Yahoo Finance

Yahoo Finance 3 Key Factors Driving Nu Holdings' Unprecedented Growth and Efficiency

With rapid expansion in Latin America, particularly in Brazil, Nu Holdings Ltd. (NYSE:NU) has emerged to facilitate access to credit compared to traditional banking alternatives in the region. Through an entirely digital, intuitive platform with no transaction fees and excellent customer service, the company has achieved the remarkable feat of attaining more than half of Brazil's adult population as its customers.

In addition to rampant growth and almost 100 million customers, the company has demonstrated its ability to effectively monetize its user base, proving to be a profitable player with higher efficiency levels than traditional banks.

This balance of growth and profitability has even attracted the attention of highly renowned investors, such as Warren Buffett (Trades, Portfolio), who holds a significant stake.

As such, I am bullish on the stock for three main reasons.

Why is Nu Holdings so special?

Nu's story exemplifies how technological innovation can revolutionize traditional sectors, offering enhanced value and superior customer experiences. Today, the company stands out as a leader in the fintech market in Brazil and across Latin America.

Founded in 2013, it is a relatively new digital bank born out of its founders' frustration with the bureaucracy and high costs of traditional banks in Brazil. Their mission was to create a digital bank that offers a straightforward, transparent experience without exorbitant fees.

With the evolution of technology, Nu Holdings' Nubank launched its first product in 2014: a credit card with no annual fee, entirely managed through a mobile appa novel concept in the South American country.

The digital bank quickly gained traction, attracting investments from major funds. It later introduced NuAccount, a free digital account offering fee-free transfers and automatic balance returns. These innovations propelled Nu Holdings to unicorn status (valued at over $1 billion) by 2018.

Fueling its growth, Nu Holdings expanded operations into Mexico and Argentina in subsequent years. In 2021, the company conducted its initial public offering on the New York Stock Exchange, solidifying its position as one of the largest fintechs globally.

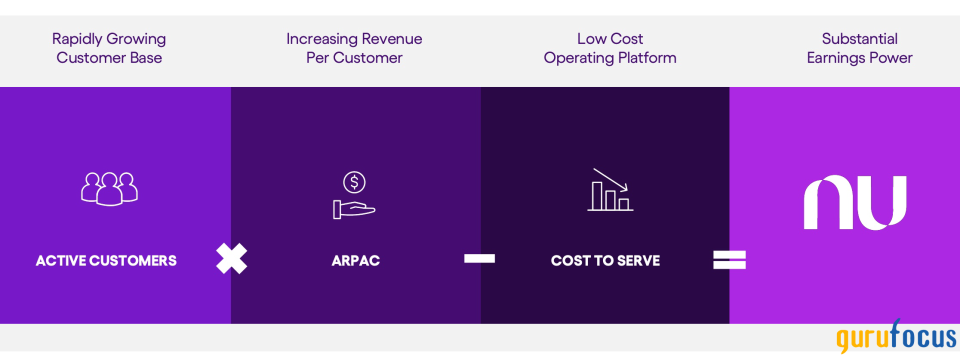

Nu follows a formula that has driven its rapid and substantial growth over the past decade. This formula multiplies active customers by average revenue per active user (ARPAC) and subtracts the cost to serve, resulting in significant earnings power. These components are precisely what, in my view, make it exceptional in the fintech and digital banking landscape.

Source: Nu Holding's Investor Relations

Rapidly growing customer base

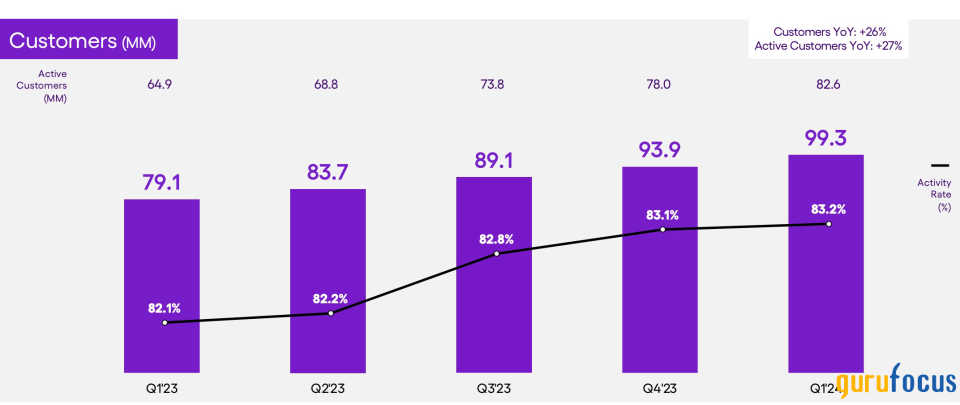

The first factor driving my bull thesis is its rapidly growing customer base. Nu Holdings has nearly doubled its expansive customer base in the past two years, achieving a compound annual growth rate of 29% from first-quarter 2022 to first-quarter 2024. The digital bank boasts 99.3 million customers, marking year-over-year growth of 20.20 million. This growth has positioned Nu Holdings to reach 54% of Brazil's adult population, with 83% of these customers being active every month.

Source: Nu Holding's Investor Relations

Despite already having the world's largest digital bank customer base, Nu Holdings anticipates continued expansion as it penetrates new markets in Latin America, particularly Mexico and Colombia.

In Mexico, where credit card penetration is notably low, Nu has achieved milestones comparable to its early stages in Brazil. As of the first quarter, Mexico registered 6.60 million customers, including 3.20 million active credit card users and 3.10 million active NuAccounts. By comparison, in fourth-quater 2018, Brazil had only 6 million customers, 4.5 million active credit card users and 1 million NuAccounts.

Given this growth trajectory in Mexico, it is likely this operation will soon become significantly relevant for sustaining the overall growth of new accounts.

Increasing revenue per customer

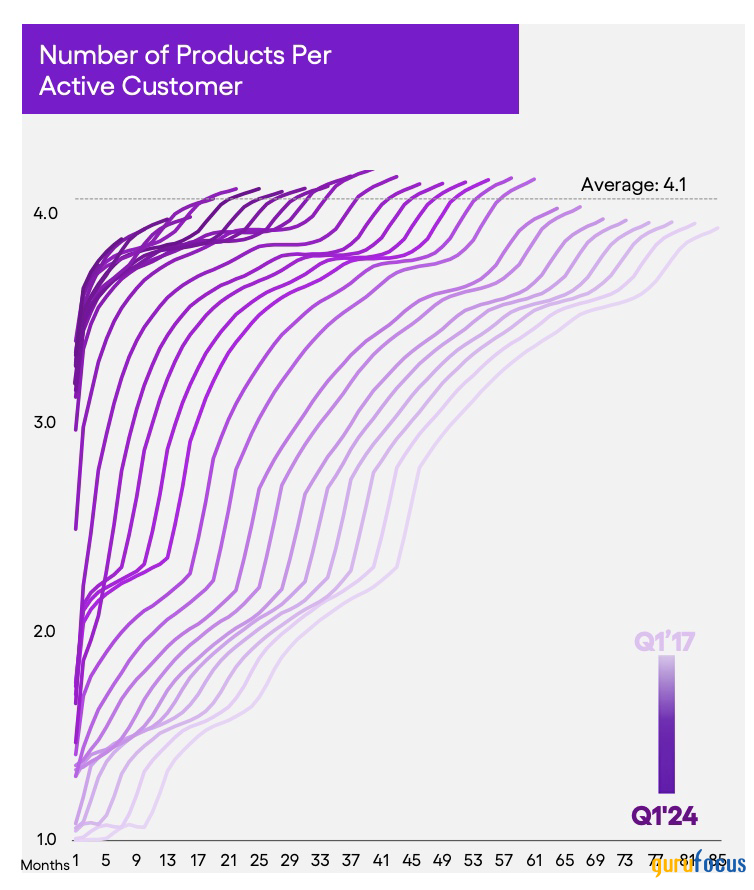

Next, Nu Holdings has not only rapidly expanded its customer base, but also efficiently monetized it. In the first quarter of 2024, the average revenue per active customer increased by 30% year over year, reaching $11.40. This growth has been a significant driver of Nu Holdings' overall revenue, which saw a 64% year-over-year increase fueled by customer acquisition and ARPAC expansion.

This revenue growth is supported by Nu Holdings' effective utilization of cross-selling and up-selling opportunities within its substantial customer base. From first-quarter 2017 to first-quarter 2024, the average number of products per active customer has risen from one to four. These additional products include credit cards, loans, credit lines, insurance and brokerage services. On the up-selling front, the bank has succeeded in offering higher-tier credit cards, paid subscriptions and personalized financial planning services.

Source: Nu Holding's Investor Relations

In the card business specifically, Nu has achieved a 30% year-over-year increase in purchase volume on a foreign exchange-neutral basis, totaling $31.10 billion, sustaining its robust growth trajectory. According to the company, the compounding effect of adding millions of new customers each month, coupled with the maturation of these customers into historically observed spending patterns, is expected to support future growth in purchase volumes at Nubank strongly.

Low-cost operating platform

Finally, Nu Holdings stands out with its best-in-class cost structure, which has enabled it to achieve significant operating leverage.

The digital bank spends $7 on customer acquisition costs, with only $2 allocated to marketing and the remainder to onboarding expenses. This ratio is favorable, especially considering the current ARPAC of $11.40, indicating efficient customer monetization. Additionally, Nu Holdings maintains a remarkably low cost to serve per customer, averaging 90 cents, approximately 85% lower than other incumbent banks.

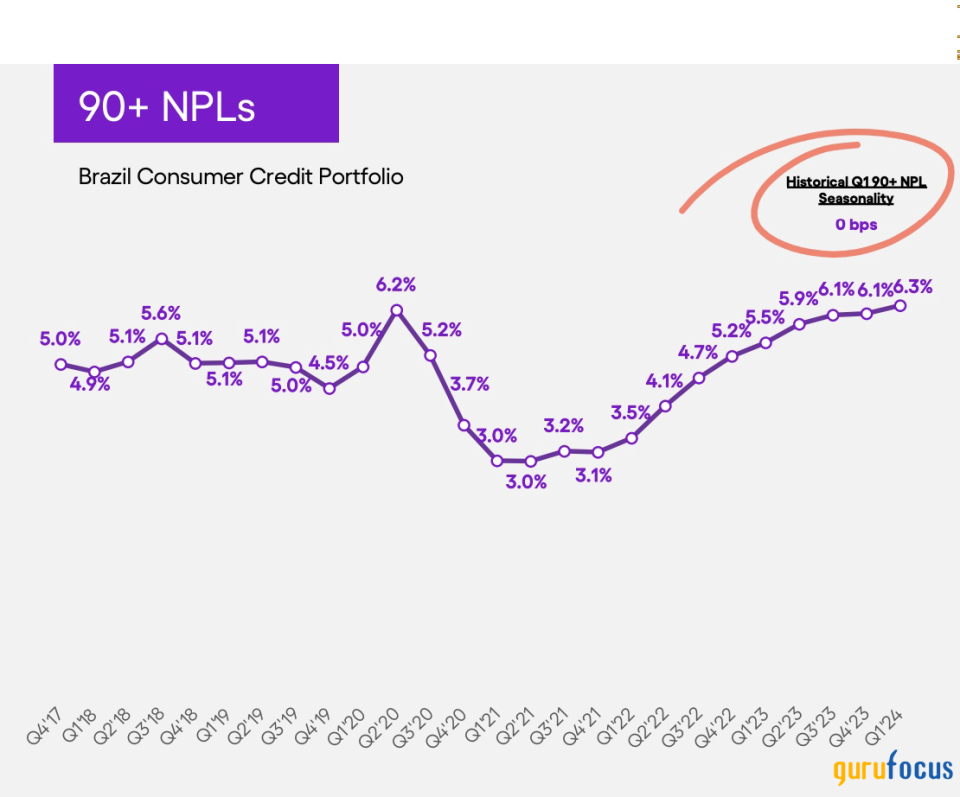

Regarding risk management, Nu reports a cost of risk that includes a consumer finance delinquency rate of 6.30%, approximately 10% lower than the industry average in Brazil. This reflects successful risk management practices, which are particularly noteworthy considering the rapid growth in digital banking and the potential for increased risk exposure in a country like Brazil during a period of extensive credit expansion.

Source: Nu Holding's Investor Relations

In terms of funding costs, Nu holds $24.30 billion in deposits and maintains a competitive funding cost at 84% of the blended interbank rates in Brazil and Mexico. This positioning narrows the gap compared to incumbent banks and widens the advantage over consumer fintechs.

Overall, the company's efficient cost structure across acquisition, servicing, risk management and funding underscores its ability to sustainably scale operations while maintaining profitability and a competitive edge in the fintech sector.

Conclusion

Nu Holdings' earnings formula has proven to be exceptionally successful. By multiplying the three factors mentioned aboveactive customer base, robust ARPAC and low cost to serveNu Holdings has achieved substantial earnings power. Net income surged from $141.80 million in first-quarter 2023 to $378.80 million in the most recent quarter, accompanied by a net margin of 14%. The annualized return on equity (ROE) stood at 23%, surpassing that of incumbents like Banco do Brasil (BSP:BBAS3) and Itau Unibanco (NYSE:ITUB), which reported ROEs of 21%. This achievement is notable for a digital bank that has been in existence for only a decade.

Of course, a business with high quality and high growth potential comes at a high cost. Given Nu Holdings' forward price-book ratio of 6.80, significantly higher than the industry average of 1, investing in the stock at current prices suggests a potential return five times greater than the industry norm.

Indeed, these metrics carry high risks, and Nu Holdings needs to sustain its current pace of growth and operational leverage in the long term, particularly in controlling delinquencies. However, based on consensus using the five-year book value growth rate for banks, Nu Holdings currently trades at a PEG ratio of 0.40. This suggests a discounted valuation relative to its future growth potential.

With that said, I continue to believe Nu Holdings, as one of the most efficient financial services companies in the world, is poised to benefit from the full potential of its platform's operating leverage as it continues to grow its customer base, upsell and cross-sell products, launch new features and eventually achieve profitability in new markets like Mexico and Colombia, which are still in their investment phases.

This article first appeared on GuruFocus.