Yahoo Finance

Yahoo Finance Oversea-Chinese Banking (SGX:O39) Is Increasing Its Dividend To SGD0.42

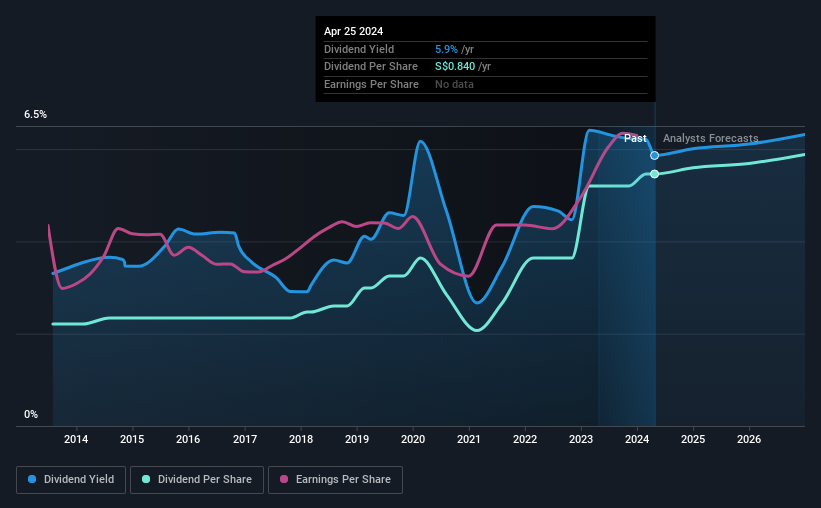

Oversea-Chinese Banking Corporation Limited's (SGX:O39) dividend will be increasing from last year's payment of the same period to SGD0.42 on 21st of May. This takes the dividend yield to 5.9%, which shareholders will be pleased with.

See our latest analysis for Oversea-Chinese Banking

Oversea-Chinese Banking's Dividend Forecasted To Be Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much.

Having distributed dividends for at least 10 years, Oversea-Chinese Banking has a long history of paying out a part of its earnings to shareholders. Based on Oversea-Chinese Banking's last earnings report, the payout ratio is at a decent 53%, meaning that the company is able to pay out its dividend with a bit of room to spare.

The next 3 years are set to see EPS grow by 6.7%. The future payout ratio could be 55% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The annual payment during the last 10 years was SGD0.34 in 2014, and the most recent fiscal year payment was SGD0.84. This means that it has been growing its distributions at 9.5% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

The Dividend Has Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Oversea-Chinese Banking has seen EPS rising for the last five years, at 8.0% per annum. The company is paying a reasonable amount of earnings to shareholders, and is growing earnings at a decent rate so we think it could be a decent dividend stock.

In Summary

Overall, this is a reasonable dividend, and it being raised is an added bonus. The payout ratio looks good, but unfortunately the company's dividend track record isn't stellar. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for Oversea-Chinese Banking that investors should take into consideration. Is Oversea-Chinese Banking not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.