Yahoo Finance

Yahoo Finance Ulta Beauty: A Debt-Free, Growing Business With Upside Potential

Ulta Beauty Inc. (NASDAQ:ULTA) has been a disappointment for shareholders over the past three months. Its share price dropped from $567 in the middle of March to $376 in the middle of May, then rebounded to $395 at the time of writing. The three-month return was -27.70%.

However, looking from a broader timeline, Ulta Beauty has delivered nice gains for shareholders. Over the past 16 years, its share price has managed to grow by more than 2,800%, with a compounded annual gain of 23%. Let's take a closer look to determine whether Ulta Beauty is a good stock for long-term investors now.

Steady growth in a challenging business environment

For the first quarter, Ulta Beauty reported steady growth in a tough market environment, with net sales up 3.50% to $2.72 billion and comparable sales up 1.60%. The company outperformed the Wall Street's forecasts of $2.72 billion. It also recored strong earnings of $6.47 per share versus estimates of $6.25. The operating profit margin reached 14.70% of sales. Notably, fragrance and skincare saw double-digit and mid-digit growth and makeup sales declined in the mid-single-digit range.

The current industry environment and increased competition led Ulta Beauty to revise its full-year forecast. The company currently expects fiscal 2024 net sales of $11.50 billion to $11.60 billion, down from $11.70 billion to $11.80 billion previously. The comp sales growth would stay in the range of 2% to 3%. Diluted earnings per share are expected to be between $25.20 and $26, versus $26.20 to $27 from earlier projections. These adjustments reflect anticipated continued pressures in the beauty category in addition to increased competition from rivals like Sephora and Amazon's (NASDAQ:AMZN) push into high-quality beauty brands.

CEO Dave Kimbell attributed the forecast adjustment to the dynamics in the first quarter and cited several strategic initiatives designed to solidify Ulta Beauty's market position. He said:

We are confident in our model and our ability to gain share and drive significant sustainable value over the long-term. The actions we have taken and investments we have made over the past few years have fortified our operating foundation and we are a stronger, more profitable company today than we were just a few years ago.

Ulta Beauty is implementing several key initiatives, including enhancing product range and digital experience, accelerating social relevance, leveraging the loyalty program and evolving promotional strategies. The company is also working to maintain its gross margin, which dropped to 39.20% in the first quarter due to lower merchandise margins and higher inventory shrink. It is launching new marketing technology later this year that will allow for more personalization and top-line growth.

Plans to continue repurchasing shares

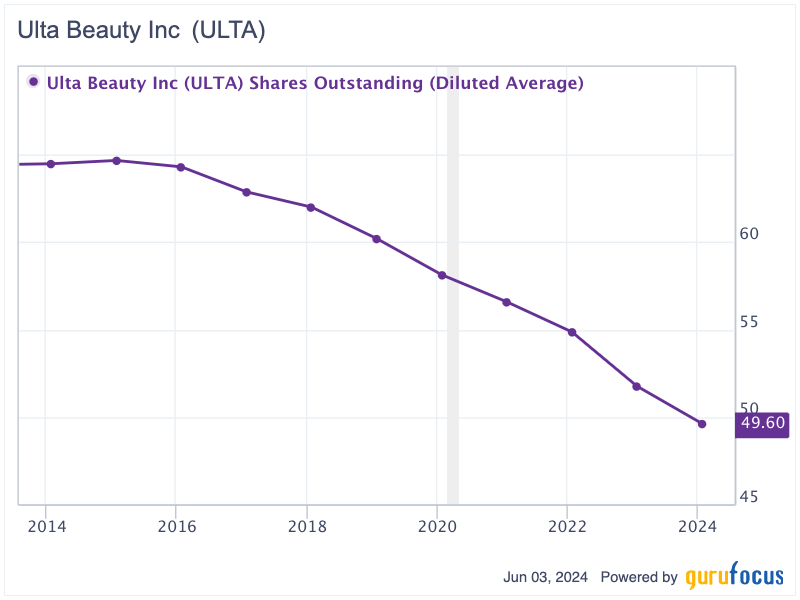

Ulta Beauty has a history of repurchasing shares on the open market, reducing its share count over the years. The company has spent over $5.86 billion on stock buybacks since 2013. As a result, total shares outstanding dropped by over 23% from 64.46 million in 2013 to 49.6 million in 2023. As of the first quarter, the share count stood at around 48.38 million.

Further, the company plans to repurchase $1 billion worth of stock within the year. If $1 billion is used to buy back shares at around $400 per share, Ulta Beauty could buy back up to 2.50 million additional shares, yielding more than 5.20% for its shareholders.

Debt-free balance sheet

What I like about Ulta Beauty is the debt-free balance sheet. As of May 2024, it had $2.30 billion in total stockholders' equity. The cash on hand came in at nearly $525 million. While the company has no interest-bearing debt, it does have operating lease liabilities. The total operating lease liabilities, both short and long term, were $1.89 billion. Although the total amount of operating leases seems to be a lot, the lease payment spread out over many years. The lease payment which the company has to pay within one year are only around $351,500. The total lease payments in the next three to five years amount to nearly $545,900.

Source: Ulta Beauty's 10-K filing

As its operating cash flow has stayed in the range of $810.3 million to $1.48 billion in the past five years, Ulta Beauty could settle operating lease payment quite easily.

Potential upside

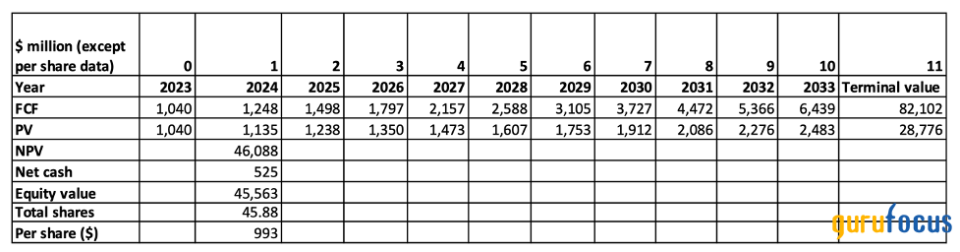

Ulta Beauty has expanded its free cash flow from $101 million in 2013 to $1.04 billion in 2023, posting compounded annual growth of 26.20%. Since the company has been generating growing free cash flow quite consistently over the past decade, we can use discounted free cash flow method to value the business.

Assuming the retailer's free cash flow growth would reduce a bit to 20% per year in the next 10 years, then the terminal growth would be 2% afterwards. With a 10% discount rate, the company's enterprise value would be around $46 billion. Adjusting the current net cash of $525 million, its market capitalization should be worth $45.56 billion. If Ulta Beauty commits all $1 billion in share repurchase within this year, the total share count would be reduced to 45.88 million. This translates to an intrinsic value per share of $993, nearly 150% upside from the current trading price.

Source: Author's calculation

Key takeaway

Ulta Beauty remains a resilient long-term investment despite recent volatility and a downward adjustment of its fiscal outlook. Its strategic initiatives, a robust share repurchase program and debt-free balance sheet underscore its sound fundamentals and focus on shareholder value. Our recent DCF valuation shows the stock is quite cheap with a potential 150% upside for investors. Therefore, Ulta Beauty fits well in portfolios of long-term investors who are looking for a growth stock with a solid financial foundation.

This article first appeared on GuruFocus.