Yahoo Finance

Yahoo Finance The over-70s who mortgage their homes to pay for care

Like many pensioners, Celia Smith faced an agonising choice as she began to realise she would need long-term care. The 73-year-old was diagnosed with multiple sclerosis 25 years ago but didn't need care until a decade later when she fell down the stairs, damaging her spine.

Faced with spiralling care costs, which are now rising at twice the rate of inflation, Mrs Smith had a heartbreaking choice to make: should she sell the family home to pay for the care she required?

She had a modest pension that would just cover the £99-a-week cost of having carers come three times a day. But she lacked the money to pay for necessary home improvements and for supporting her children. Her only significant asset was the family home in south London, which was bought in 1975 for £2,500 but had risen in value to £750,000.

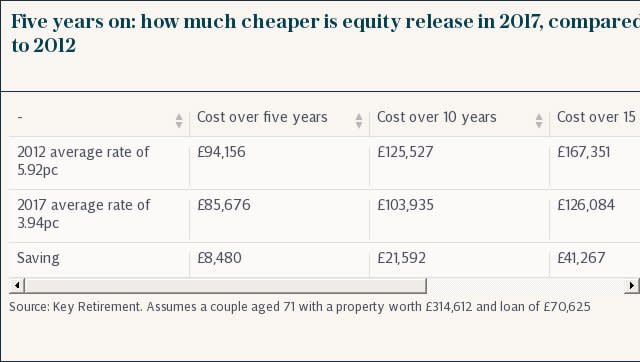

Rather than sell the home, she decided to borrow against it, using a special "lifetime mortgage" for those in later life. Lifetime mortgages, also known as equity release plans, are available only to those over 55 and are not repayable until the borrower dies.

"I've been here for 30 years and I didn't want to move out just to raise a bit of money," she said.

She borrowed £30,000 at an interest rate of 3.99pc, fixed for the life of the loan. No repayments are made, so the interest rolls up. Although compounding interest in this way can cause the outstanding loan to spiral if the borrower lives for a long time, a clause in the contract stipulates that it can never exceed the value of the home.

Mrs Smith can also borrow more money under the agreement if needed. She said: "Having the equity means I can draw on it if my children need any money and I think it's something necessary for them to have. They understand it's a loan and they need to pay it back, but they won't need to until after my death."

This means they will be able to use the remaining value of the family home to clear the debt.

The lifetime mortgage was provided by More2Life and arranged by a broker, Key Retirement.

The scale of the care funding crisis

Care funding is becoming an ever greater drain on Britain's finances.

The latest figures, from Prestige Nursing + Care, show that the average annual cost of a stay in a care home now exceeds £80,000 and is rising. The annual shortfall between pensioners' average income and the cost of care has risen by more than £5,000 since 2012 – from £14,196 to £19,382.

Jonathan Bruce from Prestige described the figures as "staggering" and called on the Government to address the growing problem. Many expected action in the Budget, but no major announcements were forthcoming.

Borrow against your biggest asset: the family home

Lifetime mortgages allow older homeowners to draw on the value of their home by borrowing against it. While the plans usually come with much higher interest rates than regular mortgages, there are usually no repayments due until the borrower dies or sells the house – the interest simply rolling up.

Nigel Waterson, the chairman of the Equity Release Council, said care homes were often assumed to be the only option for those no longer able to live independently but that a lifetime mortgage was often a viable alternative.

“Equity release provides a way for homeowners to access what is often their largest asset and continue living at home, even as their care needs change,” he added. “Many use the money to fund home care, while others might use it to fund home improvements that make the living environment easier.”

Pete Dowds of Elder, a Live-in care specialist, said borrowing in this way was a powerful but underused tool for those who needed care. “Equity release is being used a lot for holidays and renovations but it’s not being widely used for care," he said.

Elder provides live-in carers for a cost of between £695 and £750 a week. The average cost of residential care with nursing in Britain is now £845 a week while residential care alone costs £605, according to industry analysts LaingBuisson.

There are hundreds of providers of domiciliary care in Britain.

Analysis of lifetime mortgages on Money.co.uk, the price comparison service, shows that Hodge Lifetime currently has the lowest annual interest rate at 3.53pc. OneFamily has a range of offers from 3.56pc to 3.76pc, while Legal & General Home Finance's best lifetime mortgage has an annual rate of 3.86pc.

Reader service: See how much equity you could unlock with The Telegraph's Equity Release Calculator