Yahoo Finance

Yahoo Finance Revenue Diversification Aids Ally Financial (ALLY), Costs Ail

Ally Financial Inc.’s ALLY efforts to diversify revenues, along with its inorganic growth initiatives, are expected to keep supporting the top line. Given its robust capital and liquidity positions, the company will likely be able to sustain efficient capital distributions in the future.

Analysts are optimistic regarding the company’s earnings growth potential. The Zacks Consensus Estimate for ALLY’s 2024 earnings has been revised 1% upward over the past 60 days.

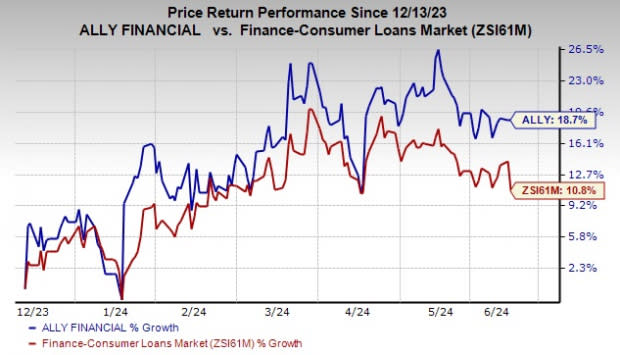

Over the past six months, shares of Ally Financial have gained 18.7% compared with the industry’s 10.8% growth.

Image Source: Zacks Investment Research

However, elevated expenses will likely hurt the company’s bottom line. Poor credit quality and higher funding costs are other concerns. Thus, the company currently carries a Zacks Rank #3 (Hold).

Looking at its fundamentals, while ALLY’s net financing revenues (a key source of revenues) declined in the first quarter of 2024, it witnessed a compound annual growth rate (CAGR) of 7.2% over the last five years (2018-2023). Given the strong origination volumes and retail loan growth, the company is expected to continue to witness a rise in the metric in the quarters ahead. While we project net financing revenues to decline in 2024, the metric is expected to rise 10.4% in 2025 and 15.5% in 2026.

As part of its strategy to diversify into banking products, Ally Financial has forayed into the mortgage business, which has been supporting its earnings. We project the Mortgage Finance segment’s revenues to witness a CAGR of 8.2% by 2026.

Also, the company has been making efforts to enhance digital offerings and introduce new products to further boost profitability. In September 2023, it launched Ally.ai, which is a proprietary, cloud-based artificial intelligence platform that will allow the company to integrate any AI capability into business operations at an enterprise scale.

Acquisitions of Fair Square Financial (a credit card provider), TradeKing and Health Credit Services (a point-of-sale payment provider) are expected to help the company improve its product offerings.

As part of its initiative to invest resources in growing scale businesses and strengthen relationships with dealer customers, ALLY sold its point-of-sale financing business — Ally Lending — to Synchrony, which is expected to be accretive to earnings in 2024.

However, over the last five years (ended 2023), ALLY’s expenses witnessed a CAGR of 9.6%, with the uptrend continuing in the first quarter of 2024. The rise was mainly due to higher compensation and benefit costs. With the company launching products, seeking opportunistic buyouts and expanding into newer areas of operations, expenses are expected to remain elevated. We expect total non-interest expenses to increase 0.8%, 2.4% and 1.6% in 2024, 2025 and 2026, respectively.

Poor asset quality is another headwind for Ally Financial. The trend for the company’s provision for loan losses has been volatile (increasing in 2020, falling in 2021, and then rising in 2022, 2023 and the first quarter of 2024). Given the rise in demand for consumer loans and the tough operating backdrop, provisions are expected to increase in the upcoming quarters. We project provisions to increase 4.1% in 2024 and 2.3% in 2025.

While the current high interest rate environment might have a positive effect on Ally Financial’s NIM to some extent, higher funding costs will likely significantly weigh on it. Its NIM (reported) was 2.67% in 2019, 2.65% in 2020, 3.54% in 2021 and 3.85% in 2022. Then, despite higher rates, NIM declined in 2023 and the first quarter of 2024. NIM pressure is not expected to be completely alleviated in the near term because of higher funding costs.

Stocks Worth a Look

A couple of better-ranked stocks from the same space are World Acceptance Corporation WRLD and EZCORP, Inc. EZPW, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for WRLD’s current fiscal-year earnings has moved 3.6% higher over the past 60 days. Its share price has declined 7.3% in the past six months.

EZPW’s earnings estimates for fiscal 2024 have been revised 5.7% upward over the past 60 days. In the past six months, EZPW’s shares have rallied 14.6%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

World Acceptance Corporation (WRLD) : Free Stock Analysis Report

EZCORP, Inc. (EZPW) : Free Stock Analysis Report

Ally Financial Inc. (ALLY) : Free Stock Analysis Report