Yahoo Finance

Yahoo Finance

What Are Singapore Treasury Bills and Are They a Good Investment?

We all know by now that it’s not the best idea to leave our excess cash in a bank savings account. After all, with some savings accounts giving as low as 0.05% per annum interest, the meagre returns are insufficient in helping us beat inflation in the long run.

Meanwhile, high-yield savings accounts such as multiplier accounts with higher interest rates may make you jump through more hoops to unlock higher interest rates.

Maybe you’re not keen on parking your cash in the Singapore Savings Bond (SSB) for 10 years or Singapore Government Securities (SGS) bonds for the full tenor (up to 50 years). Maybe you’re seeking an alternative to fixed deposits. Or maybe you are looking for a place to stash your cash until the looming global recession tides over.

Whatever the reason, if you’re hoping to reap a higher return on your excess cash, T-bills might just be your answer. In this guide, we will dive into the ins and outs of T-bills so you can decide if they’re a good addition to your portfolio.

Table of Contents

How Do T-Bills Work?

T-bills are short-term Singapore Government Securities (SGS) issued at a discount from their face value, and they pay a fixed interest rate. Their maturity periods are as short as six months and a year, with six months being more common.

T-bills are issued by the government primarily to develop the local debt markets. The issuance of these bonds serves three main reasons.

The first is to build a liquid SGS market to provide a robust government yield curve to serve as a benchmark for the pricing of private debt securities.

Second, is to foster the growth of an active secondary market for both cash transactions and derivatives to enable efficient risk management.

And the third reason is to get both domestic and foreign issuers and investors to participate in the Singapore bond market.

T-bills have an AAA credit rating with the backing of the Singapore Government, as well as short maturity periods of six months to one year. You can invest with cash, CPF or SRS funds without an overall limit, and — unlike with SGS bonds, which pay investors in coupons — receive the full value upon maturity.

So for instance, an investor who buys a six-month T-bill worth S$10,000 with a yield of 3% p.a. need only pay S$9,850 upfront. At the end of the tenor, he will receive the full S$10,000 and therefore earn S$150.

Are T-Bills a Good Investment?

Singapore is one of just 11 countries in the world — including Finland and Switzerland — that have the AAA credit rating. And since T-bills are backed by the Singapore Government, they are considered a very low-risk investment (note: there are still some risks).

If you’re a conservative investor or looking for lower-risk products to diversify your portfolio, particularly in an austere macroeconomic environment, T-bills are one of the safest products in the market to invest in. They are also a short-term option that won’t lock up your funds for too long, and you can be guaranteed a fixed-interest payment at maturity.

However, investing in T-bills would likely not generate sufficient returns to combat inflation in the long run. Therefore, they should only form a part of your investment portfolio and not the entirety of it.

On top of that, since the interest rates are determined based on a uniform-price auction, the interest rate that you will receive is not certain. Selling your T-bills before they mature may also result in losses as bond prices may fluctuate based on the market interest rate.

That said, if you’re looking to do some short-term investment, T-bills are a safe way to park some spare cash, especially now with interest rates going up and even beating fixed deposits rates offered by banks.

(For longer term low-risk investments — i.e. 5 to 10 years — you might want to consider investing in SSBs or SGS bonds instead.)

Read More: The Most Popular Types of Investment in Singapore (And How to Get the Most Out of Them)

Pros and Cons of Investing in T-Bills

Pros | Cons |

|---|---|

Low minimum investment requirement (S$1,000) | Relatively low rate of returns |

Can be bought and sold easily in the secondary market | No coupon interest payments in period leading up to maturity |

For individuals, interest income earned on SGS is tax exempt | Might hinder cash flow for those requiring steady monthly income |

Zero default risk | Potential interest rate risk |

Good for diversifying portfolio/mitigating risks | Have to bid through an auction process |

T-Bills Jan 2024 Rates

These are the closing levels as of 2 Jan 2024.

MAS Website: Treasury Bill Rates January 2024

T-Bills vs SSB vs SGS Bonds

Feature | T-bills | Savings Bonds | SGS bonds |

|---|---|---|---|

Available tenor | 6 months or 1 year | Up to 10 years | 2, 5, 10, 15, 20, 30 or 50 years |

Method of sale | Uniform price auction — competitive or non-competitive bids | Quantity ceiling format | Auction: Uniform price auction — competitive or non-competitive bids. Syndication: Public Offer — fixed price and yield as determined in the Placement Tranche. (MAS will seek to allocate the bonds in the Public Offer to as many individuals as possible, taking into account the distribution of applications) |

Frequency of issuance | Fortnightly or quarterly, according to the issuance calendar | Monthly, for at least 5 years | Auction: Monthly, according to the issuance calendar. Syndication: From time to time, according to indicative timeframe as announced by MAS |

Minimum investment amount | S$1,000, and in multiples of S$1,000 | S$500, and in multiples of S$500 | S$1,000, and in multiples of S$1,000 |

Maximum investment amount | None; up to the allotment limit for auctions | S$200,000 overall | Auction: up to allotment limit for auctions. Syndication: None |

Buy using SRS and CPF funds? | Yes | SRS: Yes; CPF: No | Auction: Yes; Syndication: No |

Type of interest rate payment | No coupon; issued and traded at a discount to the face (par) value | Fixed coupon, steps up each year | Fixed coupon |

How often interest is paid | At maturity | Every 6 months, starting from the month of issue | Every 6 months, starting from the month of issue |

Secondary market trading | At DBS, OCBC or UOB main branches | No | At DBS, OCBC or UOB main branches; on SGX through brokers |

Transferable | Yes | No | Yes |

Maturity and redemption | No early redemption. Investors receive the face (par) value at maturity (i.e. price of S$100). | Can be redeemed in any month, with no penalty. Investors receive the face (par) value plus accrued interest upon redemption. | No early redemption. Investors receive the face (par) value at maturity (i.e. price of S$100). |

Read Also: Fixed Deposit Vs Singapore Savings Bonds: Which Should You Go For?

Step-By-Step Guide to Buying and Selling T-Bills

You can buy the T-bills using cash, CPF Investment Scheme (CPFIS) or Supplementary Retirement Scheme (SRS) funds. Here’s how they work.

Using Cash

To buy T-bills using cash, you will need a bank account with any one of the three local banks (DBS/POSB, UOB, or OCBC), as well as an individual Central Depository (CDP) account. Direct crediting services must be activated for your principal payments and coupon to be credited directly to your bank account.

Once you have these in place, you can apply for T-bills via the local banks’ ATMs and internet banking portals.

You will see the transaction reflected in your CDP statement if it went through successfully.

Using SRS Funds

To buy T-bills using your SRS funds, you will need an SRS account with any one of the three SRS operators (DBS/POSB, UOB, and OCBC). You can apply for T-bills through your SRS operator’s internet banking portal.

You will see the transaction reflected in the statement issued by your SRS operator if it went through successfully.

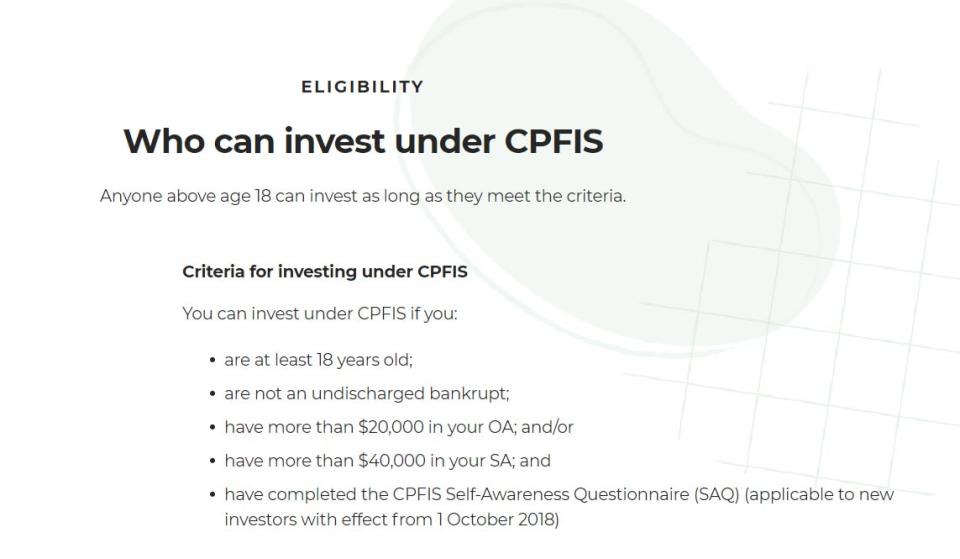

Using CPFIS Funds

To buy T-bills using CPFIS (OA) funds, you would need a CPF Investment Account with any one of the three CPFIS agent banks (DBS/POSB, UOB, or OCBC). However, unlike the above two options, you would not be able to buy T-bills via internet banking. Instead, you would need to submit an application in person at any of the CPFIS bond dealers’ branches.

You will see the transaction reflected in your CPFIS statement issued by your agent bank if it went through successfully.

Read More: A Guide to Understanding the CPF

How to Buy New T-Bills

When you apply for new T-bills, you will come across the option of a competitive and non-competitive bid.

A competitive bid requires you to specify your yield, i.e. the price you are willing to pay for the T-bills. A lower yield means a more competitive bid. Your funds will only be invested if the cut-off yield goes above your specified yield. This type of bid is typically for institutional investors or savvier investors.

A non-competitive bid doesn’t require you to specify your yield. Instead, you specify the amount that you want to invest and you will be allotted the T-bills at a uniform yield. This is the better option for average Joe investors, who might not know how to put in a competitive bid.

Non-competitive bids are allotted first (up to 40% of the total issuance amount) — before the balance is allotted to competitive ones from the lowest to highest yields — which means you have a higher chance of securing an allotment with a non-competitive bid. If the number of non-competitive bids exceeds 40%, the T-bills will be prorated and allocated to you.

Keep in mind that bidding ends one day before the Auction Date. The Auction Date for the next tranche of six-month T-bills is 18 Jan 2024. For the full issuance calendar, you can refer to the MAS website.

How to Sell T-Bills

Investors are not allowed to redeem their T-bills early, but you may consider selling them on the secondary market through the three main aforementioned dealer banks.

However, the price of the T-bill may rise or fall before maturity. The trading volume for T-bills is also low, which makes them pretty illiquid for the duration of the tenor. Therefore, if you sell them below par value, you could stand to lose some capital.

Kick-Start Your Investment Journey

Now that we have a fuller understanding of T-bills, you might want to continue your lookout for more investment instruments and alternatives. Visit our investments page for tips and beginner-friendly guides to kick-start your investment journey.

Read Also:

The article [shortcode_validation_fail] [link] url: www.valuechampion.sg/treasury-t-bills-singapore-investment-dec-2022 should be a valid relative or absolute URL. Value was invalid and will not be shown to users. originally appeared on ValueChampion.

ValueChampion helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValueChampion:

What Are Singapore Treasury Bills and How Do They Work

The Most Popular Types of Investment in Singapore (And How to Get the Most Out of Them)