Yahoo Finance

Yahoo Finance Which Is The Best Savings Accounts In Singapore?

“What is the “best” savings accounts in Singapore?” On average, we are asked this question at least a few times each month.

While choosing the best savings account is hardly going to make you rich, there is no reason why you shouldn’t maximise the interest can get from savings that are going to be left idly in the bank anyway.

In this article, we will run through 5 saving accounts in Singapore, what they offer, and what customers can realistically expect to get from the accounts.

# 1 OCBC 360 Account, OCBC

For many years, the OCBC 360 Account has been one of the easiest ways to earn extra money without putting in much effort, or take any risk.

Despite the changes made last year, the OCBC 360 Account still offers pretty attractive interest rates in return for some simple everyday transactions.

Here is what you need to do to earn bonus interest on your OCBC 360 Account.

Action Item | Annual Interest |

Credit your monthly salary via Giro (minimum $2,000) | 1.2% |

Total minimum spent of $500 on OCBC Credit Cards | 0.5% |

Pay 3 bills each month | 0.5% |

Total | 2.25% (inclusive of 0.05% base interest) |

Buy an eligible OCBC product over the past year | 1% |

Advertised interest rate bank says you get: 3.25%

What we think you would realistically get: 2.25%

We don’t like having to buying an eligible OCBC product for an extra 1%, since it requires us to buy something that not everyone would normally do.

You can earn bonus Interest fairly easily. You have a minimum spent of $500 on your OCBC Credit Card (the OCBC 365 is a good place to start), credit your monthly salary, and pay 3 bills each month (e.g. credit card bill, mobile bill, utility bill).

If we assume you have the full $60,000, you earn an interest of $1,350 a year based on the 2.25% interest.

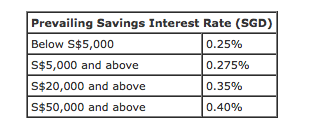

# 2 One Account, UOB

The One Account offered by fellow local bank UOB is the direct competitor to the OCBC 360. Potentially, the interest rate you earn could be higher than the OCBC 360 Account, but only given the right circumstances.

The interest rate for the One Account works in a tiered sequence.

Notice that the interest rate you could potentially earned is much higher at 3.33% per annum, and that is, without having to buy any products from the bank. You only need to spend $500 on their credit card and credit your salary, or pay 3 bills using GIRO.

However, there are two catch you need to note.

Firstly, you MUST spend $500 on the UOB One Card and/or selected UOB card. Unlike the OCBC 360 Account, where you can still earn bonus interest through bill payments or the crediting of your salary, the One Account requires you to spend $500 on credit card first each month before you can earn any bonus interest.

Secondly, interest rate shown are incremental. Here is what it means.

First $10,000 | 1.5% | $150 |

Next $20,000 | 2% | $400 |

Next $20,000 | 3.33% | $660 |

Total – $50,000 | 2.42% | $1,210 |

Advertised interest rate bank says you get – 3.33%

What we think you would realistically get – 2.42% (based on $50,000 deposit)

If you have $50,000, the effective interest rate you earn would be 2.42%, which is higher than the OCBC 360 Account. However, if you have $60,000, the effective interest rate drops to 2.03%, since the last $10,000 doesn’t earn you any bonus interest.

# 3 BOC SmartSaver, Bank Of China

Bank Of China (BOC) came onto the saving account scene and rolled out some seriously good stuff that got us excited.

Let’s start with the bonus interest first.

Earn 1.55% p.a. when you spend at least S$500 across your BOC Credit Cards and/or Debit Cards.Earn 1.00% p.a. when your company credits your salary of at least S$2,000 into your BOC MCS Account.Earn 0.60% p.a. when you transact 3 bill payments or 1 BOC Mortgage Repayment from your BOC MCS Account.

By doing the same stuff that you have done for either the OCBC 360 or the UOB One Account, you earn 3.15%, compared to 2.25% (OCBC 360) and 2.42% (One Account).

That’s not all. Base interest is also significantly higher.

For example, if you have $50,000 or more, your total interest (base interest + bonus interest) would be 3.55% per annum. This is how the interest stacks up against the other two local banks.

Savings | Interest Earned – Bank Of China | Interest Earned – OCBC 360 | Interest Earned –UOB One Account |

$50,000 | $1,775 | $1,125 | $1,210 |

$60,000 | $2,130 | $1,350 | $1,215 |

This is the first time we are writing about BOC and frankly, the numbers blew our mind. At the $60,000 mark, they are beating the OCBC 360 by $780 per annum. That’s like paying you $65 a month just to use BOC instead! Wow.

Advertised interest rate bank says you get: 3.55%

What we think you would realistically get: 3.55%

Update: BOC have changed their interest rate. To find out more about the revised interest rate, read the updated article.

# 4 CIMB FastSaver Account, CIMB

The CIMB FastSaver Account is a simple account to understand. You get 1% interest on your first $50,000 and 0.6% for any amount above $50,000.

You don’t need to do anything. No salary crediting, no credit spends, no bill payment. It’s that simple.

Advertised interest rate bank says you get: 1%

What we think you would realistically get: 1%

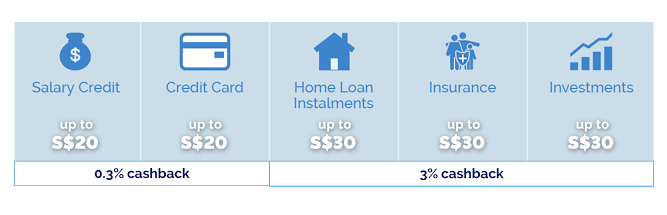

# 5 POSB CashBack Bonus, POSB

The latest entrant to the market, the POSB Cashback Bonus scheme, is a unique take on the saving account market in Singapore.

Instead of giving people bonus interest based on what they do and how much they have, the POSB Cashbank Bonus only cares about the first part, what people do.

In otherwords, whether you have $1,000 or $100,000 in your saving account doesn’t make any difference. You still get the same amount of cashback.

In order to qualify for the cashback, you need to at least have transactions in 3 out of 5 of the categories. Do also note that your salary credit must be at least $2,500 each month.

The downside to this cashback is that you would need to at least have 1 of 3 offered by POSB/DBS, a home loan mortgage, insurance products or investment products.

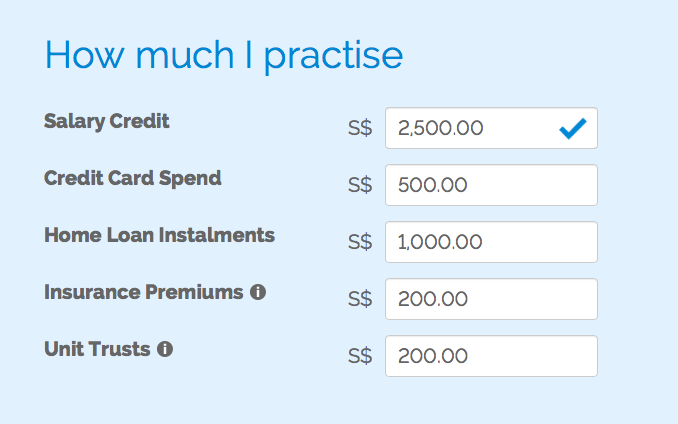

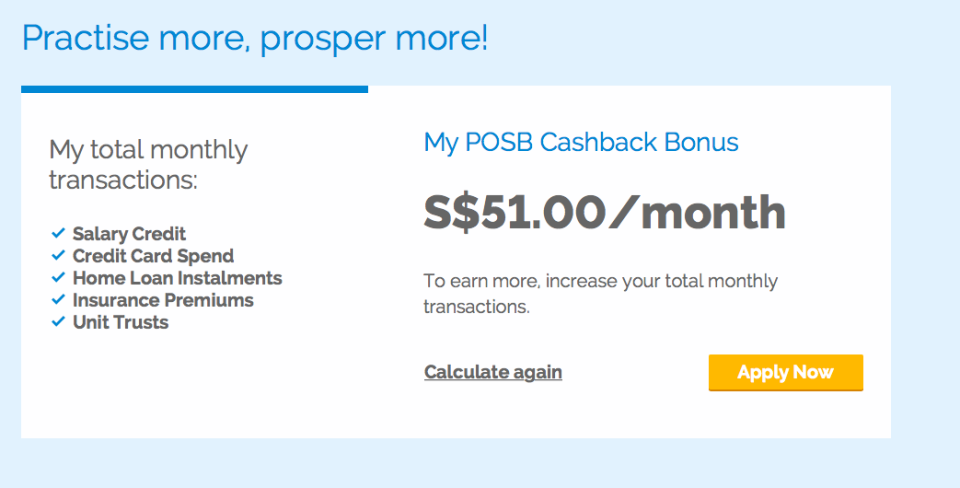

We toyed around with the inputs.

And here is how much we get in return.

Even if we decided not to credit our salary, we would still be able to enjoy a nice cashback of $42 a month, provided we have 3 different financial products with POSB/DBS.

The POSB Cashback Bonus makes sense for those who do not have a large amount of savings (yet), but only if you are intending to also get some financial products with POSB/DBS. It is possible to earn cashback from POSB while keeping your salary credited in some other banks (e.g. BOC, OCBC, UOB).

What Should I Get?

In our opinion, the BOC SmartSaver provides the best deal for saving account. A 3.55% risk-free interest is unheard of, and is pretty much unbeatable, at least for now.

Update: BOC have changed their interest rate. To find out more about the revised interest rate, read the updated article.

How can you choose winning stocks in Singapore? Join us on 16 November in our next 90-minute series: Guide To Choosing Winning Stocks, as we discuss some of the key elements to look at when choosing stocks to invest in. Subscribe to our free e-newsletter to receive exclusive content and promotions that are not available on our website. Follow us on Instagram @DNSsingapore to get daily dose of finance inspirations through photos.

The post Which Is The Best Savings Accounts In Singapore? appeared first on DollarsAndSense.sg.