Yahoo Finance

Yahoo Finance Silverlake Axis Ltd - Why did it ignore investor concerns over transactions with related parties for so long?

7/9/2015 - Singapore’s stock market seems to be an attractive destination for short sellers with the recent attack on Silverlake Axis Ltd (SAL), a Malaysia-based software company.

A 42-page report titled "The Unbelievable Financial Alchemy of Silverlake Axis", was released on August 20, authored by an anonymous author going by the name "razor99".

The report highlighted that Silverlake Axis had huge related-party transactions with private companies that are linked to its executive chairman and founder, Goh Peng Ooi.

It added that there were numerous red flags and ample evidence suggesting that Goh had used these related-party transactions to inflate Silverlake’s reported results.

It said SAL would prove to be an investor’s worst nightmare, like fraudulent IT services companies such as China-based Longtop Financial and India's Satyam Computer Services.

As a result, it said it believes that Silvelake Axis is worth S$0.29 based on a peer average price-to-sales ratio of 5.3 times and SAL’s non-related party revenue, compared to its current price of S$0.57.

It believed this target price was very generous and was based on conservative assumptions, and that it wouldn’t rule out the possibility that the stock is ultimately worth zero.

It does not "recommend investors purchase the stock at any price because with a deceptive and manipulative controlling shareholder like Goh, we doubt minority shareholders will accrue any value over time."

It also casts doubt that SAL would have much value to an acquirer because of the ongoing related party transactions and key man risk.

Silverlake asked for an immediate halt on trading of its shares after the stock fell as much as 27% in intraday trade on August 21.

Soon after the Group released its FY15 results on August 24, it also published its clarification about the allegations.

It said that the "adverse allegations contained in the Report are clearly baseless and without merit".

It is seeking "legal advice and wishes to highlight that it views this matter most seriously and will be strenuously investigating the source of the Report with a view to taking all such action as may be necessary to fully protect and defend its interests."

The statement went on to say that the Board believed that its results speak for themselves and it also confirmed that it had no undisclosed contingent liabilities.

To provide additional comfort to the shareholders, it would engage Deloitte Singapore to undertake an independent review of the allegations.

According to StarBiz, Goh said everything is in order.

The company has been growing since the assets were injected, he said.

He said the board of directors had control over the running of the company and his passion and interest were skewed towards research.

"My character is more academic and I don’t care what others think about me. But I do take people’s criticism as an education process," he said.

"It’s my responsibility as a supplier and majority shareholder to develop software. The listing side of the business is left to the board."

Maybank Research has cut FY16-FY17 licensing and project service sales from between RM250 mln and RM290 mln to between RM220 mln and RM235 mln due to a lack of new contracts.

As a result, it cut its forward EPS target by 15%-18%.

It also updated its MYR/SGD exchange rate assumptions to 3.00 from 2.60, following recent weakness in the Malaysian Ringgit.

Silverlake Axis' costs are mostly denominated in Malaysian Ringgit (MYR) but it collects part of its revenue in Singapore Dollars and US Dollars.

This implies net benefits from a weaker MYR.

Maybank points out the share price is down a sharp 40% in the past three months on concerns over interested-person transactions (IPT) between Silverlake Axis and private entities under its chairman.

Hence, even though its new discounted cash flow (DCF) valuation suggests a fair value of S$0.87, down from S$1.15 after it cut its EPS target, it doubts that there will be a re-rating before any improved disclosure.

As a result, it maintained a HOLD rating with target price lowered from S$1.15 to S$0.61.

The company just announced earnings for FY15:

Revenue: +3% to RM516 mln

Profit: +14% to RM282.7 mln

Cash flow from operations: RM302.2 mln vs RM277.4 mln

Dividend (Q4): 2 US cents per share vs 2 US cents per share

Dividend (FY15): 8 US cents per share vs 8 US cents per share

The increase in the group's revenue was due to higher contribution from maintenance and enhancement services and insurance processing.

However, it was partially offset by a decrease in revenue contribution from the sale of software and hardware products, credit and cards processing, software project services and software licensing.

Profit grew mainly from its sale of stake in Global Infotech during its recent IPO.

Investor Central. Asian insights for global investors. We ask the tough questions of Asian companies which global investors need answers to.

1. Why did it ignore investor concern over transactions with related parties for so long?

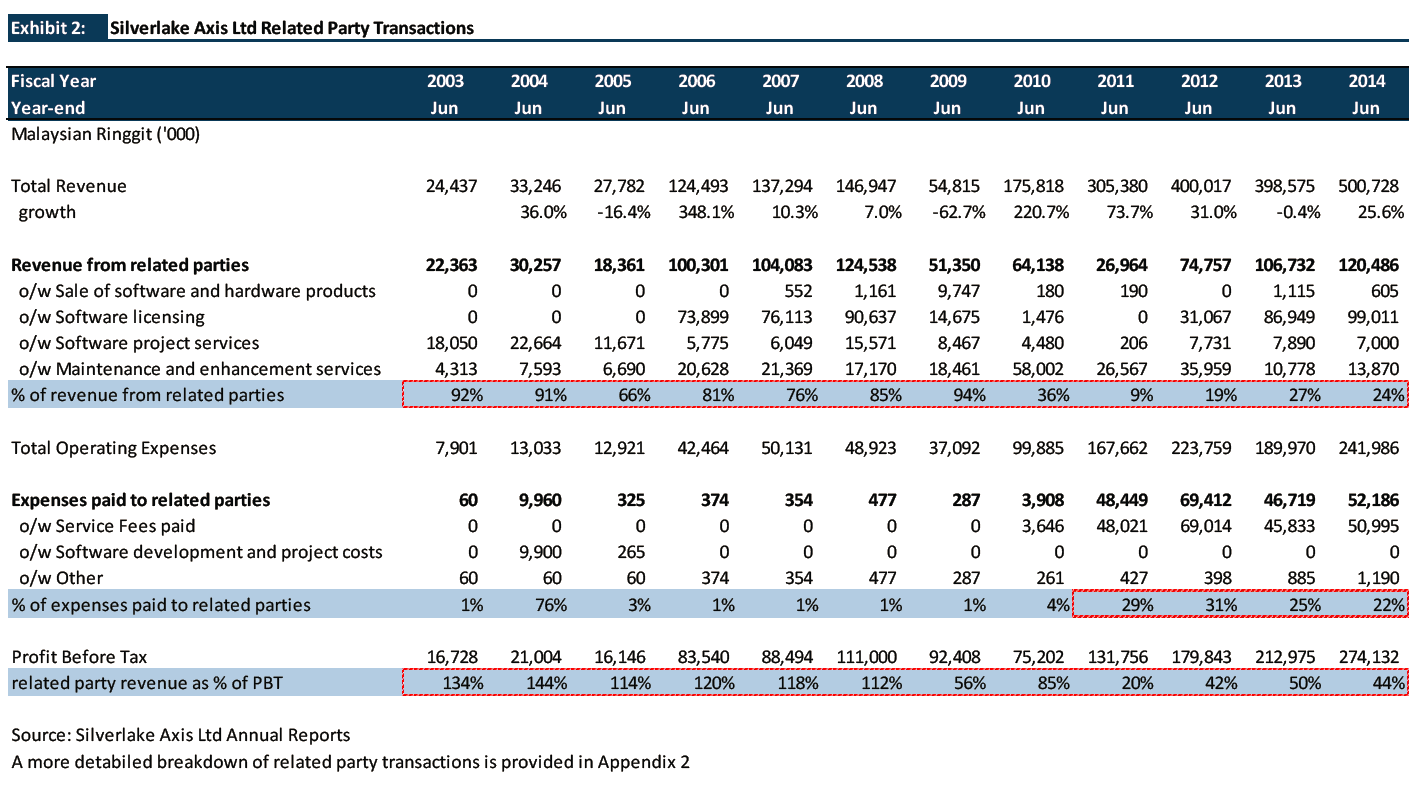

According to the short seller report, Silverlake Axis (SAL) has relied extensively on related party transactions since its IPO in 2003.

Between FY03-FY09, the vast majority of the Group's revenue was generated from related party companies in the Silverlake Group controlled by Goh, it said.

While the percent of revenue from related parties has declined since 2010 following the acquisition of Silverlake Systems Sdn Bhd (SSB), related parties still account for nearly one quarter of group revenue and expenses, it said.

Revenue from related parties contributed 92% of total revenue in 2003, 94% in 2009, 36% in 2010 and 24% in 2014.

As a percentage of profit before tax, related parties revenue was 134%, 56%, 85% and 44%, respectively, during the same period.

It believes that Goh’s stated rationale for not having all Silverlake Group entities consolidated into SAL is flimsy at best.

It is not a practice used by peers in the industry, the report said.

It is also very "telling that even after the Silverlake Adaptive Applications & Continuous Improvement Services Ltd (SAACIS) and SSB acquisitions supposedly brought nearly all of the Silverlake Group business into SAL, significant related party transactions have continued."

In fact the absolute magnitude of total related party transactions reached a new high in FY2014, the report said.

Maybank Research also says that Silverlake Axis' interested party transactions (IPTs) have been an area of market concern for some time.

Even though such transactions are reviewed by its audit committee, and their mandates are renewed at its annual general meeting, the market remains wary of any artificial inflation of profits.

As the Group derives about one-quarter of its revenue from the private entities under its chairman and 66% major shareholder, Mr Goh, and passes about one-fifth of its core operating costs to these entities, the analyst believes IPTs will remain a stock overhang, as long as IPT disclosure is not improved.

2. Will it improve its related party transactions disclosures?

From FY03-FY07, SAL disclosed a more detailed record of SAL’s transactions with each Silverlake entity.

However from FY08 onwards, SAL has only disclosed aggregate related party transaction amounts, with no related party entity breakdown.

This more limited disclosure has significantly reduced transparency, making it nearly impossible to track the related parties with whom SAL transacts, the short seller report said.

(Read the full story to get all 7 questions)

We have invited the company to an on-camera interview, and/or to reply to our questions in writing.

At the time of publication we have not received a reply (which is why you are seeing this message).

We will update this report if we do.

Legal notice

While our purpose is to ask the questions which the man on the street would ask, and to help the everyday investor make informed investments, please note that:

Our reports and presentations ('our contents') are not investment advice nor should they be construed as investment advice or any recommendation of any kind; nor meant to cast allegations or insinuations of any kind against any individuals or entities. Before acting on the material in our contents, you should either seek independent advice tailored to your particular circumstances and intentions or rely on your own judgement.

Our reports and presentations express our observations, opinions and theoretical analysis based on the facts that we have gathered or have been provided to us. While we endeavour to ensure that our contents are accurate and are presented in good faith, we cannot and do not warrant the accuracy, adequacy or completeness of the material or that the material is suitable for its intended use; and we disclaim any such warranties express or implied that may be presumed by any party; neither do we take responsibility for the views of companies or other stakeholders or observers or sources quoted or hyperlinked in our contents. While every precaution has been taken in the preparation of our contents, we (and our principals) shall not be liable for any losses or damage or inconveniences due allegedly to errors or omissions in any facts or due allegedly to reliance on our contents in any way whatsoever; nor for any damage to any computer hardware, date information or materials allegedly caused by our contents.

All expressions of opinion and observations in our contents are subject to change without notice and we do not undertake a duty to update and supplement our contents or the information contained herein in the event we obtain any further or more complete information.

©2015 Investor Central® - a service of Hong Bao Media