Yahoo Finance

Yahoo Finance

Fastacash raises $15M series B funding to enable social payments in more markets

Fintech company Fastacash announced today it has raised US$15 million in a series B funding round. The company claims it is one of the largest series B investments for a fintech company in Singapore. The round was led by Rising Dragon Singapore, and participating investors include Russian fintech venture capital firm Life.Sreda and UVM 2 Venture Investments.

Including the series B round, Fastacash has raised a total of US$23.5 million so far, from investors like Hong Kong’s FTF (who led the company’s 2012 seed funding round) and Singapore-based Jungle Ventures and Spring SEEDS Capital.

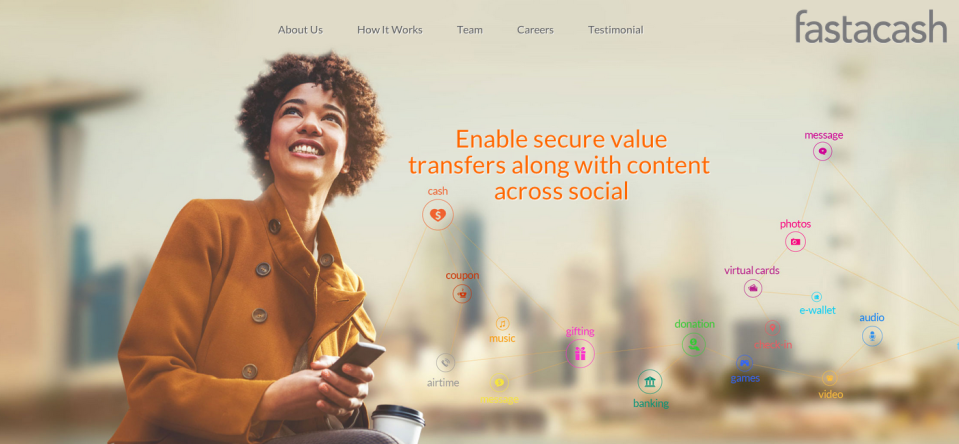

Fastacash does mobile payments, but strictly through a B2B approach. The company is providing a payment platform that can be used by partners to enable value transfers (such as money, mobile credit, or other tokens of value) using mobile and social networks.

“We want to take the capability of completing transactions and tie it to people’s social activity,” says Vince Tallent, Fastacash chairman and CEO. “If users can send photos to each other, why shouldn’t they be able to send money? We want to take transactions to where people live and breathe, and that’s social networks on their mobiles.”

Many online or mobile payments startups are looking to circumvent traditional banking and financial institutions by providing alternative payment and e-wallet systems. Fastacash is choosing to take the middle ground by partnering with those institutions and providing the transaction platform. The partners then work with the technology, which allows them to create social payment apps and services with their own branding.

For example, Fastacash has worked with Singapore bank DBS to enable this kind of social payment capability in the DBS Paylah! app. In India, it has worked with Axis Bank for the launch of Ping Pay, which allows users to send money and top-up mobile phone balances through Facebook, Whatsapp, Twitter, SMS, or email. The startup has also partnered with Visa Europe, in order to bring social payments to banks Visa Europe is working with.

See: Singapore’s DBS bank brings its Paylah mobile payments app to Apple Watch“We are a technology enabler for financial companies,” says Fastacash chief innovation officer, Shankar Narayanan. Most large banks are now looking for ways to innovate, he adds, so the company can create new products based on its partners’ needs. Narayanan reveals that a new platform to enable mobile payments for merchants is scheduled to go live “soon”. The company also plans to encourage other developers to work with its API to bring their own ideas to life.

Spreading out

Fastacash is currently active in Singapore, India, Indonesia, Russia, and Vietnam, providing payment services to six partners across those markets, according to chief marketing and strategy officer Radhika Angara. The plan now is to pursue partners in new territories. The company aims to have 64 partners within the next two to three years, targeting the next 12 months to get a third of those. Fastacash will also give its roster a boost by doubling its team from the current 44 people within a year.

Next steps include establishing a presence in the US, the UK, and the Middle East. The startup will also look to strengthen its position in India – “the largest remittance territory,” according to Tallent – the Philippines, and Indonesia. The spread of mobile devices in those countries has enabled the population to move from a cash-based economy straight to mobile transactions, almost completely bypassing credit cards. Fastacash wants to be at the forefront of that, with services addressing the needs of the unbanked population, Angara says.

Playing the long game

While there are several startups throwing their hat in the mobile transaction space, Fastacash hopes to stand out with its B2B focus. The company wants to be the one providing the tools for its partners to offer social transactions to users, rather than offer those services directly to consumers. As such, it wants to remain platform agnostic, having built a flexible enough method to be used for multiple use cases, Tallent claims.

Tallent believes that the disruption in the fintech sector isn’t going to bypass large players like banks in the long run. “B2C startups bring disruption, but how much capital can they raise?” he wonders. For all their good ideas, they lack the global reach, he says. Paypal might be the only one to scale internationally, and that has been through a very long process. Fastacash chooses to partner with big financial institutions because they have better survival prospects and they have already started to adapt to new technologies in their field.

Other projects Fastacash has been involved in are P2P money transfer services Doku, Mobi.Dengi, Oxigen Wallet, and Techcombank.

This post Fastacash raises $15M series B funding to enable social payments in more markets appeared first on Tech in Asia.