Yahoo Finance

Yahoo Finance Better Buy: CapitaLand China Trust Vs CapitaLand India Trust

REITs continue to be a preferred source for dividends that are favoured by income-seeking investors.

Despite the headwinds of high inflation and surging interest rates, well-managed REITs with strong sponsors should continue to do well.

One such sponsor is CapitaLand Investment Limited (SGX: 9CI), which has a portfolio of five Singapore-listed REITs.

Of these five REITs, we thought it will be interesting to compare CapitaLand China Trust (SGX: AU8U), or CLCT, and CapitaLand India Trust (SGX: CY6U), or CLINT.

Both REITs are invested in two of the largest countries in the world: CLCT in China, and CLINT in India.

We review each REIT to determine which makes a better investment idea for your buy watchlist.

Portfolio composition

First, we looked at each REIT’s portfolio composition.

CLCT has a total of 20 properties spread out across 12 cities in China.

These properties include a mix of retail and industrial assets such as shopping malls (11), business parks (5) and logistics parks (4).

CLINT, on the other hand, owns just 13 properties in five of India’s top-tier cities.

Its portfolio contains eight IT parks, a logistics park, an industrial facility along with three data centres.

CLCT is the winner here as its portfolio is diversified between two different asset sub-classes and its assets under management are also more than double that of CLINT.

Winner: CLCT

Financials and DPU

Moving on to each REIT’s financials, it’s clear from the table above that CLCT experienced a tough year.

Gross revenue managed to inch up 1.4% year on year because of full-year contributions from the business and logistics parks completed in 2021.

However, distribution per unit (DPU) saw a 14.1% year-on-year fall to S$0.075 because of China’s strict COVID-zero policy.

The REIT manager had to dole out higher rental relief to tenants impacted by the lockdowns, particularly in the second half of 2022 (2H 2022).

2H 2022 also saw downtime due to asset enhancement initiatives for various malls within CLCT’s portfolio.

CLINT saw healthy growth for gross revenue, net property income and DPU as the REIT enjoyed higher portfolio occupancy.

Despite retaining 10% of distributable income, the industrial REIT still saw a 5% year on year rise in DPU to S$0.0819.

CLINT’s portfolio valuation also saw an encouraging 11.7% year on year jump (in Indian Rupee terms) to INR 150.4 billion and was much higher than the 2% year on year increase in CLCT’s portfolio valuation to RMB 25.2 billion.

Winner: CLINT

Debt metrics

In light of higher interest rates, we look at each REIT’s gearing ratio, cost of debt and level of fixed-rate borrowings.

Although CLCT has a higher gearing ratio than CLINT, it has the advantage of having a much lower weighted average cost of debt of close to 3% compared with the latter’s 5.9%.

CLINT has a slightly higher level of fixed-rate loans but also has a lower interest cover ratio.

Another plus point is that CLCT has quantified the effects of the rise in interest rates so that investors can better understand its DPU sensitivity. CLINT, however, provided no such information.

Winner: CLCT

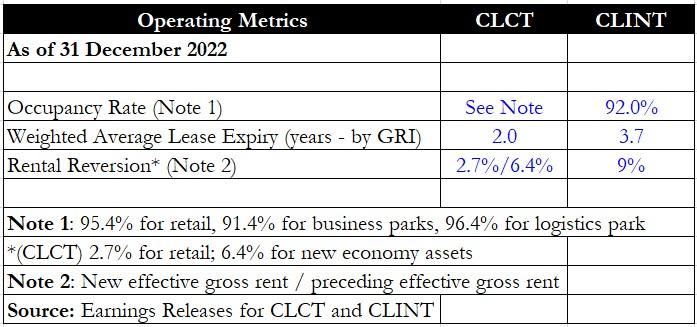

Operating metrics

Operating metrics are another important aspect to review for REITs.

For occupancy rates, both CLCT and CLINT enjoy high rates of above 90%.

CLINT, however, boasts a longer weighted average lease expiry (WALE) at 3.7 years compared to CLCT’s two years.

For rental reversion, CLINT also logs a much higher 9% year on year positive reversion compared with CLCT.

Winner: CLINT

Distribution yield

Finally, we come to the most important attribute of each REIT – its distribution yield.

CLINT wins this round as it boasts a distribution yield of 7.7% versus CLCT’s 6.6%.

Winner: CLINT

Get Smart: Catalysts and continued transformation

Although CLCT saw its DPU decline and also has a lower distribution yield, it’s good to obtain some perspective for each REIT over the past three years.

CLINT saw its DPU fall from S$0.0883 in 2020 to S$0.0819 in 2022 for a decline of 7.2% over two years, while CLCT’s DPU climbed 18.1% during the same period from S$0.0635 to S$0.075.

2022 can be viewed as a tough year for CLCT because of China’s zero-tolerance stance on COVID-19, thus adversely impacting the REIT’s portfolio of retail malls.

Looking ahead, with China’s relaxation and border reopening, CLCT’s malls should enjoy a reprieve, thereby putting the REIT back on track to generate higher rental income without any more rebates.

With CLINT’s significantly higher cost of debt, there is a high chance that continued rises in interest rates may crimp DPU.

Hence, we feel that CLCT should be the overall winner.

Is it a good time to buy into Singapore REITs? If you’ve thought about it, then our latest REITs guide will be an essential read. This exclusive pdf report shows you why REITs are still excellent assets, what sectors to look out for and how to find good REITs today. The info inside can help you build a solid retirement portfolio. Click here to download it for FREE.

Follow us on Facebook and Telegram for the latest investing news and analyses!

Disclosure: Royston Yang does not own shares in any of the companies mentioned.

The post <strong>Better Buy: CapitaLand China Trust Vs CapitaLand India Trust</strong> appeared first on The Smart Investor.