Yahoo Finance

Yahoo Finance BOK Financial (BOKF) Rides on Loan Growth as Costs Rise

BOK Financial Corporation BOKF is well-poised for revenue growth on the back of steady loan demand. High interest rates, robust deposit balance and a solid asset quality will continue to support its financials. However, elevated expenses and high debt remain concerns given limited liquidity.

BOK Financial demonstrated continued loan growth on account of diversified portfolio. Though loans declined in 2021, it witnessed a compound annual growth rate (CAGR) of 2% in the last five years (2018-2023). Concurrently, deposits saw a CAGR of 6.1%. In light of the strong loan pipeline and deposit balance, the company remains well-poised for organic growth. Management expects loans to grow in the mid-to-upper single-digit range in 2024 despite increased payoffs in commercial real estate loans. Also, deposits are projected to grow modestly.

Driven by higher rates, BOKF’s net interest income (NII) witnessed a three-year CAGR of 4.7% (ended 2023). In 2023, net interest margin (NIM) reduced to 2.93% from 2.98% in 2022 on account of deposit repricing. Given the expectations of the central bank keeping rates high in the near term, the company’s NII and NIM are expected to grow moderately as an increase in funding costs will weigh on both.

Nonetheless, restructuring of the available-for-sale loan portfolio in the fourth quarter of 2023 is expected to be accretive to both NII and NIM, per management. It anticipates NIM to decline marginally in the first quarter of 2024, with a subsequent recovery and relative stability in the following quarters attributed to stable loan demand.

Furthermore, BOK Financial’s asset quality trends seem to be encouraging as credit quality metrics have been improving compared with the pre-pandemic levels. In 2023, non-accrual loans were $145.5 million compared with $181 million in 2019. Likewise, the net-charge off ratio was 8 basis points (bps) in 2023 compared with 19 bps in 2019. Given the historical outperformance during credit cycles, BOKF is well-positioned amid expectations of an economic deceleration.

The Zacks Consensus Estimate for BOK Financial’s 2024 earnings has been revised 1.5% upward in the past 30 days.

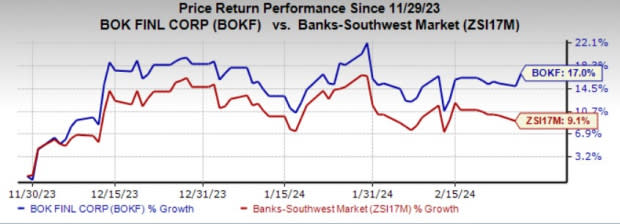

Shares of this Zacks Rank #3 (Hold) company have gained 17% over the past three months compared with the industry’s growth of 9.1%.

Image Source: Zacks Investment Research

However, BOKF remains exposed to operational risks due to elevated expenses. Operating expenses recorded a CAGR of 5.3% over the last five years (2018-2023) due to increased personnel, data processing, as well as net occupancy and equipment costs. Further escalation in the cost base is expected to result in operational inefficiency and could impede bottom-line expansion. Management projects a mid-single-digit increase in expenses in 2024.

Liquidity concerns remain another headwind for the company. As of Dec 31, 2023, BOK Financial had a total debt (comprising funds purchased and repurchase agreements as well as other borrowings) of $9.6 billion, while cash and due from banks, as well as interest-bearing cash and equivalents, aggregated to $1.49 billion. The company’s debt levels seem unsustainable, considering its relatively low cash balance. BOK Financial is, therefore, unlikely to meet its debt obligations if the economic situation deteriorates.

Bank Stocks Worth Considering

Some better-ranked bank stocks are First Financial Bancshares, Inc. FFIN and Guaranty Bancshares, Inc. GNTY. Each of them sports a Zacks Rank #1 (Strong Buy) at the moment. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for First Financial’s 2024 earnings has moved north by 5.1% in the past 30 days. The company’s shares have gained 16.1% over the past three months.

The consensus estimate for Guaranty Bancshares 2024 earnings has been revised 5.3% upward in the past 30 days. The stock has lost 2% in the past three months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BOK Financial Corporation (BOKF) : Free Stock Analysis Report

First Financial Bankshares, Inc. (FFIN) : Free Stock Analysis Report

Guaranty Bancshares Inc. (GNTY) : Free Stock Analysis Report