Yahoo Finance

Yahoo Finance VICI Properties: A Value Grab in an Overpriced Market

Finding undervalued bargains is challenging in the current economic environment. Since the beginning of the year, the market has been highly volatile and the trajectory of interest rates is uncertain, yet stocks are at an all-time high. The current Shiller PE ratio for the S&P 500 is at 35 against historical averages of around 17, and the Buffett Indicator is 184.70%, suggesting the market is heavily overbought. While glowing reports of unexpected profits and predictions of a soft landing occurred in the third quarter of 2023 to boost investor optimism, analysts caution investors to stay conservative. The January inflation report exemplifies that sentiment.

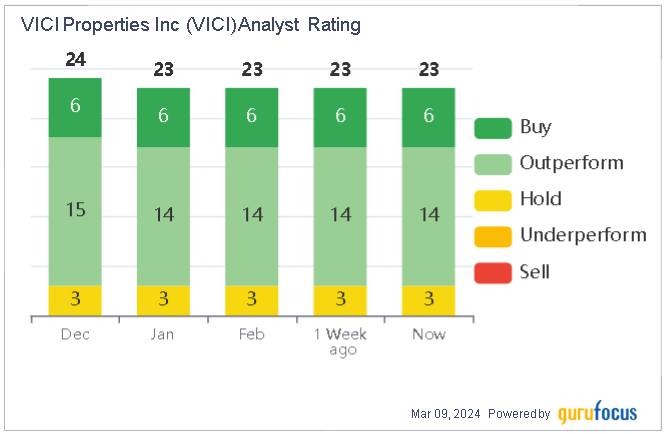

One hidden gem is VICI Properties Inc. (NYSE:VICI), a real estate investment trust that focuses on the gaming, hospitality, entertainment and leisure businesses. The stock has garnered positive analyst reviews with an average broker recommendation of outperform. As of March 8, GuruFocus lists the stock as moderately undervalued selling at a discount of 28.60% and gives it a GF Score of 89 out of 100 and a value score of 10 out of 10. The stock has an annual forward dividend yield of 5.62% and is currently trading at $29.12.

Industry and competitive landscape

The Gaming REIT sector, also known as the Casino REIT sector, is a relatively new area of real estate companies that lease land or properties to businesses focused on casinos, resorts, hotels and racetracks. The gaming REIT sector was created in 2013 with the development of Gaming and Leisure Properties Inc. (NASDAQ:GLPI), the first entrant into the space. The second entrant, MGM Growth Properties (MGP), went public in 2016 and VICI Properties became public in 2018. VICI acquired MGM Growth Properties in April 2022, reducing the public playing field to two companies. Gaming and Leisure Properties is the only pure-play publicly traded REIT in the gaming space. VICI Properties refers to itself as an experiential REIT. In addition to its gaming properties, comprising approximately 57% of its portfolio, VICI owns properties tied to four golf courses (operated by CDN Golf Management, an affiliate of Cabot) and 39 bowling alleys (operated by Bowlero.)

Blackstone Real Estate Investment Trust, a non-traded REIT and part of Blackstone's (NYSE:BX) product line, entered the gaming REIT space in 2019 when Blackstone acquired the real estate assets of the Bellagio from MGM Resorts International (NYSE:MGM). The following year, BREIT formed a joint venture with MGM Growth Properties to purchase the property assets of MGM Grand Las Vegas and Mandalay Bay. BREIT further expanded its position on the Las Vegas Strip through net-lease investments with the Cosmopolitan and the Bellagio. However, more recently, the REIT appears to be divesting gaming assets, as indicated by the sale of its stakes in MGM Grand Las Vegas and Mandalay Bay property assets to VICI in December 2022. BREIT also sold assets in the Bellagio to Realty Income Corp. (NYSE:O) in August of 2023. Currently, gaming property assets comprise approximately 5% of BREIT's portfolio.

In addition to the Bellagio property, Realty Income bought the property assets for Encore Boston Harbor from the Wynn Resorts (NASDAQ:WYNN) in February 2022. Combined with the Bellagio transaction, Realty Income's gaming property assets comprise approximately 3.90% of its portfolio.

In-person gambling still dominates the industry with enthusiasts citing the draw of the emersion experience of social interactions with other gamblers and immediate access to winnings; however, online betting appears to be encroaching on the space as in-person gambling comprised 75.30% of revenue during 2023 versus 80.50% in 2022.

Spinoff origins

Both VICI and Gaming and Leisure Properties were created as spinoffs in which the property assets of gaming operators were spun off into REITS that leased those assets back to the original companies. VICI was created in 2017 when it purchased the property assets of Caesars Entertainment Operating Company (NASDAQ:CZR) as part of the latter company's Chapter 11 bankruptcy restructuring. Gaming and Leisure Properties was created in 2013 when it was spun off from Penn National Gaming. Spinoff tactics were also used in the BREIT/MGM Growth Properties and BREIT/Realty Income transactions mentioned above.

Gaming REITS typically use triple net lease models, in which the tenant (also known as the gaming operations company) is responsible for real estate taxes, building insurance and maintenance costs in addition to costs for rent and utilities. This agreement provides tenants with generally lower rents and direct control over the rental properties while providing investors with low-risk and steady income streams.

On the other hand, sale-leaseback arrangements enable gaming operators to sell their property assets to REITS to raise capital and lighten their asset bases. Operators are then required to lease the sold property back from the REIT.

Investor sentiment toward gaming REITS

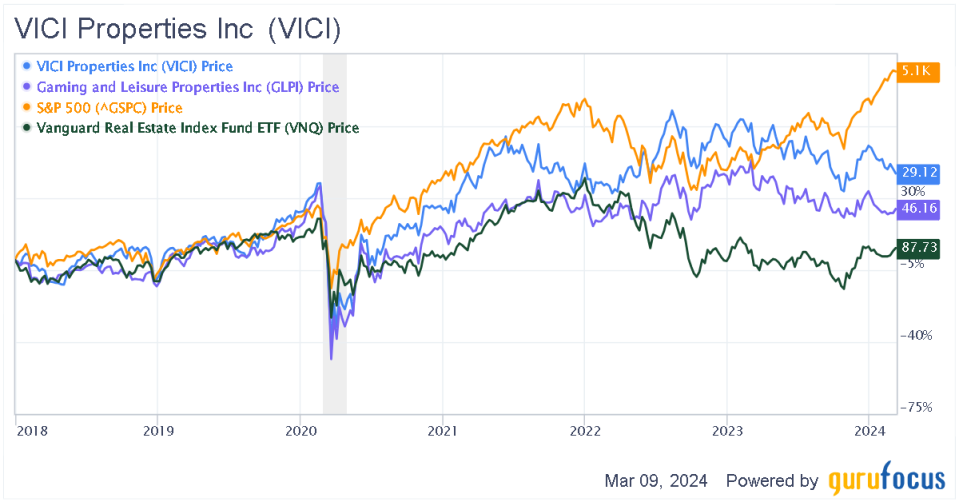

Since VICI's inception, investors have been more receptive toward gaming REITS than they have been toward the greater real estate market, which has received downward pressure due to vacancy rates of office REITS and other sectors after the Covid-19 pandemic and the rising interest rate environment. The gaming REIT sector has outpaced the wider REIT market by nearly 2 times; however, the sector has underperformed the S&P 500 Index by over the same amount. The chart below illustrates the share performance of VICI and Gaming and Leisure Properties against the Vanguard Real Estate Index Fund ETF (VNQ) (a proxy for the general REIT market) and the S&P 500 Index (^GSPC).

VICI Data by GuruFocus

VICI's capital allocation pros and cons

VICI was saddled with over $2 billion in debt when it emerged from the bankruptcy proceedings of Caesars Entertainment Operating Company. The company faced resistance from both investors and lenders when raising capital. The board selection process addressed these concerns by recruiting individuals with hospitality, gaming and REIT experience. The board also faced the challenges of deleveraging a debt-laden balance sheet, reliance on only one tenant, building competent management and developing governance practices that balanced action with risk management. According to Board Chair James Abrahamson:

"We did not have the time or the capacity to develop or execute a risk-free strategy. We needed to quickly establish a strong board culture, sound governance practices, and a highly effective board-management relationship that could act decisively and quickly to fix our problems and seize every opportunity we could generate."

The board selected hospitality industry REIT veteran Edward Pitoniak as CEO, who, in turn, chose an executive team with the expertise needed for governance of the newly created REIT.

Pitoniak first addressed VICI's pre-initial public offering debt levels, which were 10.50 times its expected first year, by meeting with prospective investors and discovering their willingness to accept debt-for-equity swaps that reduced the debt to 8.50 times Ebita; however, Pitoniak concluded that VICI would need to further reduce the ratio by growing Ebita for a viable IPO.

Concurrently, Ceasar approached VICI about purchasing Harrah's Las Vegas for $1.10 billion. To finance this transaction, VICI's management opted for investor equity dilution through a debt-for-equity swap rather than derailing the initial deleveraging goal. It also circumvented a bid by MGM Properties in early 2018. (Ironically, MGM Properties was later bought by VICI in 2021 for $17.2 billion.) VICI's over-equitization strategy allowed the company to deleverage its balance sheet as it grew through the acquisition of prime real estate assets on the Las Vegas Strip and achieve 100% rent collection rates while the company's tenets struggled through Covid-19, but were reluctant to forfeit their Las Vegas locations by defaulting on rental fees. VICI also achieved a $30 billion market capitalization and an investment-grade debt rating within five years after emerging from bankruptcy. The company's current rating is BBB-, as reviewed by both Moody's and Fitch. The company also has maintained good control over debt levels. VICI currently has a healthy debt-to-equity ratio of 0.70 and a current ratio of 28.22.

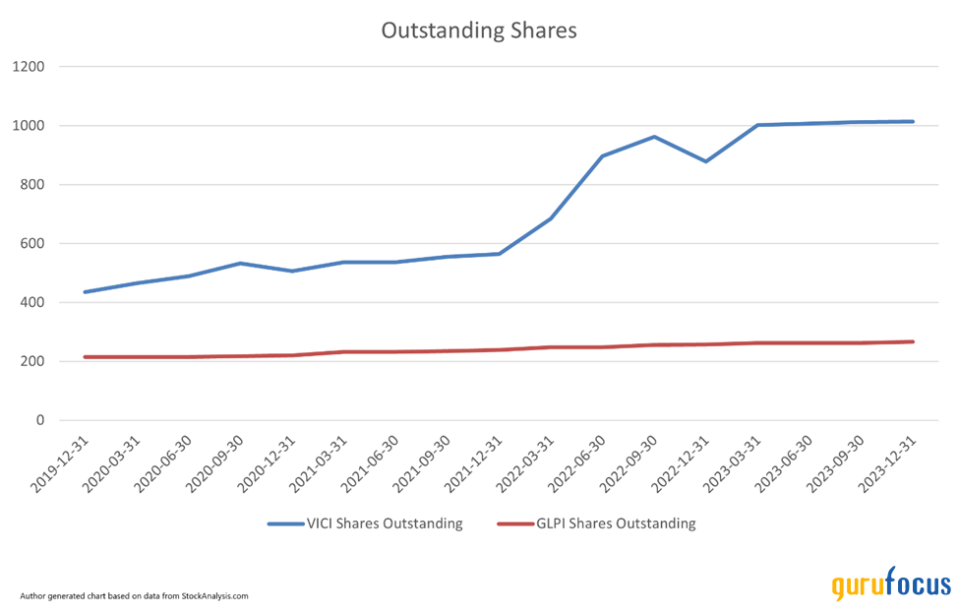

On the flip side, the strategy has also served to drag down shareholder yield. VICI's practice of issuing shares is reflected in the chart below. Its three-year buyback ratio is -24.80 and its shareholders' yield as of December 2023 is -18.77% versus Gaming and Leisure's three-year buyback ratio of -5.20 and shareholder yield of 2.18%.

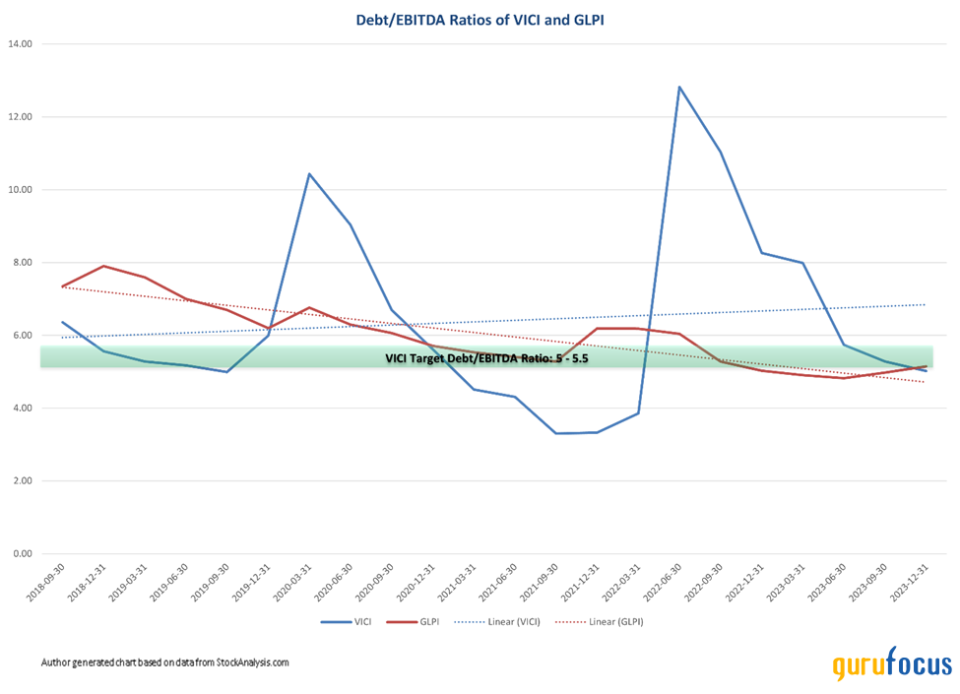

VICI has a long-term goal to keep its debt-to-Ebitda ratio between 5 and 5.50, which it is currently meeting; but this ratio has fluctuated from a low of 3 to as high as 12.82 in the last five years and is trending upward.

VICI's moat on the Las Vegas Strip

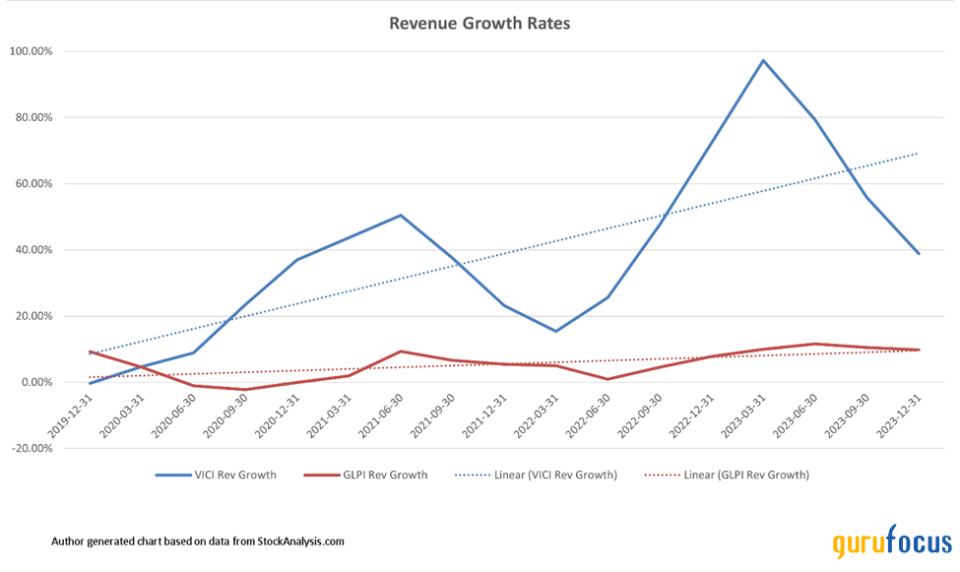

VICI's draw for investors over Gaming and Leisure Properties is demonstrated not only in terms of strong financial health, revenue growth and operating cash flow, but also in terms of its Las Vegas Strip property assets. The master lease for the Venetian, its largest tenant in terms of square footage, includes the Palazzo, Venetian Expo and Convention Center and the MSG Sphere. VICI also owns the Caesars Forum Convention Center behind the Linq. Overall, VICI owns approximately 660 acres of land covering 10 resorts on the strip. In addition to VICI's developed properties, it also owns 33 acres of undeveloped land on and near the strip that provides ample development and expansion opportunities.

Property Owner | Property | Tenant | Lease | Total Sq. Ft. (1,000s) |

VICI | The Venetian Resort Las Vegas | Venetian Las Vegas Tenant | The Venetian Resort Las Vegas Lease | 16,970 |

VICI | Mandalay Bay | MGM Resorts International | MGM Grand/Mandalay Bay Master Lease | 9,581 |

VICI | MGM Grand Las Vegas | MGM Resorts International | MGM Grand/Mandalay Bay Master Lease | 9,068 |

VICI | Caesars Palace Las Vegas | Caesars Entertainment | Caesars Las Vegas Master Lease | 8,579 |

VICI | Park MGM | MGM Resorts International | MGM Master Lease | 5,099 |

VICI | The Mirage | Hard Rock Entertainment | Mirage Lease | 4,795 |

VICI | Harrah's Las Vegas | Caesars Entertainment | Caesars Las Vegas Master Lease | 4,100 |

VICI | Luxor | MGM Resorts International | MGM Master Lease | 3,398 |

VICI | Excalibur | MGM Resorts International | MGM Master Lease | 2,860 |

VICI | New York - New York & The Park | MGM Resorts International | MGM Master Lease | 2,765 |

GLPI | Tropicana Las Vegas (Ballpark) | Bally's Corporation | Tropicana Las Vegas Lease | 0 |

BREIT | Cosmopolitan | MGM Resorts International | Cosmopolitan Net Lease | 6,902 |

O | Bellagio (95% Ownership) | Wynn Resorts | Bellagio Net Lease | 8,507 |

Wrap-up and further thoughts

VICI may be the strip's best-kept secret. The company's board of directors and shrewd management are credited with helping the company emerge from a challenging situation tied to the bankruptcy of a prominent Las Vegas casino operator to becoming a promising performer with historic growth rates. The challenge moving forward will be to continue the trek of strategic growth while maximizing shareholder value. VICI's current fundamentals are solid, but I would like to see a limit on the number of additional shares issued moving forward and focus on the development of current assets.

Please note that I am not a financial advisor, and this article is intended only for informative purposes and should not be construed as investment advice.

This article first appeared on GuruFocus.