Yahoo Finance

Yahoo Finance American Public (APEI) Gains on Better Enrollment View, Cost Ail

American Public Education, Inc. APEI has been riding high on solid strategies to boost enrollment and student persistence rate, cost-saving moves, acquisitions and affordability. It has been benefiting from increased demand for online courses and nursing programs.

Its focus on fulfilling the demand of nurses and other healthcare professionals and cybersecurity courses bode well. It has also been gaining traction of late as it provided near-term guidance for certain metrics.

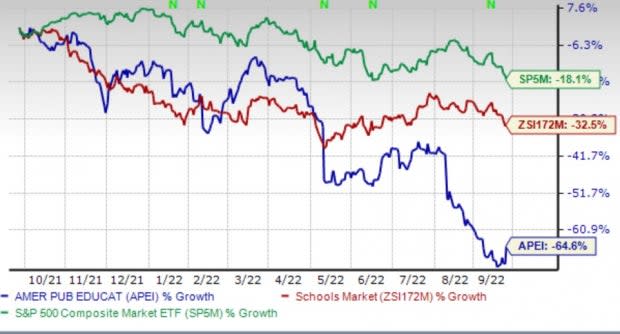

However, this Zacks Rank #4 (Sell) company has been witnessing higher costs and expenses. Also, the current macroeconomic condition is a potential headwind. In the past year, its shares tumbled 64.6% compared with the Zacks Schools industry’s 32.5% fall and S&P 500 index’s 18.1% decline.

Image Source: Zacks Investment Research

Let’s discuss the factors influencing the growth of this leading online and campus-based postsecondary education provider. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Strategies to Drive Enrollment Growth: American Public has undertaken several initiatives to improve enrollment trends and student persistence. The company intends to drive student persistence rate by improving the student mix quality, releasing new tools for students and other initiatives that increase student engagement and classroom interactivity. APEI offers various competency-based education programs, which permit students to control their own pace and progress in a program. Also, it has boosted technology investments to boost student engagement.

The company adopted a geographical approach to marketing, which focuses on using cost-effective channels and aims to reach out to college-ready students who are more likely to succeed. It aims to strengthen its digital marketing campaigns to leverage relationships with the military, public service and other high-value student populations.

The company in its recent news release noted that it has been witnessing improvement in enrollment across the segments for the next two quarters. Impressively, a shift to in-house marketing at Rasmussen and a strong interest in programs/approvals for HCN’s new Detroit campus for fall 2022 enrollment worked in favor of the company.

Business Combinations & Buyout Synergies: APEI completed the acquisitions of Rasmussen University ("RU") and GSUSA on Sep 1, 2021, and Jan 1, 2022, respectively.

RU is a nursing- and health sciences-focused institution, which provides postsecondary education to more than 17,100 students at its 23 campuses in six states and online. GSUSA provides career learning in-person and online to the federal workforce through a catalog of over 300 courses specializing in foundational and continuing professional development, as well as leadership training to advance the performance of government agencies through the competency and career advancement of their employees.

The buyouts are likely to add benefits in the future as more and more people are inclined toward these career-oriented courses. Moreover, its strong cost procurement moves will likely result in $15 million in annual cost savings, one-time transition and integration items for GSUSA and $2 million in non-recurring marketing benefits from the RU segment in 2022. This will help the company generate adjusted EBITDA of $21.1-$27.1 million in the second half of 2022 and $53-$59 million in 2022. Pro-forma adjusted EBITDA will likely be $70-76 million for the year.

Affordable Tuitions: Skill gap and increased cost of higher education have been threatening the nation. Workers are forced to take expensive courses to improve their skills. American Public continued to be a leader in affordability and value. Creating affordable pathways to support employment and career advancement would help learners of all backgrounds maximize their higher education return on investment.

Since the foundation, affordable tuition has been a priority of APUS. Currently, tuition at APUS is among the lowest in the four-year for-profit sector. TAPUS provides an APUS-funded tuition grant to undergraduate and master’s students to support its active-duty military students using TA. APUS’s low tuition and fees, in combination with APUS-funded tuition and book grant provided to all undergraduate students, active-duty military students and their spouses and dependents at the master’s level, lead to significant savings for students.

Tuition and fees at RU and HCN are also designed to be affordable and competitive with those of similar institutions offering the same level of flexibility, accessibility and student experience. At RU, students can lower their total cost of attendance through self-directed assessments, which provide savings by permitting students who demonstrate proficiency in a subject to test out of courses. The affordability of the company’s courses and programs will benefit it over the long haul.

High Costs Denting Profitability: Over the last few quarters, American Public has been experiencing increased costs, which are denting profitability. For the first half, total costs and expenses increased more than 186% year over year due to the inclusion of RU and GSUSA. Operating margins declined to a negative 44.7% versus 7.5% in the prior-year period. HCN’s operating margins declined to a negative 7.1% due to increases in nursing faculty compensation costs and other employee costs. Also, an increase in marketing expenditures dented profitability.

Macro-Economic Headwinds: APEI’s top and bottom line has been witnessing impacts of inflation and higher labor costs, particularly in RU and HCN segments. RU enrolment fell in the second quarter of 2022 due to year-over-year declines in total nursing and new nursing students enrolment, mainly caused by the impacts of the COVID-19 pandemic, record low unemployment in some RU local markets and increasing pay for nurses resulting in fewer available nursing faculty to educate and oversee clinical.

Key Picks

Some better ranked stocks in the Zacks Consumer Discretionary sector are New Oriental Education & Technology Group Inc. EDU, PowerSchool Holdings, Inc. PWSC and Virco Mfg. Corporation VIRC.

New Oriental Education currently carries a Zacks Rank #2 (Buy). The Zacks Consensus Estimates for the company’s current-year earnings reflects 204.8% year-over-year growth.

The Zacks Consensus Estimate for EDU’s fiscal 2023 earnings has been revised upward from 47 cents to 65 cents over the past 30 days.

PowerSchool currently has a Zacks Rank #2. The Zacks Consensus Estimates for this cloud-based software provider’s current-year earnings reflects 23.8% year-over-year growth.

The Zacks Consensus Estimate for PWSC’s 2022 earnings has been revised upward from 76 cents to 78 cents over the past 60 days.

Virco currently holds a Zacks Rank #2. The Zacks Consensus Estimates for this leading furniture manufacturer’s current-year earnings reflects 174.7% year-over-year growth.

The Zacks Consensus Estimate for VIRC’s fiscal 2023 earnings has been revised upward from 71 cents to 39 cents in the past seven days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Public Education, Inc. (APEI) : Free Stock Analysis Report

Virco Manufacturing Corporation (VIRC) : Free Stock Analysis Report

New Oriental Education & Technology Group, Inc. (EDU) : Free Stock Analysis Report

PowerSchool Holdings, Inc. (PWSC) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research