Yahoo Finance

Yahoo Finance Analysts positive on S-REITs as tapering hike momentum 'turns the tide'

CGS' top picks for S-REITs are ART, CDLHT and FEHT

DBS Group Research analysts Geraldine Wong, Derek Tan, Rachel Tan and Dale Lai are optimistic on the Singapore REITs (S-REITs) sector. This is in light of having much economic tumult blown over for the sector, as the Fed hike momentum tapers and inflation levels wane, the analysts write in their Aug 1 report.

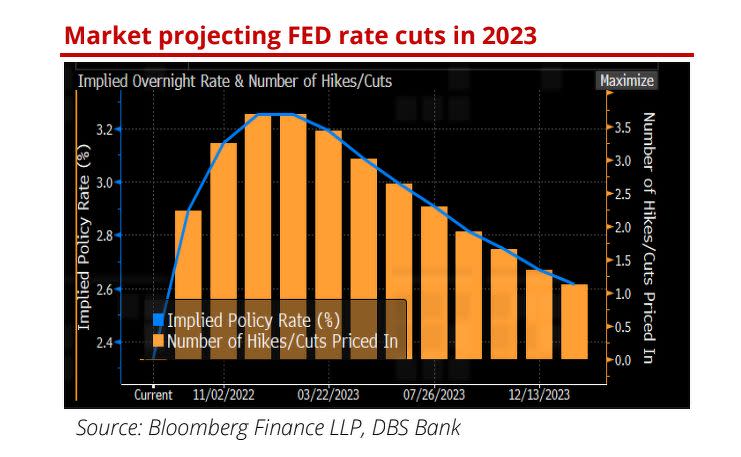

The Fed has hiked by 75 basis points (bps) which resulted in a strong rally in the US indices. In addition, guidelines on forward hikes appear to suggest a slowdown in the pace of rate hikes.

The analysts view this “small pivot” by the Fed to be a significant guidance, opening the door to a downshift in hikes in 2HFY2022 ending December.

“At this stage, we are now past the “three peaks” – peak inflation, peak Fed action, and peak Fed rhetoric, which has been an overhang for the S-REITs,” they write.

The analysts see a stronger backdrop for the S-REITs in 2HFY2022 as they see the unwinding of themes such as a strong US dollar and higher rates. “As such, while the S-REITs have underperformed in the 1HFY2022 down 3.4% compared to the Straits Times Index (STI)’s 2.3% rise, we sense the ‘turn of the tide’, especially with the market focusing on possible rate rates in 2023,” they say.

“Our economists are projecting that SG 10-year yields will peak out in 3QFY2022 at around 3.2% before declining towards 2.65% by end of 2023 on the back of lower inflation and an economic slowdown,” the analysts add. At a FY2023 yield of 6.1%, this implies that the current yield will expand from an expected 3.3% to 3.5% over time.

The S-REITs have held steady in July, the analysts observe, up 0.6% though underperforming as compared to the 2.2% rise in the STI.

Amongst the various subsectors, the industrial S-REITs are up 2.4% for large caps and 1.9% for mid-caps, with Retail S-REITs up 2.1%, given the respective sectors’ perceived resilience against economic slowdown.

Office S-REITs (-1.3%) and hospitality S-REITs (-1.1%) declined given their closer correlation to economic growth, say the analysts.

In terms of stocks, best performers are Daiwa House Logistics Trust (DHLT), up 7.7%; Mapletree Logistics Trust (MLT), up 4.1%; and Mapletree Industrial Trust (MLT), up 3.4%.

On a whole, with the current interim results season still underway, S-REITs that have reported results showed a strong rebound in earnings for 1HFY2022 to the analysts, on the back of positive organic growth prospects with robust guidelines in 2HFY2022. “We saw strong rental reversions seen in the office, industrial and retail spaces,” write the analysts.

Notably, the hospitality space is seeing a strong revenue per available room (RevPAR) rebound in 2QFY2022, with most hoteliers reporting RevPAR upside over 50% y-o-y from pent-up leisure demand.

In a separate report, CGS Group Research analyst Lock Mun Yee is “overweight” on S-REITs, seeing how hospitality REITs have been boosted by strong demand, delivering a robust set of 1HFY2022 results driven by an improvement in RevPAR in most markets they are in.

“There has been strong growth in 2QFY2022 RevPARs surpassing 2019 levels in several markets, though China and Japan continue to lag recovery due to travel restrictions,” says Lock.

The Singapore Tourism Board (STB) projects tourist arrivals to reach 4 million-6 million in 2022, or 21%-32% of 2019 levels. For June, Singapore recorded 1.5 million inbound tourists.

Hospitality REITs indicated that business demand has picked up, says Lock, particularly from small- and medium-sized enterprises (SMEs) and project group bookings, although larger scale corporate bookings are still absent. That said, the current occupancy levels have enabled hotel operators to execute yield management strategies across their portfolio.

Moreover, hoteliers have regained pricing power on the back of strong demand, observes Lock. “In addition, the short stay profile provides REITs with pricing flexibility to raise prices to offset inflationary costs, enabling them to preserve margins,” she adds.

In Singapore, while the hospitality market is experiencing a strong recovery, CDL Hospitality Trusts (CDLHT) and Far East Hospitality Trust (FEHT) have retained two and four hotels on government contracts respectively. “We believe this would bolster portfolio occupancy levels while generating better returns as they have been re-contracted at higher rates,” says Lock.

The analyst also observes how hospitality REITs balance sheets remain robust with gearing levels ranging from 33.3% for FEHT, 37.5% for Ascott Residence Trust (ART) and 39.5% for CDLHT, as at end-1HFY2022.

In addition, the REITs have hedged between 60.9%-79% of their debt into fixed rates. In terms of impact, every 25 bp change in average funding cost would impact CDREIT, ART and FEHT’s distribution income by 2%, 0.9% and 1% respectively, explains Lock. With cap rates still remaining stable, hospitality REITs indicated that they would continue to tap into acquisition growth opportunities.

CGS’s hospitality top pick is now FEHT as it continues to benefit from demand recovery in its hotel and service residences (SR) segments while the stated distribution of divestment gains would provide an upside kicker.

The analyst places an “add” rating on FEHT with a target price of 78 cents. “Strong corporate demand has resulted in SR revenue per available unit (RevPAUs) [for FEHT] surpassing pre-Covid-19 levels, while its newly revamped hotel offerings have allowed it to better compete with its peers and drive higher room rates,” writes Lock.

FEHT’s 1HFY2022 distribution income of $30.6 million, inclusive of divestment gains of $1.6 million, was slightly above the analyst’s expectations, underpinned by a 31.4% and 31.9% rise in the RevPAR of its hotel and SR segments.

Lock observes FEHT’s capital gain distributions amounting to $8 million per annum (p.a.) or 0.47 cents/unit for three years, arising from the divestment of Central Square, providing an added yield uplift on top of her 4.3%/5.5% FY2022/FY2023 distribution per unit (DPU) yield.

Other picks by CGS-CIMB include ART and CDREIT, where Lock accords “add” ratings to both REITs as well and target prices of $1.24 and $1.38 respectively.

For ART, its geographically diversified portfolio of SRs, business hotels and extended stay assets strike a balance between stable and growth income, says Lock, with long-stay demand providing stability that is highly valued in a hospitality counter, while shorter-stays allow it to drive rates, providing earnings upside.

Lock also observes that ART recorded a 13.6% y-o-y rise in DPU as RevPAU ticked up 85% q-o-q to $124, its eighth consecutive quarter of RevPAU improvement.

“With 66% assets under management (AUM) in Singapore, CDLHT is a proxy for the recovery of the Singapore hospitality sector,” writes Lock. “Asset Enhancement Initiatives (AEIs) undertaken at several of its properties and strong demand across its other key markets of Australia, Maldives and UK will continue to support further RevPAR growth.”

Hospitality REITs such as ART and CDLHT are trading at around 1.01x P/NAV while FEHT is trading at 0.75x P/NAV. ART and CDLHT 1HFY2022 DPU came in above the analyst’s FY2022 expectations while FEHT missed.“Nonetheless, we believe net asset value (NAV) would likely remain robust on the back of strong operating performance,” says the analyst.

Overall, Lock believes that the upward momentum of demand from both domestic and international travel would continue for the rest of FY2022, where the reopening of borders and resumption of global travel will underpin demand for hotel and serviced residence accommodation.

As at 11.53am, units in ART, CDLHT and FEHT are trading at $1.16, $1.29 and 64 cents respectively.

Photo: Albert Chua/The Edge Singapore

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

‘Stronger growth pipeline’ for KIT, Basslink troubles behind it: DBS

Market outlook in August to follow historical pattern of post-July slump: DBS

Analysts from DBS, OCBC and UOB Kay Hian increase their TPs as SIA outperforms 1Q expectations

Get in-depth insights from our expert contributors, and dive into financial and economic trends