Currently, consensus estimates call for BlackRock to grow full-year 2024, 2025 and 2026 earnings per share at annual rates of 9.6%, 12.7% and 14.9%. This represents an increase compared to the company's historical annual earnings per share growth rate of roughly 9% over the past 10 years. Thus, over the near term BlackRock is likely to experience accelerated earnings growth compared to recent history.

Valuation discount to the broader market

Currently, BlackRock shares are trading at roughly 19.60 times consensus 2024 earnings per share. Comparably, the S&P 500 trades at roughly 21.50 times consensus earnings. Thus, on a relative basis, BlackRock is trading at a valuation discount relative to the broader market despite having better growth prospects over the next few years.

One reason why BlackRock trades at a below-market valuation is its earnings in any given year tend to be highly cyclical as assets under management tend to fluctuate significantly based on market moves.

Historically, over the past 10 years, BlackRock shares have traded at an average price-earnings ratio of roughly 19. Thus, the stock appears to be reasonably valued at current levels compared to historical norms.

BlackRock trades at a valuation premium to peers such as T Rowe Price, Franklin Resources and Invesco, which trade at roughly 13.30, 9.90 and 9.90. Historically, the company has tended to trade at a premium to peers, so current relative valuations are not inconsistent with historical norms. I believe BlackRock deserves to trade at a premium due to its scale advantage and wide moat around its competitive position.

Regulatory risks are limited due to fragmented industry

As the largest asset management company in the world, BlackRock faces potential regulatory risks due to its important position within the global financial system. At some point, regulators could decide its immense scale poses risks to the financial system and thus, policies may be implemented which make it more difficult for the company to continue growing. However, I view this risk as somewhat limited as BlackRock has just 3% of global asset management revenue despite its massive size.

Conclusion

BlackRock is a company with a long history of delivering solid returns for shareholders. The company enjoys a wide moat around its business due to its massive size and scope of operations.

The company has a number of key growth drivers that should allow it to post better medium-term earnings per share growth rates than the broader market. Additionally, BlackRock has sustainable competitive advantages versus peers. However, despite these factors, its shares are currently trading at a modest valuation discount relative to the broader market.

For these reasons, I believe BlackRock is an attractive wide-moat opportunity at current levels.

This article first appeared on GuruFocus.