Yahoo Finance

Yahoo Finance 94% of S’pore business leaders surveyed not accounting for Scope 3 emissions: ISCA, Schneider Electric survey

Scope 3 continues to be tricky for local business leaders, despite the category contributing up to 80% of the typical firm.

Measuring and reporting Scope 3 emissions, such as emissions arising from business travel and the value chain, continue to be challenging for the majority of companies here. This is despite the category contributing up to 80% of the average organisation’s greenhouse gas emissions.

A survey of over 500 of Singapore’s senior business leaders found that just 6% are fully measuring and analysing their firms’ Scope 3 emissions. This significantly lags behind their measurement of Scope 1 (52%) and Scope 2 (30%) emissions.

Released on July 2, the joint study by Schneider Electric and the Institute of Singapore Chartered Accountants (ISCA) also found strong correlation between executives’ seniority and their Scope 3 knowledge. Board members scored higher in their understanding of Scope 3 emissions (58%) than C-suites (51%), directors (30%) and senior managers (27%).

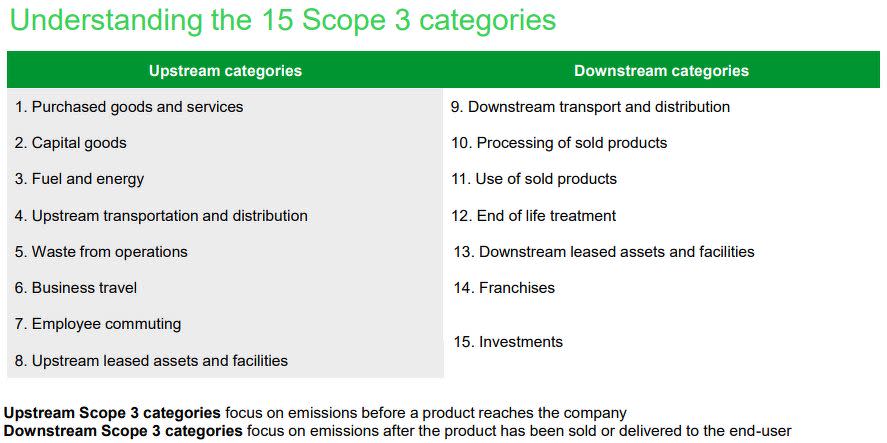

Scope 1 emissions are typically generated by an organisation’s operations, while Scope 2 emissions are largely calculated from a firm’s purchased electricity, heat, steam or cooling.

In contrast, there are 15 categories of Scope 3 emissions, split between upstream and downstream categories. They include purchased goods and services, capital goods, franchises, business travel and employee commuting, among others.

According to the “Counting to 3: Navigating Singapore’s Emissions Journey Together” study, only 27% of leaders surveyed believe their organisation’s Scope 3 targets are highly achievable.

Their confidence in meeting their firms’ Scope 3 emissions targets is also significantly lower than that of their Scope 1 (40%) and Scope 2 (31%) emissions targets.

That said, leaders from larger businesses are significantly more likely to indicate they have set targets for Scope 3 (54%) compared with those at small businesses (31%).

According to respondents, a lack of human resources and expertise is the biggest barrier to improving Scope 3 emissions management. Other challenges include financial constraints, commercial motivation and access to fit-for-purpose technological infrastructure.

Scope 3 emissions are the next frontier of emissions management, but are still uncharted territory for many organisations in Singapore, says Yoon Young Kim, cluster president, Schneider Electric Singapore and Brunei. “Education is critical for advancing Singapore’s green agenda. We see correlations throughout the findings of this study that a lack of understanding of key areas of management of greenhouse gas emissions leads to a lower level of planning, target-setting and, ultimately, action.”

Accountancy and finance professionals are well-placed to take on the role of sustainability reporting, says ISCA, echoing Minister for Sustainability and the Environment Grace Fu’s comments from March.

The accountancy body believes the skillsets of accountants are transferable to sustainability reporting, including Scope 3 emissions reporting.

Kang Wai Geat, divisional director, professional standards, ISCA, says sustainability is a “megatrend” reshaping the accountancy profession. “Increasingly, organisations are turning to the accountancy profession for sustainability reporting and assurance. To take full advantage of the opportunity to help organisations advance their emissions agenda, accountants must upskill and reskill to keep up with the latest developments in sustainability.”

Kang adds: “The accountancy profession is key to reporting sustainability performance to shed light on how companies earn their profits. Having consistent and comparable sustainability reporting will help stakeholders make informed decisions in support of sustainability.”

Table: ISCA, Schneider Electric

See Also:

Click here to stay updated with the Latest Business & Investment News in Singapore

ISCA, Council for Board Diversity sign MOU to improve support for Singapore’s board directors

Get in-depth insights from our expert contributors, and dive into financial and economic trends