Yahoo Finance

Yahoo Finance Here's Why We Think Ensign Energy Services (TSE:ESI) Is Well Worth Watching

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Ensign Energy Services (TSE:ESI). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Ensign Energy Services with the means to add long-term value to shareholders.

View our latest analysis for Ensign Energy Services

How Fast Is Ensign Energy Services Growing Its Earnings Per Share?

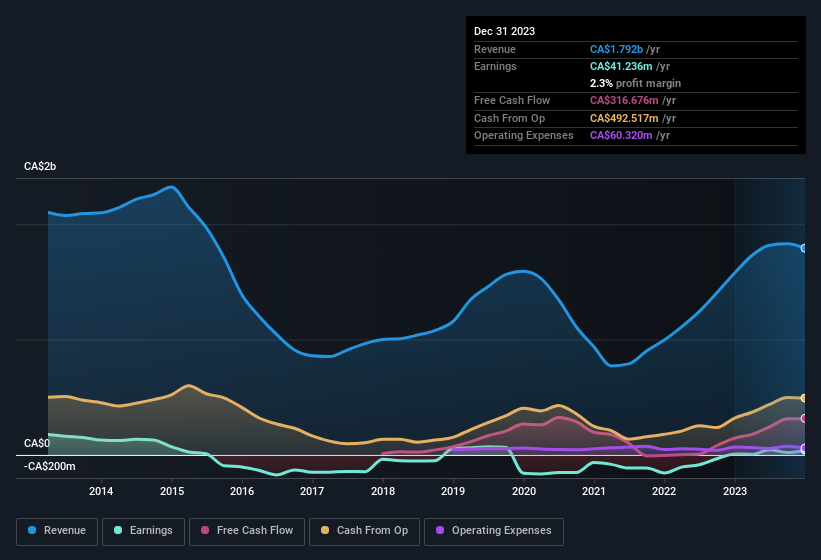

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. So for many budding investors, improving EPS is considered a good sign. Commendations have to be given in seeing that Ensign Energy Services grew its EPS from CA$0.046 to CA$0.22, in one short year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. The music to the ears of Ensign Energy Services shareholders is that EBIT margins have grown from 4.6% to 10% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Ensign Energy Services?

Are Ensign Energy Services Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Any way you look at it Ensign Energy Services shareholders can gain quiet confidence from the fact that insiders shelled out CA$799k to buy stock, over the last year. This, combined with the lack of sales from insiders, should be a great signal for shareholders in what's to come. It is also worth noting that it was President Robert Geddes who made the biggest single purchase, worth CA$747k, paying CA$2.99 per share.

On top of the insider buying, it's good to see that Ensign Energy Services insiders have a valuable investment in the business. Indeed, they have a considerable amount of wealth invested in it, currently valued at CA$136m. This totals to 27% of shares in the company. Enough to lead management's decision making process down a path that brings the most benefit to shareholders. Looking very optimistic for investors.

Does Ensign Energy Services Deserve A Spot On Your Watchlist?

Ensign Energy Services' earnings have taken off in quite an impressive fashion. Just as heartening; insiders both own and are buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Ensign Energy Services deserves timely attention. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Ensign Energy Services that you should be aware of.

Keen growth investors love to see insider buying. Thankfully, Ensign Energy Services isn't the only one. You can see a a curated list of Canadian companies which have exhibited consistent growth accompanied by recent insider buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.