Yahoo Finance

Yahoo Finance Can V.F Corp (VFC) Get Back on Track With Its Growth Endeavors?

V.F. Corp VFC has been witnessing a tough operating environment and continued supply-chain headwinds, including higher lead times and increased volatility on the distribution and logistics front. This led to a sluggish year-over-year performance in third-quarter fiscal 2022.

Adjusted earnings per share of $1.12 declined 17% year over year. On a constant-currency (cc) basis, adjusted earnings per share were down 10%. Net revenues of $3,531 million dipped 3% year over year due to weakness in the EMEA and APAC regions, partly offset by the solid performance in the outdoor brands, particularly The North Face. Revenues of the company’s big four brands were down 3%, while the rest of the portfolio decreased 2%.

The fiscal third-quarter adjusted gross margin decreased 140 bps to 54.9% due to higher promotions. Meanwhile, the adjusted operating margin contracted 280 bps to 14.9% due to a lower gross margin. SG&A expenses rose 5% to $1,421.6 million.

Moving on, the company’s China business continues to remain dismal. Notably, fiscal third-quarter APAC revenues decreased 7% on a reported basis (up 4% at cc), whereas revenues in Greater China fell 11% (down 1% at cc). Although its raw material suppliers across China are currently operational, it saw an eight-week lockdown in China in the first quarter of fiscal 2023. This led to logistics-related issues causing ongoing product delays. VFC is working with its suppliers to minimize disruptions. Currently, China has been witnessing sequential improvement as it reopens, but lower consumer spending remains concerning.

Consequently, the company expects fiscal 2023 constant dollar revenue growth of 3%, down from the earlier mention of 5-6%. Vans brand revenues for the fiscal year will now be down in the high-single digits compared with the prior mentioned mid-single digits. VFC forecasts gross margin to decline 200 bps year over year compared with the prior mentioned decline of 100-150 bps. The adjusted operating margin is envisioned to be 9.5%, down from the earlier mentioned 11%. V.F. Corp expects adjusted earnings per share of $2.05-$2.15 compared with the $2.40-$2.50 stated earlier.

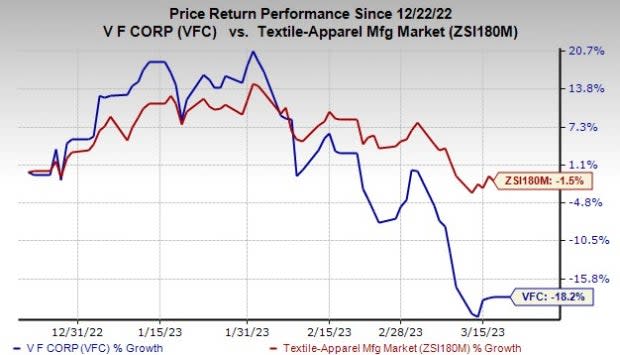

Image Source: Zacks Investment Research

We note that shares of VFC have lost 18.2% in the past three months compared with the industry’s decline of 1.5%.

Efforts to Counter Hurdles

That said, management is leaving no stone unturned to get back on track. It remains focused on the strategic review of its Global Packs business, consisting of the Kipling, Eastpak and JanSport brands, as well as the divestiture and leaseback of its Europe headquarters in Stabio, Switzerland. VFC is focused on lowering working capital and optimizing inventories.

Also, it has been accelerating its cost-saving efforts, which are likely to generate $225 million in fiscal 2024, on an annual basis, after the completion of its previously announced actions.

For fiscal 2024, revenues are anticipated to grow in the low-single-digit range on a constant-currency basis. Gross and operating margins are likely to expand. Operating income is expected to grow in double digits, whereas the operating cash flow is likely to grow faster than earnings.

Gains from the Supreme buyout remain a key growth driver for V.F. Corp. The company is benefitting from Supreme’s strong follower base in the younger generation, even when consumers are moving away from apparel to essential spending. The acquisition has accelerated its 2024 strategy. This strengthens the company’s long-standing partnership with Supreme. V.F. Corp collaborated with Supreme for its brands, such as The North Face, Vans and Timberland, on various occasions.

Management also unveiled its five-year growth plan for fiscal 2023-2027. The company expects revenue five-year compounded annual growth rate (CAGR) of mid- to high-single digits. The bottom line is predicted to grow, seeing a five-year CAGR of high single to low-double digits. The operating margin is envisioned to be 15% by fiscal 2027, driven by gross margin expansion and reduced SG&A. Management also noted that it would return roughly $7 billion via dividends and share repurchases by fiscal 2027. Free cash flow is forecast to be $5.5 billion.

Bottom Line

All said, we believe that the aforementioned initiatives will help offset supply-chain woes and other macroeconomic headwinds. Topping it, a Value Score of B and a long-term earnings growth rate of 3.2% raise optimism in the Zacks Rank #3 (Hold) stock.

Stocks to Consider

Some better-ranked companies are Ralph Lauren RL, Deckers Outdoor DECK and H&R Block HRB.

Ralph Lauren, a footwear and accessories dealer, has a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Ralph Lauren’s next-financial-year sales and EPS suggests growth of 5% and 12.8%, respectively, from the year-ago reported figures. RL has a trailing four-quarter earnings surprise of 23.6%, on average.

Deckers Outdoor currently carries a Zacks Rank #2 (Buy). The company has a trailing four-quarter earnings surprise of 31%, on average.

The Zacks Consensus Estimate for Deckers Outdoor’s current financial-year sales and earnings suggests growth of 12% and 13.5% from the year-ago period’s reported numbers, respectively.

H&R Block provides assisted income tax return preparation and do-it-yourself tax return preparation services. HRB currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for H&R Block’s current financial year’s EPS suggests growth of 9.4% from the year-ago reported figure. H&R Block has a trailing four-quarter earnings surprise of 10.7%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

V.F. Corporation (VFC) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

H&R Block, Inc. (HRB) : Free Stock Analysis Report