Yahoo Finance

Yahoo Finance

Get a business loan in hours? For Asia’s fintech startups, that’s the promised land.

For many startups and small enterprises, cashflow comes in fits and starts. Banks consider these companies risky, causing some loan approvals to take weeks. Interest rates are pegged high, between 18 to 30 percent a year. But for startups struggling to meet payroll, waiting often isn’t an option.

Several startups, however, believe they can improve the financing prospects for young enterprises, and in the process help these companies get on firm footing. For Asia’s optimistic and go-getting middle class, this couldn’t have come at a better time.

Singapore’s ApexPeak has what’s called invoice financing, a service which turns invoices into cash in as soon as five days. That means service providers can receive cash before payment is due. ApexPeak made a move recently that could speed things up – acquiring Dubai-based startup Cashnomix (price tag unannounced). While also an invoice financing firm, the latter has a few things that ApexPeak lacks: a presence in the Middle East, and a prototype credit scoring algorithm for invoices.

“The Cashnomix risk model solves a dilemma that has troubled the UAE for years. Credit data on companies are sparse, so making an underwriting decision is labor-intensive. The algorithm we’ve built collects signals from a large variety of sources to determine a score and a confidence index for each invoice”, says Sujith Kurup, founder of Cashnomix, who will now become the managing director of Middle East operations at the acquiring company.

ApexPeak has many features which speed up loan processing. It removes paperwork by getting sellers to upload their invoices digitally. Instead of running in one jurisdiction, it operates in 25 countries, eliminating the friction of cross-border transactions. Pair the fast processing speed with the ability to transact one invoice at a time, and you get a service that gives enterprises flexibility instead of making them stick to a lump sum term loan.

The company’s co-founder Gakim Solomons says that integrating the algorithm could speed up underwriting for loans. “Today, we can provide SMEs with an answer in five days. Tomorrow, we will be able to approve transactions in a fraction of the time.” All it’ll take is for a small enterprise to upload an invoice onto ApexPeak’s platform, which will do the rest. This speed boost is crucial for ApexPeak’s growth – five days is hardly spectacular as some banks offer business loans that can be approved in a day.

ApexPeak’s success will depend on its growth and the ability to stay liquid to finance the loans. The startup declined to reveal exact traction and growth numbers, but it has maintained a zero default rate and a treasury of about US$1.3 billion.

Automatic social proofing

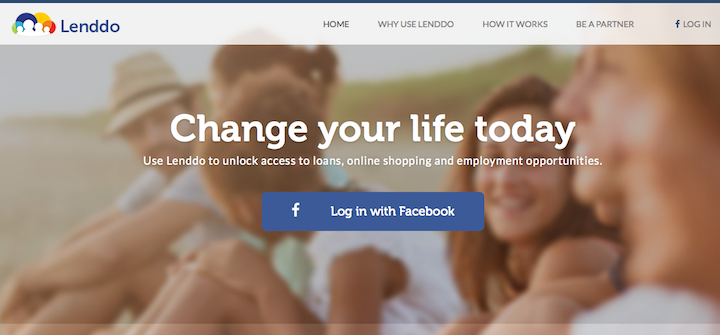

ApexPeak isn’t the only one harnessing algorithms to determine trustworthiness. Tech in Asia reported on Lenddo, a Philippine startup that can automatically figure out the credit worthiness of a loan-seeker – by looking at their social media activity. It’s a rich source of information that could be more useful than looking at credit card and digital transactions, which banks currently do. For people living in cash-based economies, credit card spend won’t be an accurate gauge of a person’s trustworthiness.

It sounds like a far-fetched idea, but the startup appears to be progressing well. It has access to the data of over one million users, and has raised US$14 million in funding from Accel Partners and other investors. Now, it’s now preparing to take its algorithm beyond approving personal loans, given that it has a default rate in the low single digits.

Telcos can use Lenddo to verify the ability of postpaid subscribers to pay. Online buyers and sellers can now quickly verify the trustworthiness of the other party. Dating sites can use it to ban troublemakers. Also, pre-employment screening can take minutes instead of two weeks, and it’ll cost a fraction less.

We may be scratching the surface of alternative finance’s potential to increase the cash liquidity of the masses. Bitcoin can foster fast and cheap cash transactions across borders, which is useful to the millions of overseas workers from the Philippines, Indonesia, and other emerging economies. But it lacks one key ingredient that would make it truly useful in peer-to-peer lending – the ability to quickly verify a borrower’s credit worthiness.

That may change soon. Singapore startup Tembusu Systems has shed its dependence on bitcoin in exchange for a new technology stack called the TRUST Framework, which is a variant of the popular Bitcoin alternative Ripple. Besides featuring blockchain technology – the backbone of the Bitcoin economy with the ability to verify transactions without involving a third-party – it also has a credit worthiness system. Essentially, the more valid transactions you make, the more ‘trust’ you earn.

Unlike Lenddo and ApexPeak, Tembusu is a relatively untested company and it’ll need to prove that it can integrate its technology with banks, governments, and other large organizations. But if the system lives up to its potential, It’s not a stretch to think that Tembusu, or a service just like it, could one day facilitate loans.

This leaves the question of what role banks can play in the fast-moving world of fintech. With legacy systems in place, billions of dollars put into incumbent businesses, as well as massive scale and size, top banks become slow giants with little incentive to innovate. It’s the smaller banks that are most open to new paradigms. They have the least to lose after all.

Nonetheless, we’re seeing signs that the financial establishment is getting involved in fintech. Bitcoin startup Coinbase has raised US$70 million from high-profile investors like the New York Stock Exchange, Spanish bank BBVA, and the former CEOs of Citigroup and Reuters. In Singapore, prominent European accelerator Startupbootcamp will be launching its fintech program soon, and it is partnering with DBS Bank and the Monetary Authority of Singapore – the country’s central bank – to assist startups in refining and testing their ideas.

It’s too early to predict how the banking establishment will react to fintech, partly because no startup in the space has reached that much-fabled disruptive potential yet. By getting involved early though, these banks possess a ringside seat to what could be the future of finance. What they do with this privilege is anybody’s guess.

See more: What the FX! Banks are bleeding you dry on your money transfers. A new startup wants to disrupt that

This post Get a business loan in hours? For Asia’s fintech startups, that’s the promised land. appeared first on Tech in Asia.