Yahoo Finance

Yahoo Finance Home Loans in Singapore – The Complete Guide to Property Loans

Buying a home in Singapore is a huge financial commitment that almost everyone goes through at some point in their lives. Whether you’re a newly married couple or single, whether you’re buying an HDB flat or a private property, the time will come when you need to get a home loan.

What property you are planning on purchasing and how much you intend on borrowing are factors that go into deciding which property loan is best for you in Singapore.

Before you take a leap into the unknown, here’s what you need to know about home loans in Singapore.

Contents:

Types of home loans in Singapore

There are two options when it comes to home loans in Singapore. There is the HDB Concessionary Loan (better known as the HDB Loan), and loans from financial institutions (better known as bank loans).

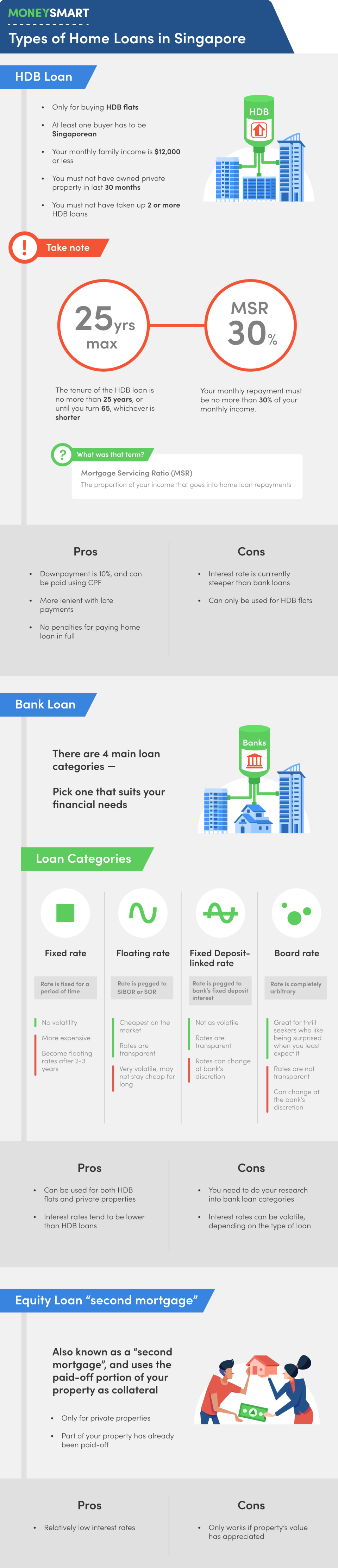

HDB Loan

The HDB Concessionary Loan is only for buying HDB flats (obviously) and therefore at least one buyer has to be Singaporean. The HDB loan is ideal for home buyers who are looking for a stable interest rate. It is also good for home buyers who might not have much cash on hand, such as young newlyweds.

This is because HDB loans require a smaller downpayment of 10% of the purchase price, compared to a bank loans, which require 20% of the purchase price as a downpayment. What’s more, the 10% of the purchase price can be paid via your CPF Ordinary Account so you don’t need to have a large amount of cash on hand.

There are a couple of other advantages of taking up an HDB Loan, including being more lenient with late repayments and has no penalties for paying of your home loan in full, unlike a bank loan.

However, the main consideration has to be the interest rate. The HDB Loan interest rate is always pegged at 0.1% more than the CPF Ordinary Account interest rate. Currently it is 2.6% and it has remained at this rate for almost two decades. At this time, however, it is considered steep compared to bank loans.

To be eligible for an HDB loan, you need to have a family monthly income of $12,000 or less, must not have owned any private property in the last 30 months, or taken up 2 or more housing loans from HDB.

The amount you can borrow from a HDB loan is limited by a handful of factors. The tenure of the HDB loan is no more than 25 years, or till you turn 65, whichever is shorter. Your monthly repayment must be no more than 30% of your monthly income. This is known as the Mortgage Servicing Ratio, or MSR. We’ll talk more about it later on.

Bank Loan

Bank loans can be used for both HDB flats and private properties. There are many different types of bank loans to choose from, so you should go with a bank loan that is the most suitable for your financial situation, since taking a loan is a long term commitment.

We can classify bank loans into 4 main categories:

Advantages | Disadvantages | |

Fixed Rate | No volatility, no surprises | More expensive |

Floating Rate | Cheapest on the market, rates are transparent | Very volatile, may not stay cheap for long |

Fixed Deposit-linked Rate | Not as volatile, rates are transparent | Rates can change at the bank’s discretion |

Board Rate | Great for thrill seekers who like being surprised when you least expect it | Rates are not transparent and can change at the bank’s discretion |

A fixed rate is a home loan where the interest rate is fixed throughout a period of time, typically 1 to 2 years. There are no fluctuations to the interest rate during this time, so your monthly repayment amount does not change. However, fixed rates tend to be a bit more expensive compared to other rates, because you’re paying for the stability of the rate. Fixed rates don’t stay fixed forever, though, and become floating rates after 2 to 3 years.

A floating rate is a home loan where the interest rate is pegged to the SIBOR or SOR. The SIBOR is the Singapore Interbank Offer Rate, what the SOR is the Swap Offer Rate. These are rates which are public knowledge so there’s a level of transparency.

Most floating rates use 1-month SIBOR or 3-month SIBOR as a peg, and charge an additional spread on top of it. This peg determines how volatile your home loan will be. 1-month SIBOR home loans are more volatile since they can (and will!) change every month, while 3-month SIBOR home loans are slightly more stable since they only change every 3 months. However the 3-month SIBOR is usually higher than the 1-month SIBOR. Once again, you’re paying a bit more for added stability.

Fixed deposit-linked rates are a relatively new innovation by DBS to try to create a product that has all the advantages but none of the disadvantages. Its subsequent popularity has resulted in several other banks coming up with their own versions of the product. Fixed deposit-linked rates are home loan packages that are pegged to a bank’s fixed deposit interest rates, hence the name.

Fixed deposit-linked rates are popular because they’re supposed to be just transparent and as low as SIBOR floating rates, but without the volatility. This is because raising the fixed deposit interest rate represents a significant cost to the bank, so the bank is not expected to change their rates on a whim. That said, any changes to a fixed deposit-linked rate is done at the sole discretion of the bank, which means there are no external checks and balances. This means that they’re still as dangerous as board rates.

For more information, see our write-up on fixed deposit-linked rates.

Board rates are home loans where the interest rate is completely arbitrary. The formula for determining the interest rate is at the bank’s complete discretion, and not known to the public. This means they technically have the right to change it anytime they want, as long as they give you a month’s notice. Because of this, we highly discourage customers from going with board rates, and as a result, banks themselves have mostly stopped offering board rates, replacing them with fixed deposit-linked rates.

Equity Loan (“second mortgage”)

Sometimes you can ask for what is known as a “second mortgage”. This is also known as a “equity term loan” or simply, an equity loan. This is when you borrow money, using the paid-off portion of your property as collateral. It’s a great way to get a loan with a relatively low interest rate, but it only works if your property’s appreciated in value, or if you’ve already paid off a substantial part of your home loan.

Do note that only private properties are eligible for equity loans. You can’t get an equity loan from an HDB flat.

Costs of Buying a Property

We talked earlier about the downpayment. Without a doubt, it’s the biggest upfront payment there is when buying a property. However, it’s not the only upfront payment involved. There are several other fees and charges. These include the option fee, legal fees and stamp duties (which incidentally just went up for properties above $1 million).

Buyer’s Stamp Duty (BSD)

The Buyer’s Stamp Duty, or BSD, is a tax that every home buyer has to pay when they purchase a property. The amount you have to pay depends on the price of your property, with more expensive properties being tax proportionately more. The amount you have to pay is rounded down to the nearest dollar.

Purchase Price or Market Value of the Property | BSD Rates for residential properties | BSD Rates for non-residential properties |

First $180,000 | 1% | 1% |

Next $180,000 | 2% | 2% |

Next $640,000 | 3% | 3% |

Remaining Amount | 4% |

Additional Buyer’s Stamp Duty (ABSD)

As you may have guessed by its name, it is an addition to the Buyer’s Stamp Duty that is imposed on all purchases of a residential property in Singapore. Unlike the Buyer’s Stamp Duty, the Additional Buyer’s Stamp Duty, or ABSD, is a kind of tax on the purchase of a residential property in Singapore that only affects Singapore Permanent Residents and foreigners, or Singapore Citizens who are buying more than one property.

In other words, it artificially raises the property prices for everyone except Singapore Citizens buying their first residential property.

The ABSD is calculated as a percentage of the market value of the property. Here are the current rates:

Profile of Buyer | ABSD Rates from 8 Dec 2011 to 11 Jan 2013 | ABSD Rates from 12 Jan 2013 |

Singapore Citizens buying first residential property | Not applicable | Not applicable |

Singapore Citizens buying second residential property | Not applicable | 7% |

Singapore Citizens buying third and subsequent residential property | 3% | 10% |

Singapore Permanent Residents buying first residential property | Not applicable | 5% |

Singapore Permanent Residents buying second and subsequent residential property | 3% | 10% |

Foreigners and entities buying any residential property | 10% | 15% |

Downpayment

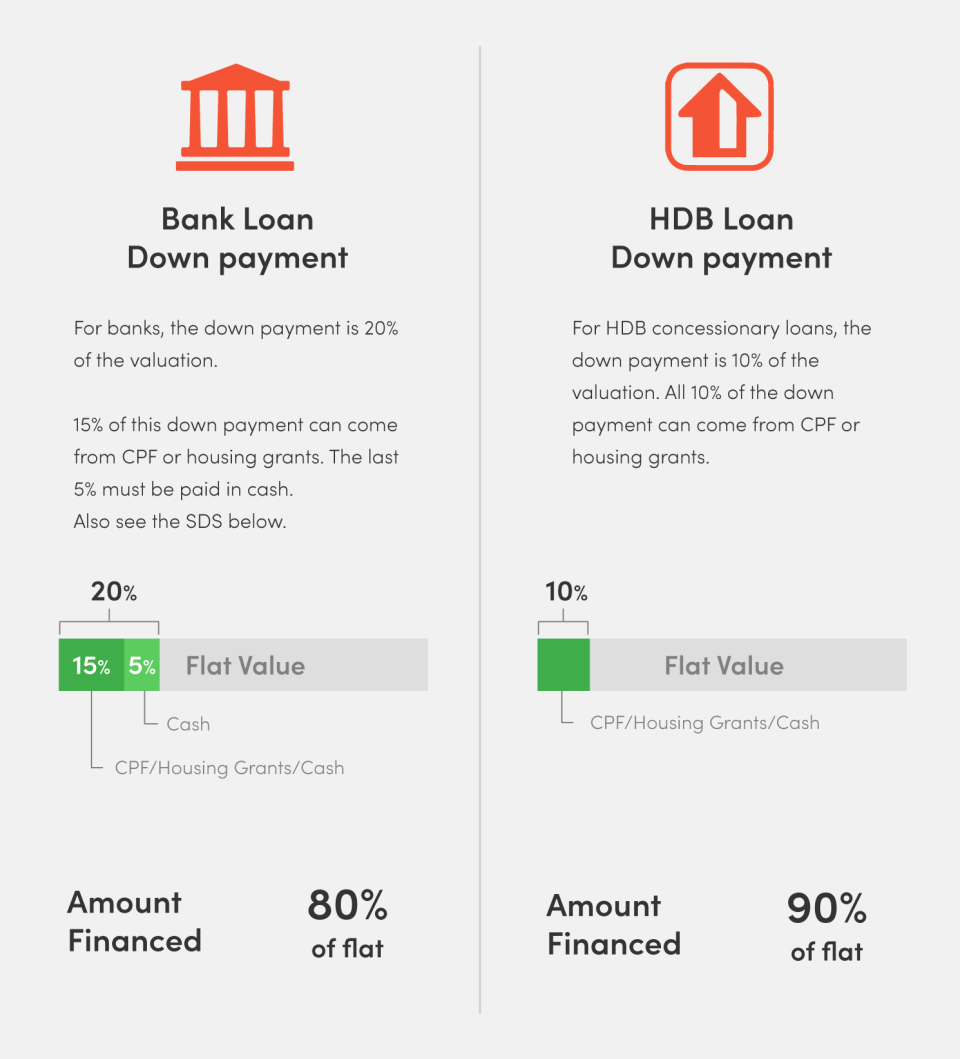

Whether you choose an HDB Loan or a Bank Loan, you will need to come up with the downpayment.

HDB Loan | Bank Loan | |

Loan Amount | Up to 90% of purchase price | Up to 80% of purchase price |

Downpayment | At least 10% of purchase price | At least 20% of purchase price |

Cash/CPF savings requirement | All 10% can come from cash and/or CPF savings | At least 5% must be cash, the remaining 15% can be in cash/CPF |

For bank loans, the downpayment needs to be 20% of the purchase price, and at least 5% must be in cash, so make sure you have the money.

If you’re buying a $600,000 flat for example, you need to have at least $120,000 set aside as a downpayment.

Purchase Price | $600,000 |

Bank Loan (80%) | $480,000 |

Downpayment (20%) | $120,000 |

At least 5% must be in cash | $30,000 |

The remaining 15% can be in cash or CPF | $90,000 |

Many of the above-mentioned fees aren’t refundable. For example, the Option to Purchase fee is usually 1% of the purchase price. For a $600,000 property, 1% is $6,000. $6,000 that you will be forfeiting if you can’t come up with the downpayment in time.

How to qualify for a home loan in Singapore

Okay, it’s time to stop putting off the most obvious question – can you even qualify for a home loan in Singapore? Here’s what you need.

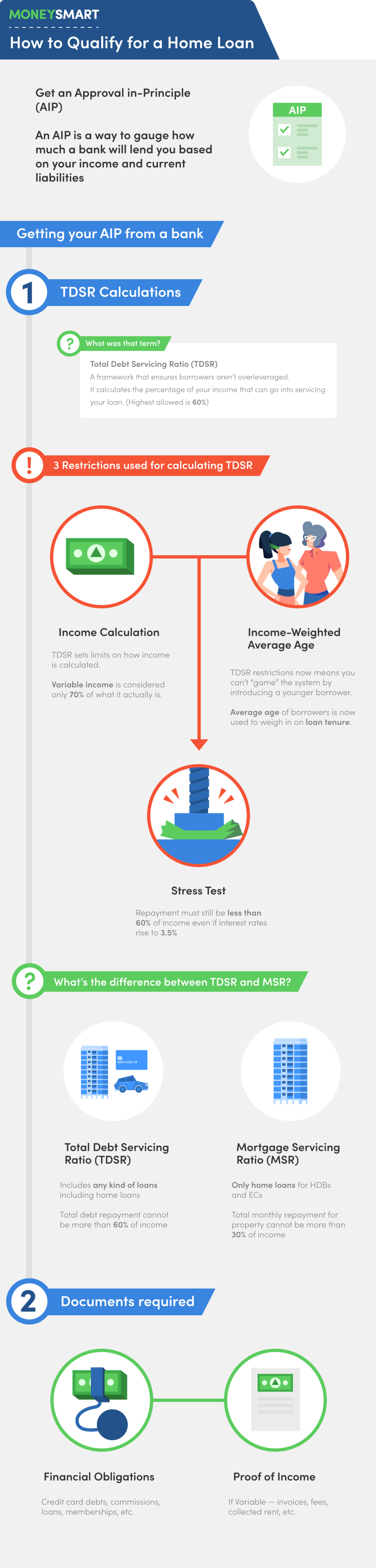

Approval In-Principle

An Approval In-Principle (AIP) is a great way to kick off the process as it is way to gauge how much a bank will lend you based on your income and current liabilities. (Sometimes AIP is also known as an In-Principle Approval (IPA). Don’t worry. They’re the same.)

You will not need an Option To Purchase to apply for one, and all it involves is providing your income related documents to a bank for assessment. The bank assesses your ability to repay the loan using what is known as the Total Debt Servicing Ratio. We talk more about this below.

Once they have assessed your finances, the bank is able to give you the approximate amount they can lend you and you can use that as a budget when searching for a property to buy. This is a more prudent approach compared to placing a downpayment for a home prematurely and then realizing you cannot loan enough money to buy the it.

What is the Total Debt Servicing Ratio (TDSR)?

The Total Debt Servicing Ratio (TDSR) framework is to ensure borrowers aren’t overleveraged (i.e. borrowing like a broke alcoholic in a liquor store). It’s a standard that applies to property loans granted by all financial institutions (not just banks).

Here’s a summary of the three main restrictions that come with TDSR.

Stress Test | Repayment must still be within TDSR constraints even if interest rates rise to 3.5% |

Income calculation | TDSR sets limits on how income is calculated. Variable income is considered only 70% of what it actually is. |

Income-Weighted Average Age | TDSR restrictions now means you can’t “game” the system by introducing a younger borrower |

TDSR calculates the percentage of your income that can go into servicing your loan. At present, the highest TDSR that financial institutions are meant to allow is 60%.

That means your housing loan repayments, after adding all your repayment obligations (student loans, credit card debts, car loans, personal loans, etc.), cannot exceed 60% of your income.

Since home loans are subject to changing interest rates. So when you take such a loan, the bank doesn’t just use the current rate; they implement a “stress test”, to see if you can handle sudden spikes in interest.

This “stress test” is now standardized at 3.5% for residential properties, and 4.5% for commercial properties.

In other words, home buyers must maintain a TDSR of 60% or under, even if interest rates were to rise to 3.5% (currently, it hovers around 1.7%).

This significantly affects the loan quantum (i.e. the total amount that can be borrowed), even if there’s no outstanding debts.

Okay, so TDSR is 60% of your income. But how do you define that income? Not everyone gets a fixed paycheck.

A businessman takes out variable sums from his business, landlords get rent, and salesmen have commissions.

Under the new TDSR framework, that’s lumped under variable income. And FIs are to treat that variable income as though it’s 30% less than it actually is.

So if you’re a business owner making an average of $5,000 a month, your income when calculating your TDSR is just $3,500. That, in turn, means a much lower loan quantum.

And lastly, forget about stretching the loan tenure.

Previously, you could make a joint application with a younger borrower (say, your daughter), and FIs would just use the age of the youngest applicant. That helped, because a 25 year old can get a 30 year loan tenure, which a 55 year old obviously can’t.

But now, the average age of the borrowers will be used; so a 25 year old and a 55 year old would count as having the collective age of 40.

Also, FIs will only count borrowers with an income. So you can’t be earning nothing, but list yourself as a co-borrower with mum or dad to lower the average age.

How is TDSR different from MSR?

Mortgage Servicing Ratio (MSR) only takes into account your housing loan repayments. So a MSR of 30% means 30% of your monthly income can go into home loan repayments, regardless of what your other repayment obligations are.

If you already have an outstanding home loan (or two), it’s unlikely you can take on another without breaking the 60% TDSR.

Total Debt Servicing Ratio | Any kind of loans including home loans | Total debt repayment cannot be more than 60% of income |

Mortgage Servicing Ratio | Home loans for HDBs and ECs | Total monthly repayment for property cannot be more than 30% of income |

What documents are required by the bank?

What statements do the banks need now? All the statements.

Credit card debts, commissions, student loans, gym memberships, the personal loan you took out to buy a decent Magic deck, all of it. And if you have variable income, you need documentary proof of rent you collect, commissions, fees from clients, etc.

If you don’t feel like listening to a million bankers telling you different things about which home loan to choose, you can always save yourself the hassle by using MoneySmart’s Home Loan Wizard and speaking to one of our mortgage specialists. You’ll come to a much more informed decision faster, and it’s free so you’re saving both time and money.

Related articles:

SIBOR Forecast 2018 – Why So Many Singaporeans Are Refinancing Now

How To Get A Home Loan On Bad Credit

HDB Loan Vs Bank Loan: Which Is Better?

3 Reasons You Shouldn’t Pay Off Your Home Loan Early

The post Home Loans in Singapore - The Complete Guide to Property Loans appeared first on the MoneySmart blog.

MoneySmart.sg helps you maximize your money. Like us on Facebook to keep up to date with our latest news and articles.

Compare and shop for the best deals on Loans, Insurance and Credit Cards on our site now!

More From MoneySmart